What is Polyurethane Foam (PUR) Sandwich Panel - Global Market?

Polyurethane Foam (PUR) Sandwich Panels are a significant component in the construction and insulation industries, known for their excellent thermal insulation properties and structural strength. These panels consist of a core made from polyurethane foam, sandwiched between two layers of durable material, often metal or plastic. The foam core provides high insulation efficiency, making these panels ideal for maintaining temperature control in various environments. The global market for PUR Sandwich Panels is driven by the increasing demand for energy-efficient building solutions and the need for lightweight, durable construction materials. These panels are used in a wide range of applications, from residential and commercial buildings to industrial facilities and cold storage units. Their versatility, combined with the growing emphasis on sustainable construction practices, has led to a steady increase in their adoption worldwide. As industries continue to seek materials that offer both performance and environmental benefits, the demand for PUR Sandwich Panels is expected to grow, reflecting their critical role in modern construction and insulation solutions.

Thickness below 51 mm, Thickness 51 mm-100 mm, Thickness above 100mm in the Polyurethane Foam (PUR) Sandwich Panel - Global Market:

When examining the global market for Polyurethane Foam (PUR) Sandwich Panels based on thickness, we can categorize them into three main segments: below 51 mm, 51 mm to 100 mm, and above 100 mm. Panels with a thickness below 51 mm are typically used in applications where space is limited, and weight is a critical factor. These thinner panels are often employed in interior partitions and ceilings, where they provide adequate insulation without adding significant bulk. Despite their reduced thickness, they still offer good thermal performance, making them suitable for environments where moderate insulation is sufficient. On the other hand, panels with a thickness ranging from 51 mm to 100 mm are more versatile and widely used in various construction applications. This thickness range strikes a balance between insulation efficiency and structural integrity, making these panels ideal for both walls and roofs in residential and commercial buildings. They provide enhanced thermal resistance, which is crucial for maintaining energy efficiency in buildings. Additionally, these panels are often used in industrial settings, where they contribute to maintaining controlled environments. Panels with a thickness above 100 mm are primarily used in applications requiring superior insulation, such as cold storage facilities and specialized industrial environments. The increased thickness provides exceptional thermal resistance, ensuring that temperature-sensitive goods are stored under optimal conditions. These panels are also used in extreme climates, where maintaining internal temperatures is critical. The global market for PUR Sandwich Panels is influenced by various factors, including regional climate conditions, building regulations, and the growing emphasis on energy efficiency. As the demand for sustainable and energy-efficient building materials continues to rise, manufacturers are focusing on developing panels with improved insulation properties and environmental performance. This trend is expected to drive innovation in the production of PUR Sandwich Panels, leading to the development of new products that cater to the diverse needs of the construction industry.

Building Wall, Building Roof, Cold Storage in the Polyurethane Foam (PUR) Sandwich Panel - Global Market:

Polyurethane Foam (PUR) Sandwich Panels are extensively used in the construction industry, particularly in building walls, roofs, and cold storage facilities. In building walls, these panels offer excellent thermal insulation, helping to maintain comfortable indoor temperatures while reducing energy consumption. Their lightweight nature makes them easy to install, reducing construction time and labor costs. Additionally, PUR Sandwich Panels provide sound insulation, contributing to a quieter indoor environment. In building roofs, these panels are valued for their ability to withstand harsh weather conditions while providing superior insulation. They help in reducing heat transfer, keeping buildings cooler in the summer and warmer in the winter. This not only enhances occupant comfort but also leads to significant energy savings. The durability of these panels ensures a long lifespan, making them a cost-effective solution for roofing applications. In cold storage facilities, PUR Sandwich Panels are indispensable due to their exceptional thermal resistance. They help maintain the low temperatures required for storing perishable goods, ensuring product quality and safety. The panels' ability to prevent heat ingress is crucial in minimizing energy consumption and operational costs in these facilities. Furthermore, their moisture resistance properties help prevent condensation and mold growth, which are critical considerations in cold storage environments. Overall, the use of PUR Sandwich Panels in these areas highlights their versatility and effectiveness in providing insulation and structural benefits across various applications.

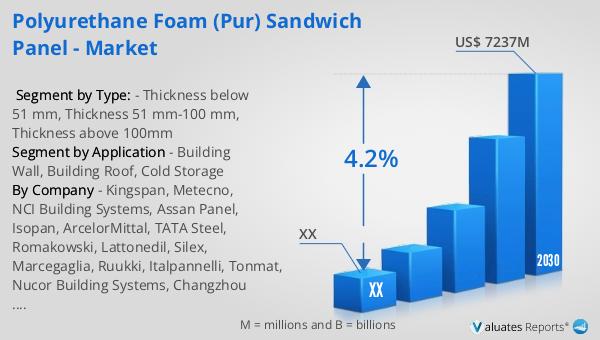

Polyurethane Foam (PUR) Sandwich Panel - Global Market Outlook:

The global market for Polyurethane Foam (PUR) Sandwich Panels was valued at approximately $5,448 million in 2023. It is projected to grow to a revised size of around $7,237 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.2% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for energy-efficient and sustainable building materials across various industries. In North America, the market for PUR Sandwich Panels was valued at a significant amount in 2023, with expectations of reaching a higher value by 2030, supported by a steady CAGR throughout the forecast period. The growth in this region is attributed to the rising adoption of these panels in construction projects, driven by stringent building codes and the need for improved energy efficiency. As the construction industry continues to evolve, the demand for materials that offer both performance and environmental benefits is expected to drive the market for PUR Sandwich Panels, making them a critical component in modern building practices.

| Report Metric | Details |

| Report Name | Polyurethane Foam (PUR) Sandwich Panel - Market |

| Forecasted market size in 2030 | US$ 7237 million |

| CAGR | 4.2% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kingspan, Metecno, NCI Building Systems, Assan Panel, Isopan, ArcelorMittal, TATA Steel, Romakowski, Lattonedil, Silex, Marcegaglia, Ruukki, Italpannelli, Tonmat, Nucor Building Systems, Changzhou Jingxue, Alubel, Zhongjie Group, BCOMS, TENAX PANEL |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |