What is Global Automated Blood Component Separators Market?

The Global Automated Blood Component Separators Market refers to the sector of the healthcare industry that focuses on the development, production, and sale of automated systems used for the separation of blood components. These advanced medical devices are designed to efficiently separate whole blood into its primary components: red blood cells, plasma, and platelets. This process is crucial for various medical and research applications, enabling the targeted use of specific blood components for transfusions, research, and therapeutic purposes. The market encompasses a range of technologies and systems tailored to meet the needs of hospitals, blood banks, and research institutions worldwide. With the growing demand for blood products and the increasing emphasis on safety and efficiency in blood processing, the Global Automated Blood Component Separators Market is witnessing significant growth. Innovations in automation and separation technology are further propelling this market, making blood component separation more efficient, less time-consuming, and safer for both donors and recipients. This market's expansion is also driven by the rising prevalence of diseases requiring blood transfusions and the growing number of surgical procedures globally.

Single Press, Double Press in the Global Automated Blood Component Separators Market:

In the realm of the Global Automated Blood Component Separators Market, the technologies are primarily categorized into Single Press and Double Press systems, each with its unique operational methodologies and applications. Single Press systems are designed to perform the separation process in a single cycle. They are typically used for simpler separation tasks, where the blood component of interest can be efficiently isolated in one go. These systems are appreciated for their straightforwardness and are often favored in settings where time and simplicity are of the essence. On the other hand, Double Press systems offer a more complex separation process, capable of executing two cycles in one run. This dual-phase operation allows for a more refined separation of blood components, making it possible to isolate multiple components with higher purity levels. Double Press systems are particularly valuable in scenarios requiring the precise separation of blood components for specialized medical treatments or research purposes. The choice between Single Press and Double Press systems depends on various factors, including the specific requirements of the blood component separation task, the desired purity and volume of the separated components, and the operational capabilities of the healthcare or research facility. As the Global Automated Blood Component Separators Market continues to evolve, both Single Press and Double Press technologies are being enhanced with advanced features, such as improved automation, greater efficiency, and enhanced safety protocols, to meet the growing demands of the healthcare industry.

Hospitals, Blood Centers, Others in the Global Automated Blood Component Separators Market:

The usage of Global Automated Blood Component Separators in Hospitals, Blood Centers, and Other areas is a testament to their versatility and critical role in modern healthcare. In hospitals, these devices are indispensable for supporting a wide range of medical procedures, including surgeries, trauma care, and treatment for various conditions requiring blood transfusions. By enabling the rapid and efficient separation of blood components, these separators ensure that patients receive timely and appropriate treatment, significantly improving outcomes. Blood Centers, on the other hand, rely heavily on automated blood component separators to process and store large volumes of blood donations. These centers are responsible for ensuring a safe and adequate blood supply, making the efficiency and reliability of these devices crucial. The separators' ability to isolate specific blood components means that donors' blood can be used more effectively, catering to the diverse needs of patients. Lastly, in other areas such as research institutions and pharmaceutical companies, automated blood component separators play a vital role in advancing scientific knowledge and developing new treatments. They allow for the precise separation and analysis of blood components, facilitating research into diseases, drug development, and the creation of novel therapies. Across all these settings, the Global Automated Blood Component Separators Market is driving innovations that enhance the safety, efficiency, and effectiveness of blood component separation, ultimately contributing to better health outcomes and advancing medical science.

Global Automated Blood Component Separators Market Outlook:

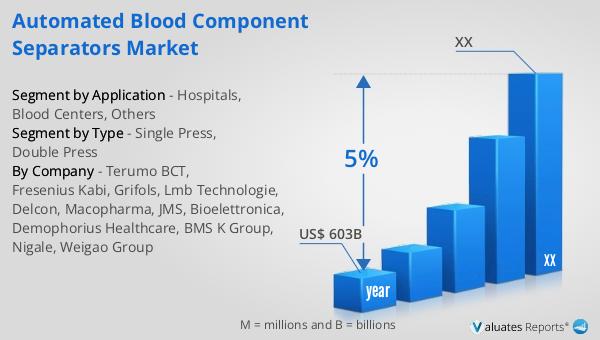

Our analysis indicates that the global market for medical devices is currently valued at approximately US$ 603 billion as of the year 2023. This market is on a trajectory of steady growth, with expectations to expand at a compound annual growth rate (CAGR) of 5% over the next six years. This growth is reflective of the increasing demand for medical technologies across various healthcare sectors, driven by factors such as the aging global population, rising prevalence of chronic diseases, and advancements in medical technologies. The expansion of the medical devices market is also supported by the growing emphasis on healthcare quality and efficiency, which encourages the adoption of innovative medical solutions. As the market continues to evolve, it is anticipated that new product developments, along with the expansion of healthcare infrastructure globally, will further propel the demand for medical devices, ensuring sustained growth in this sector.

| Report Metric | Details |

| Report Name | Automated Blood Component Separators Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Terumo BCT, Fresenius Kabi, Grifols, Lmb Technologie, Delcon, Macopharma, JMS, Bioelettronica, Demophorius Healthcare, BMS K Group, Nigale, Weigao Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |