What is Hydroxypropyl Methylcellulose (HPMC) Capsules - Global Market?

Hydroxypropyl Methylcellulose (HPMC) capsules are a significant innovation in the global market, primarily used as an alternative to traditional gelatin capsules. These capsules are derived from cellulose, a natural polymer found in plant cell walls, making them suitable for vegetarians and vegans. HPMC capsules are known for their stability, resistance to moisture, and ability to encapsulate a wide range of substances, including pharmaceuticals, nutraceuticals, and dietary supplements. The global market for HPMC capsules is driven by the increasing demand for plant-based and allergen-free products, as well as the growing awareness of health and wellness among consumers. Additionally, these capsules offer advantages such as low moisture content, which enhances the shelf life of the encapsulated products. The market is also influenced by the rising trend of clean-label products, where consumers prefer products with minimal and recognizable ingredients. As a result, HPMC capsules are gaining popularity across various industries, contributing to their expanding market presence worldwide.

Pectin, Carrageenan, Glycerin, Gellan gum, Others in the Hydroxypropyl Methylcellulose (HPMC) Capsules - Global Market:

In the context of Hydroxypropyl Methylcellulose (HPMC) capsules, several other substances play a crucial role in the global market, including pectin, carrageenan, glycerin, and gellan gum. Pectin, a natural polysaccharide found in fruits, is often used as a gelling agent in food products. In the realm of HPMC capsules, pectin can be utilized to enhance the texture and stability of the capsules, making them more appealing to consumers who seek plant-based alternatives. Carrageenan, derived from red seaweed, is another polysaccharide that serves as a gelling, thickening, and stabilizing agent. Its application in HPMC capsules is particularly beneficial for improving the mechanical strength and thermal stability of the capsules, ensuring they maintain their integrity during processing and storage. Glycerin, a simple polyol compound, is commonly used as a plasticizer in capsule formulations. In HPMC capsules, glycerin helps to improve flexibility and reduce brittleness, which is essential for maintaining the capsules' structural integrity. Gellan gum, a water-soluble polysaccharide produced by bacterial fermentation, is used as a gelling agent and stabilizer. In the context of HPMC capsules, gellan gum can enhance the capsules' ability to encapsulate a wide range of substances, including those with varying pH levels and solubility profiles. The inclusion of these substances in HPMC capsules not only improves their functional properties but also aligns with the growing consumer demand for natural and sustainable ingredients. As the global market for HPMC capsules continues to expand, the role of these complementary substances becomes increasingly important, driving innovation and development in capsule formulations. The integration of pectin, carrageenan, glycerin, and gellan gum into HPMC capsules reflects the industry's commitment to meeting consumer preferences for clean-label, plant-based, and environmentally friendly products. This trend is expected to continue as manufacturers seek to differentiate their products in a competitive market, offering consumers a wider range of options that align with their values and dietary preferences.

Pharmaceuticals, Food, Neutraceuticals, Dentistry, Cosmetics, Others in the Hydroxypropyl Methylcellulose (HPMC) Capsules - Global Market:

Hydroxypropyl Methylcellulose (HPMC) capsules have found extensive usage across various sectors, including pharmaceuticals, food, nutraceuticals, dentistry, cosmetics, and others. In the pharmaceutical industry, HPMC capsules are widely used for encapsulating drugs and active pharmaceutical ingredients (APIs). Their stability and resistance to moisture make them ideal for protecting sensitive compounds, ensuring the efficacy and safety of medications. Additionally, HPMC capsules are preferred for their ability to dissolve quickly in the gastrointestinal tract, facilitating the rapid release and absorption of the encapsulated drugs. In the food industry, HPMC capsules are used to encapsulate flavors, colors, and other food additives, providing a convenient and efficient delivery system. Their plant-based origin and allergen-free nature make them suitable for a wide range of dietary preferences, including vegetarian and vegan diets. In the nutraceutical sector, HPMC capsules are popular for encapsulating vitamins, minerals, and herbal supplements. Their low moisture content and stability help preserve the potency and shelf life of these products, ensuring consumers receive the intended health benefits. In dentistry, HPMC capsules are used in the formulation of dental materials, such as impression materials and adhesives. Their biocompatibility and ease of use make them a preferred choice for dental applications. In the cosmetics industry, HPMC capsules are used to encapsulate active ingredients in skincare and personal care products. Their ability to protect sensitive compounds from degradation and enhance the delivery of active ingredients to the skin makes them valuable in cosmetic formulations. Beyond these sectors, HPMC capsules are also used in other applications, such as agriculture and animal feed, where their stability and versatility offer significant advantages. Overall, the diverse applications of HPMC capsules across various industries highlight their importance in the global market, driven by the demand for innovative and sustainable solutions.

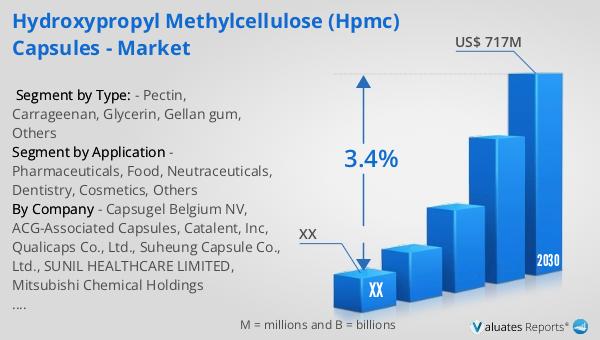

Hydroxypropyl Methylcellulose (HPMC) Capsules - Global Market Outlook:

The global market for Hydroxypropyl Methylcellulose (HPMC) capsules was valued at approximately $563.4 million in 2023. It is projected to grow to a revised size of $717 million by 2030, with a compound annual growth rate (CAGR) of 3.4% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for HPMC capsules across various industries, driven by consumer preferences for plant-based and allergen-free products. The market is particularly strong in North America and Europe, which together account for over 53% of the global market share. This significant market presence in these regions can be attributed to the high level of consumer awareness and the growing trend of clean-label products. As consumers become more health-conscious and environmentally aware, the demand for HPMC capsules is expected to continue to rise, further driving market growth. The market outlook for HPMC capsules reflects the broader trends in the global market, where sustainability, innovation, and consumer preferences are key drivers of growth. As manufacturers continue to develop new formulations and applications for HPMC capsules, the market is poised for continued expansion, offering opportunities for growth and innovation in the coming years.

| Report Metric | Details |

| Report Name | Hydroxypropyl Methylcellulose (HPMC) Capsules - Market |

| Forecasted market size in 2030 | US$ 717 million |

| CAGR | 3.4% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Capsugel Belgium NV, ACG-Associated Capsules, Catalent, Inc, Qualicaps Co., Ltd., Suheung Capsule Co., Ltd., SUNIL HEALTHCARE LIMITED, Mitsubishi Chemical Holdings Corporation, ACG World, Encap |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |