What is Global 5G Rigid PCB Market?

The Global 5G Rigid PCB Market refers to the worldwide industry focused on the production and distribution of rigid printed circuit boards (PCBs) specifically designed for 5G technology applications. Rigid PCBs are essential components in electronic devices, providing a stable platform for mounting and interconnecting electronic components. With the advent of 5G technology, which promises faster data speeds, lower latency, and enhanced connectivity, the demand for high-performance PCBs has surged. These PCBs are crucial in supporting the infrastructure required for 5G networks, including base stations, routers, and various consumer electronics. The market encompasses various types of rigid PCBs, each tailored to meet the specific requirements of 5G applications, such as high-frequency transmission and increased data handling capabilities. As 5G technology continues to expand globally, the market for these specialized PCBs is expected to grow, driven by the increasing adoption of 5G-enabled devices and the ongoing development of 5G infrastructure. This growth is further fueled by advancements in PCB manufacturing technologies, which aim to enhance the performance and reliability of these critical components in the 5G ecosystem.

Single-sided, Double-sided, Multi-layered, High-density Interconnect (HDI), Others in the Global 5G Rigid PCB Market:

The Global 5G Rigid PCB Market is characterized by several types of PCBs, each serving distinct functions and applications within the 5G technology landscape. Single-sided PCBs are the simplest form, featuring a single layer of substrate with conductive pathways on one side. These are typically used in less complex devices where space and cost are primary considerations. However, their application in 5G technology is limited due to their inability to support the high-density and high-frequency requirements of advanced 5G systems. Double-sided PCBs, on the other hand, have conductive pathways on both sides of the substrate, allowing for more complex circuitry and increased component density. This makes them more suitable for 5G applications, where efficient space utilization and enhanced performance are crucial. Multi-layered PCBs take this a step further by incorporating multiple layers of substrate and conductive pathways, enabling even greater complexity and functionality. These are essential in 5G technology, as they can support the intricate circuitry required for high-speed data transmission and processing. High-density Interconnect (HDI) PCBs represent the pinnacle of PCB technology, featuring extremely dense circuitry and microvias that allow for maximum component integration in a compact space. HDI PCBs are particularly important in 5G applications, where space is at a premium, and performance demands are high. They enable the miniaturization of devices while maintaining or even enhancing their functionality, making them ideal for use in smartphones, tablets, and other portable 5G-enabled devices. Other types of PCBs in the 5G market include flexible and rigid-flex PCBs, which offer additional design flexibility and durability. These are used in applications where the PCB must withstand mechanical stress or conform to specific shapes, such as in wearable devices or automotive applications. Overall, the diversity of PCB types in the Global 5G Rigid PCB Market reflects the varied and complex requirements of 5G technology, driving innovation and development in PCB manufacturing to meet these demands.

Automotive, Telecommunication, Consumer Electronics, Industrial, Others in the Global 5G Rigid PCB Market:

The Global 5G Rigid PCB Market finds extensive usage across various sectors, each leveraging the unique capabilities of 5G technology to enhance their operations and offerings. In the automotive industry, 5G rigid PCBs are integral to the development of advanced driver-assistance systems (ADAS), autonomous vehicles, and in-car entertainment systems. These applications require high-speed data processing and reliable connectivity, which are facilitated by the robust performance of 5G PCBs. In telecommunication, 5G rigid PCBs are crucial for the infrastructure that supports 5G networks, including base stations, routers, and network servers. The high-frequency and high-density capabilities of these PCBs enable efficient data transmission and processing, which are essential for maintaining the performance and reliability of 5G networks. Consumer electronics is another major area of application, with 5G rigid PCBs being used in smartphones, tablets, laptops, and other portable devices. The demand for faster data speeds and enhanced connectivity in these devices drives the need for advanced PCBs that can support the high-performance requirements of 5G technology. In the industrial sector, 5G rigid PCBs are used in automation systems, robotics, and industrial IoT applications. The ability to handle large volumes of data and provide real-time connectivity is crucial in these applications, where efficiency and precision are paramount. Other areas of application include healthcare, where 5G PCBs are used in medical devices and telemedicine systems, and the entertainment industry, where they support the development of virtual reality and augmented reality applications. Overall, the Global 5G Rigid PCB Market plays a vital role in enabling the widespread adoption and implementation of 5G technology across various sectors, driving innovation and enhancing the capabilities of modern electronic devices and systems.

Global 5G Rigid PCB Market Outlook:

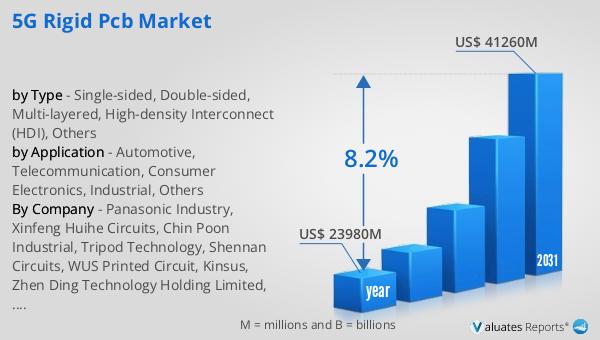

In 2024, the global market for 5G Rigid PCBs was valued at approximately $23,980 million. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an estimated size of $41,260 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 8.2% during the forecast period. The expansion of this market is driven by the increasing demand for 5G technology across various sectors, including telecommunications, automotive, consumer electronics, and industrial applications. As 5G networks continue to roll out globally, the need for high-performance PCBs that can support the advanced capabilities of 5G technology becomes more critical. This demand is further fueled by the ongoing development of 5G infrastructure and the proliferation of 5G-enabled devices, which require sophisticated PCBs to function effectively. Additionally, advancements in PCB manufacturing technologies are expected to enhance the performance and reliability of 5G rigid PCBs, further contributing to market growth. As a result, the Global 5G Rigid PCB Market is poised for substantial expansion, driven by the increasing adoption of 5G technology and the continuous evolution of electronic devices and systems.

| Report Metric | Details |

| Report Name | 5G Rigid PCB Market |

| Accounted market size in year | US$ 23980 million |

| Forecasted market size in 2031 | US$ 41260 million |

| CAGR | 8.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Panasonic Industry, Xinfeng Huihe Circuits, Chin Poon Industrial, Tripod Technology, Shennan Circuits, WUS Printed Circuit, Kinsus, Zhen Ding Technology Holding Limited, Hannstar Board, Compeq Manufacturing, NIPPON MEKTRON, Unimicron, TTM Technologies, Sierra Circuits, Lexington Europe GmbH, Winonics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |