What is Global Polycrystalline Silicon Thin Film Market?

The Global Polycrystalline Silicon Thin Film Market is a significant segment within the broader solar energy and electronics industries. Polycrystalline silicon, often referred to as polysilicon, is a material consisting of small silicon crystals. It is primarily used in the production of solar panels and electronic devices due to its semiconducting properties. The thin film variant of polycrystalline silicon is particularly valued for its efficiency and cost-effectiveness in converting sunlight into electricity. This market has been growing steadily as the demand for renewable energy sources increases globally. The thin film technology allows for the production of lightweight and flexible solar panels, which can be used in a variety of applications, from residential rooftops to large-scale solar farms. Additionally, the advancements in manufacturing processes have made polycrystalline silicon thin films more accessible and affordable, further driving their adoption. As countries strive to reduce their carbon footprint and transition to cleaner energy sources, the Global Polycrystalline Silicon Thin Film Market is poised to play a crucial role in meeting these energy needs. The market's growth is also supported by government incentives and policies promoting renewable energy, making it an attractive investment for stakeholders in the energy sector.

Chemical Vapor Deposition (CVD), Solid-Phase Crystallized (SPC), Laser-Crystallized (LC) in the Global Polycrystalline Silicon Thin Film Market:

Chemical Vapor Deposition (CVD), Solid-Phase Crystallized (SPC), and Laser-Crystallized (LC) are three critical processes in the production of polycrystalline silicon thin films, each contributing uniquely to the market. CVD is a chemical process used to produce high-purity, high-performance solid materials. In the context of polycrystalline silicon thin films, CVD involves the deposition of silicon onto a substrate through the reaction of gaseous precursors. This method is favored for its ability to produce uniform and high-quality films, which are essential for efficient solar cells and electronic devices. The CVD process is highly controllable, allowing for precise adjustments in film thickness and composition, which is crucial for optimizing the performance of the final product. On the other hand, Solid-Phase Crystallized (SPC) involves the transformation of amorphous silicon into polycrystalline silicon through a thermal annealing process. This method is known for its cost-effectiveness and simplicity, making it a popular choice for large-scale production. SPC is particularly advantageous in applications where cost reduction is a priority, such as in the manufacturing of solar panels for residential and commercial use. The process involves heating the amorphous silicon to a temperature that allows the silicon atoms to rearrange into a crystalline structure, resulting in a polycrystalline silicon film. This transformation enhances the electrical properties of the silicon, making it suitable for use in photovoltaic cells and other electronic applications. Laser-Crystallized (LC) is another technique used in the production of polycrystalline silicon thin films. This process involves the use of laser energy to crystallize amorphous silicon into polycrystalline silicon. The LC method is known for its precision and ability to produce high-quality films with excellent electrical properties. The use of lasers allows for localized heating, which minimizes thermal damage to the substrate and enables the production of films with superior crystallinity. This method is particularly beneficial in applications where high efficiency and performance are critical, such as in advanced electronic devices and high-efficiency solar cells. The LC process is also advantageous in terms of scalability, as it can be easily integrated into existing manufacturing lines, allowing for the production of large-area films. Each of these processes—CVD, SPC, and LC—offers distinct advantages and is chosen based on the specific requirements of the application. The choice of process depends on factors such as cost, desired film properties, and production scale. As the demand for polycrystalline silicon thin films continues to grow, advancements in these processes are expected to further enhance the efficiency and cost-effectiveness of the films, driving their adoption in various industries. The Global Polycrystalline Silicon Thin Film Market is thus characterized by a diverse range of production techniques, each contributing to the overall growth and development of the market.

Photovoltaics, Semiconductors, Automotive Electronics, Consumer Electronics, Others in the Global Polycrystalline Silicon Thin Film Market:

The Global Polycrystalline Silicon Thin Film Market finds extensive usage across various sectors, including photovoltaics, semiconductors, automotive electronics, consumer electronics, and others. In the field of photovoltaics, polycrystalline silicon thin films are primarily used in the production of solar panels. Their ability to efficiently convert sunlight into electricity makes them a popular choice for both residential and commercial solar installations. The thin film technology allows for the production of lightweight and flexible solar panels, which can be easily integrated into various surfaces, including rooftops and building facades. This versatility, combined with the cost-effectiveness of polycrystalline silicon, has made it a preferred material in the solar energy industry. In the semiconductor industry, polycrystalline silicon thin films are used as a key material in the fabrication of integrated circuits and other electronic components. Their excellent electrical properties and compatibility with existing semiconductor manufacturing processes make them an ideal choice for various applications. The use of polycrystalline silicon thin films in semiconductors helps improve the performance and efficiency of electronic devices, contributing to the advancement of technology in this sector. In the automotive electronics industry, polycrystalline silicon thin films are used in the production of various electronic components, including sensors, displays, and control systems. The lightweight and flexible nature of thin films makes them suitable for use in automotive applications, where space and weight are critical considerations. The use of polycrystalline silicon thin films in automotive electronics helps enhance the performance and efficiency of vehicles, contributing to the development of advanced automotive technologies. In the consumer electronics sector, polycrystalline silicon thin films are used in the production of various electronic devices, including smartphones, tablets, and laptops. Their excellent electrical properties and compatibility with existing manufacturing processes make them an ideal choice for use in consumer electronics. The use of polycrystalline silicon thin films in consumer electronics helps improve the performance and efficiency of devices, contributing to the advancement of technology in this sector. In addition to these sectors, polycrystalline silicon thin films are also used in other applications, including energy storage, lighting, and telecommunications. The versatility and cost-effectiveness of polycrystalline silicon make it a preferred material in various industries, driving the growth of the Global Polycrystalline Silicon Thin Film Market. As the demand for renewable energy and advanced electronic devices continues to grow, the usage of polycrystalline silicon thin films is expected to increase, further contributing to the development of the market.

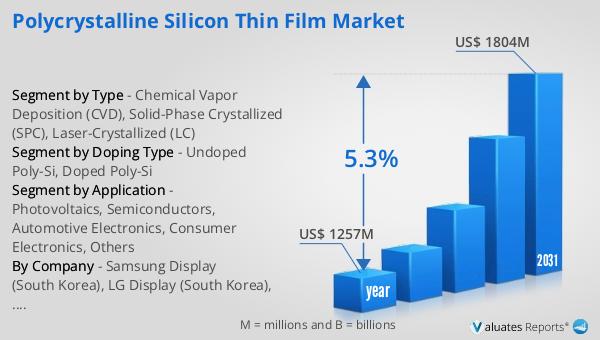

Global Polycrystalline Silicon Thin Film Market Outlook:

In 2024, the global market for Polycrystalline Silicon Thin Film was valued at approximately $1,257 million. Looking ahead, this market is anticipated to expand significantly, reaching an estimated value of $1,804 million by the year 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 5.3% over the forecast period. This upward trend is indicative of the increasing demand for polycrystalline silicon thin films across various industries, driven by the need for efficient and cost-effective solutions in renewable energy and electronics. The market's expansion is supported by advancements in manufacturing technologies, which have made polycrystalline silicon thin films more accessible and affordable. Additionally, the growing emphasis on reducing carbon emissions and transitioning to cleaner energy sources has further fueled the demand for polycrystalline silicon thin films, particularly in the solar energy sector. As countries around the world continue to invest in renewable energy infrastructure and adopt policies promoting sustainable development, the Global Polycrystalline Silicon Thin Film Market is poised for continued growth. This positive market outlook presents significant opportunities for stakeholders in the energy and electronics industries, making it an attractive investment for those looking to capitalize on the growing demand for renewable energy solutions.

| Report Metric | Details |

| Report Name | Polycrystalline Silicon Thin Film Market |

| Accounted market size in year | US$ 1257 million |

| Forecasted market size in 2031 | US$ 1804 million |

| CAGR | 5.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Doping Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Samsung Display (South Korea), LG Display (South Korea), Kyocera Display (Japan), Sharp Display (Japan), BOE Technology (China), Tianma Microelectronics (China), Visionox (China), Truly Semiconductors (China), HKC Display (China), TCL CSOT (China), AU Optronics (Taiwan), Innolux (Taiwan), HannStar Display (Taiwan) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |