What is Global K-12 Technology Spend Market?

The Global K-12 Technology Spend Market refers to the total amount of money spent on technology within the kindergarten to 12th-grade education sector across the globe. This market encompasses a wide range of technological investments made by educational institutions to enhance learning, teaching, and administrative operations. It includes expenditures on hardware, software, solutions, and support services designed specifically for the K-12 education level. The significance of this market lies in its aim to integrate technology into the classroom to improve educational outcomes, facilitate personalized learning, and prepare students for a digital future. As technology becomes increasingly integral to education, the Global K-12 Technology Spend Market is witnessing substantial growth, driven by the demand for innovative educational tools and digital learning environments. This market's expansion is a testament to the global shift towards technology-enhanced learning, reflecting the evolving needs of modern education systems and the growing emphasis on preparing students with the skills necessary for the 21st century.

Hardware, Software, Solution, Support in the Global K-12 Technology Spend Market:

In the realm of the Global K-12 Technology Spend Market, investments are categorized into hardware, software, solutions, and support, each playing a pivotal role in transforming educational landscapes. Hardware encompasses the physical components such as computers, tablets, interactive whiteboards, and other devices that facilitate digital learning environments. Software includes educational and administrative applications that enhance learning experiences and operational efficiency, ranging from learning management systems (LMS) to student information systems (SIS). Solutions refer to comprehensive, integrated offerings that combine hardware, software, and services to address specific educational needs, such as digital classrooms or STEM labs. Support services are essential for the successful implementation and ongoing maintenance of technology in schools, including training for educators, technical support, and updates to ensure the longevity and effectiveness of technological investments. Together, these components form the backbone of the Global K-12 Technology Spend Market, enabling educational institutions to leverage technology for improved teaching and learning outcomes. The synergy between hardware, software, solutions, and support is crucial for creating interactive, engaging, and personalized learning experiences that meet the diverse needs of students and educators alike.

Pre-primary School, Primary School, Middle School, High School in the Global K-12 Technology Spend Market:

The Global K-12 Technology Spend Market plays a crucial role across various educational levels, including pre-primary, primary, middle, and high schools. In pre-primary schools, technology is used to introduce young learners to digital learning through interactive games and activities that foster foundational skills. At the primary school level, technology supports the development of literacy and numeracy skills, with interactive software and educational apps enhancing engagement and personalized learning. Middle schools leverage technology to facilitate project-based learning and collaboration, using tools that promote critical thinking and problem-solving skills. High schools, on the other hand, utilize advanced technologies to prepare students for higher education and the workforce, incorporating digital tools for research, advanced coursework, and career exploration. Across all these levels, the Global K-12 Technology Spend Market is instrumental in providing the infrastructure and resources necessary for implementing technology-enhanced learning. This not only enriches the educational experience but also equips students with essential digital skills, ensuring they are prepared for the challenges and opportunities of the digital age.

Global K-12 Technology Spend Market Outlook:

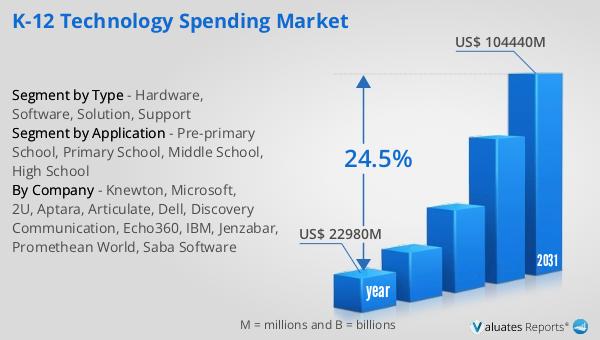

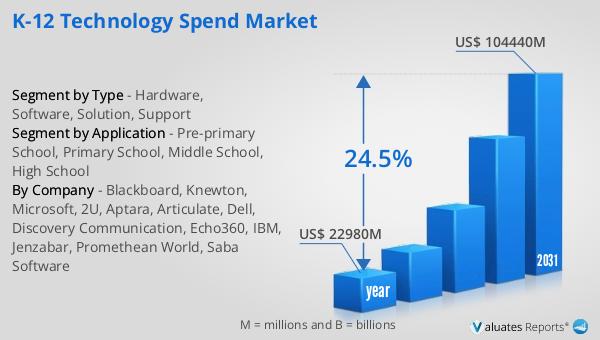

The market outlook for the Global K-12 Technology Spend Market reveals a significant growth trajectory from a valuation of US$ 14,810 million in 2023 to an anticipated US$ 70,110 million by 2030. This remarkable expansion, with a compound annual growth rate (CAGR) of 24.5% during the forecast period from 2024 to 2030, underscores the increasing investment in educational technology across the globe. This surge reflects a broader trend towards digital transformation in education, driven by the recognition of technology's potential to enhance learning outcomes, streamline administrative processes, and prepare students for a future dominated by digital competencies. The substantial growth of the Global K-12 Technology Spend Market is indicative of the sector's commitment to adopting innovative solutions and tools to foster engaging, efficient, and effective educational environments. As schools and educational institutions worldwide continue to prioritize technology integration, this market is set to play a pivotal role in shaping the future of education, highlighting the critical importance of technological investments in driving educational progress and innovation.

| Report Metric | Details |

| Report Name | K-12 Technology Spend Market |

| Accounted market size in 2023 | US$ 14810 million |

| Forecasted market size in 2030 | US$ 70110 million |

| CAGR | 24.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Blackboard, Knewton, Microsoft, 2U, Aptara, Articulate, Dell, Discovery Communication, Echo360, IBM, Jenzabar, Promethean World, Saba Software |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |