What is Global Soil Moisture Monitoring System Sales Market?

The Global Soil Moisture Monitoring System Sales Market is a specialized segment within the broader agricultural and environmental monitoring industry. This market focuses on the development, sale, and implementation of systems designed to measure and monitor soil moisture levels. These systems are crucial for optimizing agricultural productivity, managing water resources, and mitigating the impacts of droughts and floods. They provide real-time data that helps farmers, researchers, and environmentalists make informed decisions about irrigation, crop selection, and land management. The market is driven by the increasing need for efficient water management practices, especially in regions facing water scarcity. Technological advancements have led to the development of more accurate and user-friendly systems, further propelling market growth. The market is characterized by a variety of products, including sensors, data loggers, and software solutions, each catering to different user needs and preferences. As awareness about sustainable agricultural practices grows, the demand for soil moisture monitoring systems is expected to rise, making it a vital component of modern agriculture and environmental management.

in the Global Soil Moisture Monitoring System Sales Market:

The Global Soil Moisture Monitoring System Sales Market offers a diverse range of products tailored to meet the varying needs of its customers. One of the most common types is the Tensiometer System, which measures the tension or suction of water in the soil. This system is particularly popular among farmers and agricultural professionals because it provides precise data on soil moisture levels, helping them optimize irrigation schedules and improve crop yields. Another widely used type is the Volumetric Soil Moisture Sensor, which measures the volume of water in the soil. This type is favored by researchers and environmentalists who require accurate data for scientific studies and environmental assessments. Capacitance Sensors are also prevalent in the market, known for their ability to provide continuous soil moisture readings. These sensors are often used in automated irrigation systems, allowing for real-time adjustments based on soil moisture levels. Time Domain Reflectometry (TDR) Sensors are another type, offering high accuracy and reliability. They are commonly used in research settings and large-scale agricultural operations. Additionally, there are Gypsum Blocks, which are a cost-effective option for measuring soil moisture in specific soil types. These blocks are often used in educational settings and by small-scale farmers. Each type of soil moisture monitoring system has its own set of advantages and limitations, making it essential for customers to choose the right system based on their specific needs and budget. The market is also seeing an increase in the adoption of wireless and IoT-enabled systems, which offer the convenience of remote monitoring and data analysis. These advanced systems are particularly appealing to tech-savvy farmers and large agricultural enterprises looking to integrate precision agriculture practices. As the market continues to evolve, manufacturers are focusing on developing more user-friendly and affordable systems to cater to a broader audience. This includes the introduction of smartphone apps and cloud-based platforms that allow users to access and analyze soil moisture data from anywhere in the world. The growing emphasis on sustainable agriculture and water conservation is also driving innovation in the market, with companies investing in research and development to create more efficient and eco-friendly products. Overall, the Global Soil Moisture Monitoring System Sales Market is characterized by a wide range of products that cater to the diverse needs of its customers, from small-scale farmers to large agricultural corporations and research institutions.

in the Global Soil Moisture Monitoring System Sales Market:

The Global Soil Moisture Monitoring System Sales Market serves a wide array of applications, each benefiting from the precise data these systems provide. In agriculture, these systems are indispensable for optimizing irrigation practices. By providing real-time soil moisture data, farmers can make informed decisions about when and how much to water their crops, leading to improved yields and reduced water usage. This is particularly important in regions facing water scarcity, where efficient water management is crucial for sustainable agriculture. Beyond agriculture, soil moisture monitoring systems are also used in environmental management. They help researchers and environmentalists monitor soil health and assess the impacts of climate change on ecosystems. By tracking soil moisture levels, they can study patterns of drought and flood, contributing to better land management and conservation strategies. In the construction industry, these systems are used to assess soil stability and suitability for building projects. Accurate soil moisture data is essential for ensuring the safety and longevity of structures, particularly in areas prone to soil erosion or landslides. Additionally, soil moisture monitoring systems are used in landscaping and gardening, helping homeowners and landscapers maintain healthy lawns and gardens. By providing precise data on soil moisture levels, these systems enable users to optimize watering schedules and conserve water. The market is also seeing increased adoption in sports turf management, where maintaining optimal soil moisture levels is crucial for the health and performance of sports fields. Overall, the Global Soil Moisture Monitoring System Sales Market plays a vital role in various applications, from agriculture and environmental management to construction and landscaping, providing valuable data that supports sustainable practices and efficient resource management.

Global Soil Moisture Monitoring System Sales Market Outlook:

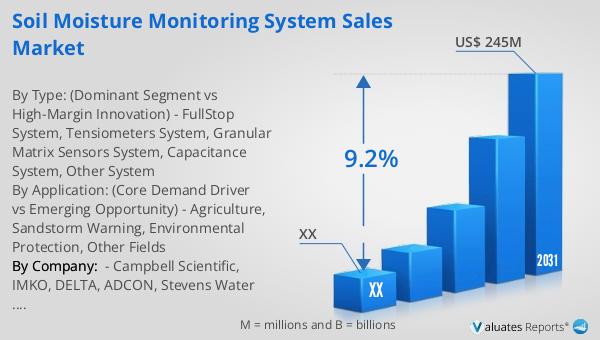

In 2024, the global market for Soil Moisture Monitoring Systems was valued at approximately $133 million. Looking ahead, it is projected to grow significantly, reaching an estimated $245 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 9.2% during the forecast period from 2025 to 2031. The market is characterized by a competitive landscape, with the top four manufacturers collectively holding a market share exceeding 20%. Among the various product segments, the Tensiometer System stands out as the largest, accounting for about 30% of the market share. This indicates a strong preference for Tensiometer Systems among consumers, likely due to their precision and reliability in measuring soil moisture levels. The market's growth is driven by increasing awareness of the importance of efficient water management and sustainable agricultural practices. As more regions face water scarcity and climate change impacts, the demand for accurate soil moisture monitoring systems is expected to rise. Manufacturers are focusing on innovation and technological advancements to meet this growing demand, offering more user-friendly and cost-effective solutions. Overall, the Global Soil Moisture Monitoring System Sales Market is poised for significant growth, driven by the need for efficient resource management and sustainable practices.

| Report Metric | Details |

| Report Name | Soil Moisture Monitoring System Sales Market |

| Forecasted market size in 2031 | US$ 245 million |

| CAGR | 9.2% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Campbell Scientific, IMKO, DELTA, ADCON, Stevens Water Monitoring Systems, McCrometer, Lindsay, Eco-Drip, Isaacs & Associates, Skye, CHINA HUAYUN GROUP, Hebei Fei Meng electric Technology, FORTUNE FLYCO, JIANGSU RADIO SCIENTIFIC INSTITUTE, Jinzhou Sunshine Technology, TOOP, ZHONETI, BAOTAI, FRT |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |