What is Global Aluminum and Composites for Aerospace Market?

The Global Aluminum and Composites for Aerospace Market is a dynamic and evolving sector that plays a crucial role in the aerospace industry. This market encompasses the production and application of aluminum and composite materials specifically designed for use in aircraft and spacecraft. Aluminum, known for its lightweight and durable properties, has been a staple in aerospace manufacturing for decades. Composites, on the other hand, are engineered materials made from two or more constituent materials with significantly different physical or chemical properties. These materials are combined to produce a material with characteristics different from the individual components. The demand for these materials is driven by the need for lighter, more fuel-efficient aircraft that can reduce operational costs and environmental impact. As the aerospace industry continues to grow, particularly with the expansion of commercial air travel and advancements in military technology, the market for aluminum and composites is expected to expand, offering new opportunities for innovation and development in material science and engineering. The integration of these materials into aerospace design not only enhances performance but also contributes to the sustainability goals of the industry.

Aluminum, Composites in the Global Aluminum and Composites for Aerospace Market:

Aluminum and composites are integral to the Global Aluminum and Composites for Aerospace Market, each offering unique benefits that cater to the demanding requirements of the aerospace industry. Aluminum is prized for its lightweight nature, high strength-to-weight ratio, and resistance to corrosion, making it an ideal choice for aircraft structures. It is used extensively in the construction of fuselages, wings, and other critical components where weight reduction is essential for fuel efficiency and performance. The ability of aluminum to withstand high stress and its recyclability further enhance its appeal in aerospace applications. On the other hand, composites are engineered materials that combine two or more distinct substances to create a material with superior properties. In aerospace, composites often consist of a matrix material, such as epoxy, reinforced with fibers like carbon or glass. These materials are known for their exceptional strength, stiffness, and lightweight characteristics, which are crucial for modern aircraft design. Composites allow for greater design flexibility, enabling the creation of complex shapes and structures that would be difficult or impossible to achieve with traditional materials. This flexibility is particularly valuable in the development of aerodynamic surfaces and components that require precise engineering to optimize performance. The use of composites also contributes to noise reduction and improved thermal insulation, enhancing passenger comfort and safety. As the aerospace industry continues to evolve, the demand for advanced materials like aluminum and composites is expected to grow, driven by the need for more efficient, sustainable, and high-performance aircraft. The integration of these materials into aerospace design not only enhances performance but also contributes to the sustainability goals of the industry. The ongoing research and development in material science are likely to yield new innovations that will further expand the capabilities and applications of aluminum and composites in aerospace.

Commercial Aircraft, Military Aircraft, Helicopter in the Global Aluminum and Composites for Aerospace Market:

The usage of Global Aluminum and Composites for Aerospace Market materials extends across various segments of the aerospace industry, including commercial aircraft, military aircraft, and helicopters. In commercial aircraft, the primary focus is on reducing weight to improve fuel efficiency and lower operating costs. Aluminum has been a traditional choice for constructing the fuselage, wings, and other structural components due to its lightweight and durable nature. However, the increasing demand for more efficient and environmentally friendly aircraft has led to a growing interest in composites. These materials offer significant weight savings and can be tailored to meet specific performance requirements, making them ideal for use in commercial aviation. Composites are often used in the construction of wings, tail sections, and other aerodynamic surfaces, where their strength and stiffness contribute to improved fuel efficiency and reduced emissions. In military aircraft, the emphasis is on performance, stealth, and survivability. Aluminum and composites are used extensively to achieve these objectives. The lightweight nature of these materials allows for greater maneuverability and speed, while their strength and durability enhance the aircraft's ability to withstand the rigors of combat. Composites, in particular, are valued for their radar-absorbing properties, which contribute to the stealth capabilities of modern military aircraft. These materials are used in the construction of fuselages, wings, and other critical components, where their advanced properties can be fully utilized. In helicopters, the use of aluminum and composites is driven by the need for lightweight, high-performance materials that can withstand the unique challenges of rotary-wing flight. The rotor blades, in particular, benefit from the use of composites, which offer the necessary strength and stiffness to withstand the high stresses and vibrations experienced during flight. The use of these materials also contributes to noise reduction and improved fuel efficiency, enhancing the overall performance and sustainability of helicopters. As the aerospace industry continues to evolve, the demand for advanced materials like aluminum and composites is expected to grow, driven by the need for more efficient, sustainable, and high-performance aircraft.

Global Aluminum and Composites for Aerospace Market Outlook:

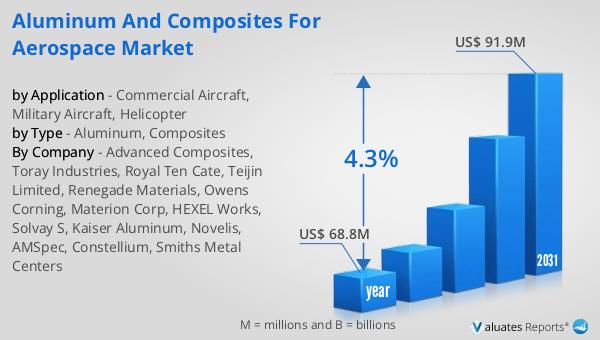

The global market for Aluminum and Composites for Aerospace was valued at $68.8 million in 2024, with projections indicating a growth to $91.9 million by 2031. This growth represents a compound annual growth rate (CAGR) of 4.3% over the forecast period. This upward trend is indicative of the increasing demand for lightweight, durable materials in the aerospace industry, driven by the need for more fuel-efficient and environmentally friendly aircraft. The use of aluminum and composites in aerospace applications offers significant advantages in terms of weight reduction, performance enhancement, and sustainability. As the industry continues to evolve, the demand for these materials is expected to grow, offering new opportunities for innovation and development in material science and engineering. The integration of these materials into aerospace design not only enhances performance but also contributes to the sustainability goals of the industry. The ongoing research and development in material science are likely to yield new innovations that will further expand the capabilities and applications of aluminum and composites in aerospace. The market outlook for aluminum and composites in aerospace is positive, with continued growth expected as the industry seeks to meet the challenges of the future.

| Report Metric | Details |

| Report Name | Aluminum and Composites for Aerospace Market |

| Accounted market size in year | US$ 68.8 million |

| Forecasted market size in 2031 | US$ 91.9 million |

| CAGR | 4.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Advanced Composites, Toray Industries, Royal Ten Cate, Teijin Limited, Renegade Materials, Owens Corning, Materion Corp, HEXEL Works, Solvay S, Kaiser Aluminum, Novelis, AMSpec, Constellium, Smiths Metal Centers |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |