What is Diode Pumped Solid State Laser (DPSSL) - Global Market?

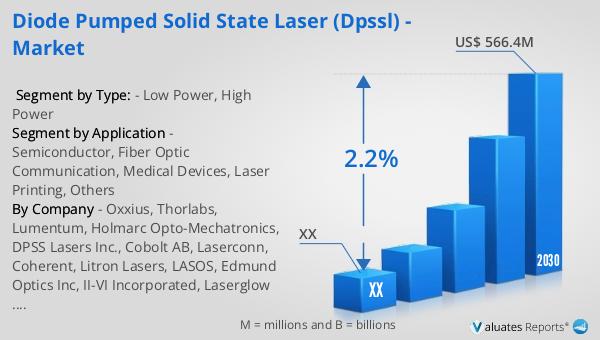

Diode Pumped Solid State Lasers (DPSSLs) represent a significant segment within the global laser technology market. These lasers utilize a diode laser to pump a solid gain medium, typically a crystal like neodymium-doped yttrium aluminum garnet (Nd:YAG), to produce laser light. This method of pumping is more efficient than traditional lamp-pumped lasers, offering advantages such as higher efficiency, longer lifespan, and better beam quality. DPSSLs are used in a variety of applications due to their ability to produce high-intensity beams with precision. The global market for DPSSLs was valued at approximately US$ 487.4 million in 2023, and it is projected to grow steadily, reaching an estimated US$ 566.4 million by 2030. This growth is driven by increasing demand across various industries, including telecommunications, healthcare, and manufacturing, where precision and efficiency are paramount. The market's expansion is also supported by technological advancements that enhance the performance and reduce the costs of these lasers, making them more accessible for a wider range of applications. As industries continue to evolve, the role of DPSSLs is expected to become even more integral, supporting innovations and efficiencies across multiple sectors.

Low Power, High Power in the Diode Pumped Solid State Laser (DPSSL) - Global Market:

In the realm of Diode Pumped Solid State Lasers (DPSSLs), the distinction between low power and high power lasers is crucial for understanding their applications and market dynamics. Low power DPSSLs typically operate at power levels ranging from a few milliwatts to several watts. These lasers are predominantly used in applications where precision and control are more critical than raw power. For instance, in the medical field, low power DPSSLs are employed in procedures such as eye surgery and skin treatments, where they provide the necessary precision without causing excessive damage to surrounding tissues. Similarly, in the realm of scientific research, low power lasers are used for spectroscopy and other analytical techniques that require precise measurements. On the other hand, high power DPSSLs, which can operate at power levels of several watts to kilowatts, are essential in industries where cutting, welding, and material processing are required. These lasers are capable of delivering the high energy needed to cut through metals and other materials with precision and speed. In the manufacturing sector, high power DPSSLs are used for tasks such as cutting, welding, and engraving, where their ability to deliver concentrated energy efficiently is invaluable. The global market for DPSSLs is witnessing a growing demand for both low and high power lasers, driven by advancements in technology and the increasing need for precision and efficiency in various applications. As industries continue to innovate and seek more efficient solutions, the demand for DPSSLs is expected to rise, with both low and high power lasers playing pivotal roles in meeting the diverse needs of different sectors. The market's growth is further supported by ongoing research and development efforts aimed at enhancing the performance and reducing the costs of these lasers, making them more accessible and appealing to a broader range of industries. As a result, the global DPSSL market is poised for continued expansion, with both low and high power lasers contributing significantly to its growth.

Semiconductor, Fiber Optic Communication, Medical Devices, Laser Printing, Others in the Diode Pumped Solid State Laser (DPSSL) - Global Market:

Diode Pumped Solid State Lasers (DPSSLs) have found extensive applications across various industries, each leveraging the unique capabilities of these lasers to enhance efficiency and precision. In the semiconductor industry, DPSSLs are used for tasks such as wafer inspection and photolithography, where their ability to produce high-intensity, focused beams is crucial for achieving the precision required in semiconductor manufacturing. The demand for DPSSLs in this sector is driven by the increasing complexity of semiconductor devices and the need for more precise manufacturing processes. In fiber optic communication, DPSSLs play a vital role in the transmission of data over long distances. Their ability to produce stable, high-quality beams makes them ideal for use in optical amplifiers and other components of fiber optic networks, where maintaining signal integrity is essential. The growing demand for high-speed internet and data services is fueling the need for advanced fiber optic communication systems, thereby driving the demand for DPSSLs in this sector. In the medical field, DPSSLs are used in a variety of applications, including laser surgery, dermatology, and ophthalmology. Their precision and ability to produce controlled, high-intensity beams make them ideal for procedures that require minimal invasiveness and high accuracy. The increasing demand for minimally invasive medical procedures is contributing to the growth of the DPSSL market in the healthcare sector. In laser printing, DPSSLs are used to produce high-quality prints with precision and speed. Their ability to produce consistent, high-intensity beams ensures that prints are sharp and clear, making them ideal for use in both commercial and industrial printing applications. The demand for high-quality printing solutions is driving the adoption of DPSSLs in this sector. Beyond these specific applications, DPSSLs are also used in a variety of other industries, including defense, automotive, and entertainment, where their unique capabilities are leveraged to enhance performance and efficiency. As industries continue to evolve and seek more efficient solutions, the demand for DPSSLs is expected to grow, with their applications expanding across a wider range of sectors.

Diode Pumped Solid State Laser (DPSSL) - Global Market Outlook:

The global market for Diode Pumped Solid State Lasers (DPSSLs) was valued at approximately US$ 487.4 million in 2023. It is anticipated to grow to a revised size of US$ 566.4 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.2% over the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for DPSSLs across various industries, driven by their efficiency, precision, and versatility. In parallel, the global semiconductor market was estimated at US$ 579 billion in 2022 and is projected to reach US$ 790 billion by 2029, growing at a CAGR of 6% during the forecast period. The growth in the semiconductor market is fueled by the rising demand for electronic devices, advancements in technology, and the increasing complexity of semiconductor devices. As the semiconductor industry continues to expand, the demand for DPSSLs is expected to rise, given their critical role in semiconductor manufacturing processes. The synergy between the growth of the DPSSL market and the semiconductor industry highlights the interconnectedness of these sectors and underscores the importance of DPSSLs in supporting technological advancements and innovations. As industries continue to evolve and seek more efficient solutions, the demand for DPSSLs is expected to grow, with their applications expanding across a wider range of sectors.

| Report Metric | Details |

| Report Name | Diode Pumped Solid State Laser (DPSSL) - Market |

| Forecasted market size in 2030 | US$ 566.4 million |

| CAGR | 2.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Oxxius, Thorlabs, Lumentum, Holmarc Opto-Mechatronics, DPSS Lasers Inc., Cobolt AB, Laserconn, Coherent, Litron Lasers, LASOS, Edmund Optics Inc, II-VI Incorporated, Laserglow Technologies, Quantum Composers, Crystalaser |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |