What is Global Shikimic Acid Sales Market?

The Global Shikimic Acid Sales Market revolves around the trade and distribution of shikimic acid, a crucial compound primarily used in the pharmaceutical industry. Shikimic acid is a key ingredient in the production of antiviral drugs, most notably oseltamivir, commonly known as Tamiflu, which is used to treat influenza. The market for shikimic acid is driven by the demand for these antiviral medications, especially during flu seasons and pandemics. Additionally, shikimic acid is derived from natural sources, such as the star anise plant, and its extraction and refinement are significant aspects of the market. The global market is influenced by factors such as the availability of raw materials, advancements in extraction technologies, and the regulatory landscape governing pharmaceutical ingredients. As the demand for effective antiviral treatments continues to grow, the Global Shikimic Acid Sales Market is expected to expand, with key players focusing on enhancing production capacities and exploring sustainable sourcing methods. The market's dynamics are shaped by the interplay of supply chain efficiencies, technological innovations, and the ever-evolving needs of the healthcare sector.

in the Global Shikimic Acid Sales Market:

In the Global Shikimic Acid Sales Market, various types of shikimic acid are utilized by different customers, each catering to specific needs and applications. The primary type of shikimic acid available in the market is the 99% pure form, which is highly sought after for its efficacy in pharmaceutical applications. This high-purity shikimic acid is predominantly used by pharmaceutical companies to manufacture antiviral drugs, ensuring the highest quality and effectiveness of the final product. The demand for 99% pure shikimic acid is particularly strong in regions with advanced pharmaceutical industries, such as China and Europe, where stringent quality standards necessitate the use of high-purity ingredients. Another type of shikimic acid available in the market is the lower purity variant, which is often used in research and development settings. This type is favored by academic institutions and research laboratories that are exploring new applications and formulations of shikimic acid. The lower cost of this variant makes it an attractive option for experimental purposes, where the focus is on innovation rather than mass production. Additionally, some customers in the cosmetic industry utilize shikimic acid for its potential benefits in skincare products. Although not as prevalent as its pharmaceutical applications, shikimic acid is being explored for its antioxidant properties, which can contribute to skin health and rejuvenation. This has led to a niche market for shikimic acid in the cosmetics sector, where formulations are developed to harness its potential benefits for topical applications. Furthermore, the agricultural sector is also a customer of shikimic acid, albeit to a lesser extent. In agriculture, shikimic acid is used as a precursor in the synthesis of certain herbicides and plant growth regulators. This application is particularly relevant in regions with intensive agricultural activities, where the need for effective crop management solutions drives the demand for shikimic acid-based products. The versatility of shikimic acid across different industries highlights its importance as a multi-functional compound, with each type catering to the specific requirements of its respective market. As the Global Shikimic Acid Sales Market continues to evolve, the development of new types and formulations is expected to further diversify its applications, meeting the diverse needs of customers worldwide.

in the Global Shikimic Acid Sales Market:

The Global Shikimic Acid Sales Market finds its applications across a wide range of industries, each leveraging the unique properties of shikimic acid to meet specific needs. The most prominent application of shikimic acid is in the pharmaceutical industry, where it serves as a critical precursor in the synthesis of antiviral drugs. The production of oseltamivir, a widely used medication for treating influenza, relies heavily on shikimic acid, making it an indispensable component in the fight against viral infections. The demand for shikimic acid in this sector is driven by the need for effective antiviral treatments, particularly during flu seasons and global health crises. Beyond pharmaceuticals, shikimic acid is also utilized in the cosmetic industry, where its antioxidant properties are harnessed for skincare products. Formulations containing shikimic acid are developed to promote skin health, offering benefits such as anti-aging effects and improved skin texture. This application is gaining traction as consumers increasingly seek natural and effective ingredients in their beauty products. In the agricultural sector, shikimic acid is used as a precursor in the synthesis of certain herbicides and plant growth regulators. This application is particularly relevant in regions with intensive farming activities, where effective crop management solutions are essential for maximizing yield and ensuring sustainable agricultural practices. The versatility of shikimic acid extends to the research and development domain, where it is used in various experimental settings. Academic institutions and research laboratories explore new applications and formulations of shikimic acid, contributing to the advancement of scientific knowledge and the discovery of novel uses for this compound. The diverse applications of shikimic acid underscore its significance as a multi-functional compound, with each industry leveraging its unique properties to address specific challenges and opportunities. As the Global Shikimic Acid Sales Market continues to grow, the exploration of new applications and the development of innovative formulations are expected to further expand its reach, meeting the evolving needs of industries worldwide.

Global Shikimic Acid Sales Market Outlook:

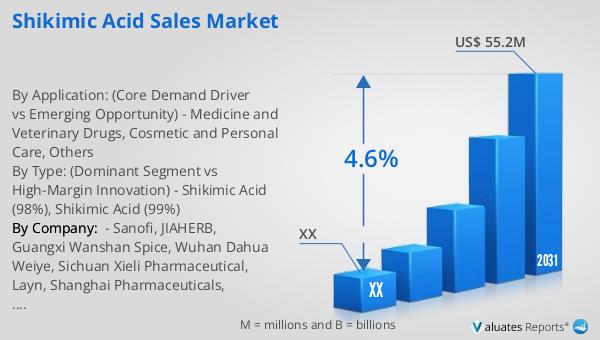

In 2024, the global market for shikimic acid was valued at approximately $40.5 million. Projections indicate that by 2031, this market is expected to grow to a revised size of $55.2 million, reflecting a compound annual growth rate (CAGR) of 4.6% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold over 70% of the market share. China emerges as the largest market for shikimic acid, accounting for more than 80% of the global share, followed by Europe, which holds about 20%. This significant market presence in China is attributed to the country's robust pharmaceutical industry and its capacity to produce high-purity shikimic acid. The market segmentation analysis, particularly in Chapter 4, highlights the potential for discovering untapped markets, often referred to as "blue ocean markets." An example of this is the demand for 99% pure shikimic acid in China, which presents opportunities for growth and expansion. The market outlook underscores the importance of strategic positioning and innovation in capturing these emerging opportunities, ensuring sustained growth and competitiveness in the Global Shikimic Acid Sales Market.

| Report Metric | Details |

| Report Name | Shikimic Acid Sales Market |

| Forecasted market size in 2031 | US$ 55.2 million |

| CAGR | 4.6% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Sanofi, JIAHERB, Guangxi Wanshan Spice, Wuhan Dahua Weiye, Sichuan Xieli Pharmaceutical, Layn, Shanghai Pharmaceuticals, Dongyangguang, Shaanxi Hongda |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |