What is Global Semiconductor Test Board Market?

The Global Semiconductor Test Board Market is a crucial segment within the semiconductor industry, focusing on the development and production of test boards used to evaluate the performance and reliability of semiconductor devices. These test boards are essential tools in the semiconductor manufacturing process, ensuring that chips meet the required specifications and function correctly before they are integrated into electronic devices. The market encompasses a variety of test boards, including probe cards, load boards, and burn-in boards, each serving specific testing purposes. As the demand for advanced electronic devices continues to grow, driven by technological advancements and the proliferation of IoT devices, the need for efficient and accurate semiconductor testing solutions has become more pronounced. This market is characterized by continuous innovation, with companies striving to develop test boards that can handle the increasing complexity and miniaturization of semiconductor components. The global semiconductor test board market is poised for significant growth, driven by the expanding semiconductor industry and the increasing emphasis on quality assurance and reliability in electronic products.

Probe Card, Load Board, Burn-inBoard(BIB) in the Global Semiconductor Test Board Market:

Probe cards, load boards, and burn-in boards (BIBs) are integral components of the Global Semiconductor Test Board Market, each playing a distinct role in the testing and validation of semiconductor devices. Probe cards are used in wafer testing, where they serve as the interface between the test system and the semiconductor wafer. They are designed to make contact with the pads or bumps on the wafer, allowing for the electrical testing of the individual chips before they are cut and packaged. The precision and accuracy of probe cards are critical, as they must align perfectly with the tiny contact points on the wafer to ensure reliable test results. Load boards, on the other hand, are used in the final testing phase of semiconductor devices. They are designed to hold the device under test (DUT) and connect it to the automated test equipment (ATE). Load boards must be highly reliable and capable of handling the electrical and thermal stresses associated with testing high-performance semiconductor devices. They play a crucial role in ensuring that the final packaged chips meet the required performance specifications. Burn-in boards (BIBs) are used in the burn-in testing process, where semiconductor devices are subjected to elevated temperatures and voltages for an extended period. This process is designed to identify early-life failures and ensure the long-term reliability of the devices. BIBs must be able to withstand the harsh conditions of the burn-in process while providing accurate test results. The design and construction of BIBs are critical, as they must ensure uniform temperature distribution and reliable electrical connections to the devices under test. In the context of the Global Semiconductor Test Board Market, these test boards are essential for ensuring the quality and reliability of semiconductor devices, which are increasingly being used in a wide range of applications, from consumer electronics to automotive systems and industrial equipment. As the complexity and performance requirements of semiconductor devices continue to increase, the demand for advanced test boards that can handle these challenges is expected to grow. Companies in the semiconductor test board market are continually innovating to develop new solutions that can meet the evolving needs of the industry, focusing on improving the accuracy, reliability, and efficiency of their test boards.

BGA, CSP, FC, Others in the Global Semiconductor Test Board Market:

The Global Semiconductor Test Board Market plays a vital role in the testing and validation of semiconductor devices used in various packaging technologies, including Ball Grid Array (BGA), Chip Scale Package (CSP), Flip Chip (FC), and others. BGA is a type of surface-mount packaging used for integrated circuits, characterized by an array of solder balls on the underside of the package. Test boards for BGA devices must be designed to accommodate the specific layout and pitch of the solder balls, ensuring reliable electrical connections during testing. CSP is a smaller form of packaging that allows for a higher density of connections in a compact form factor. Test boards for CSP devices must be capable of handling the fine pitch and small size of the connections, requiring precise alignment and contact during testing. Flip Chip (FC) is a method of connecting semiconductor devices to external circuitry with the chip face down, allowing for a more direct and efficient electrical path. Test boards for FC devices must be designed to handle the unique requirements of this packaging technology, including the need for precise alignment and contact with the chip's bumps or pads. In addition to these specific packaging technologies, the Global Semiconductor Test Board Market also serves other types of semiconductor devices, each with its own unique testing requirements. The increasing complexity and miniaturization of semiconductor devices have led to a growing demand for advanced test boards that can handle the challenges associated with these technologies. Companies in the semiconductor test board market are continually innovating to develop new solutions that can meet the evolving needs of the industry, focusing on improving the accuracy, reliability, and efficiency of their test boards. As the demand for advanced electronic devices continues to grow, driven by technological advancements and the proliferation of IoT devices, the need for efficient and accurate semiconductor testing solutions has become more pronounced. The Global Semiconductor Test Board Market is poised for significant growth, driven by the expanding semiconductor industry and the increasing emphasis on quality assurance and reliability in electronic products.

Global Semiconductor Test Board Market Outlook:

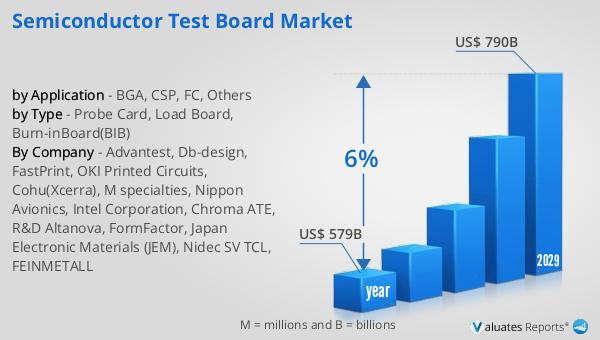

The global semiconductor market was valued at approximately $579 billion in 2022 and is anticipated to reach around $790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth trajectory underscores the increasing demand for semiconductors across various industries, driven by technological advancements and the proliferation of electronic devices. The semiconductor industry is a cornerstone of modern technology, providing the essential components that power everything from smartphones and computers to automotive systems and industrial machinery. As the world becomes increasingly digital, the demand for semiconductors is expected to continue its upward trend, fueled by the rapid adoption of emerging technologies such as artificial intelligence, 5G, and the Internet of Things (IoT). These technologies require advanced semiconductor solutions to deliver the performance and efficiency needed to support their applications. The projected growth of the semiconductor market highlights the critical role that semiconductors play in enabling innovation and driving economic growth. As the industry continues to evolve, companies are investing heavily in research and development to create new semiconductor technologies that can meet the demands of the future. The global semiconductor market is poised for significant expansion, offering opportunities for growth and innovation across a wide range of sectors.

| Report Metric | Details |

| Report Name | Semiconductor Test Board Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2025 - 2029 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Advantest, Db-design, FastPrint, OKI Printed Circuits, Cohu(Xcerra), M specialties, Nippon Avionics, Intel Corporation, Chroma ATE, R&D Altanova, FormFactor, Japan Electronic Materials (JEM), Nidec SV TCL, FEINMETALL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |