What is Metallic Expansion Joints - Global Market?

Metallic expansion joints are essential components in various industrial applications, designed to absorb thermal expansion and contraction in piping systems. These joints are typically made from stainless steel or other durable metals, allowing them to withstand high temperatures and pressures. The global market for metallic expansion joints is driven by their critical role in maintaining the integrity and efficiency of pipelines, especially in industries where temperature fluctuations are common. These joints help prevent damage to pipes by accommodating movement, reducing stress, and minimizing the risk of leaks or ruptures. As industries continue to expand and modernize, the demand for reliable and efficient piping solutions like metallic expansion joints is expected to grow. This market encompasses a wide range of products, each tailored to specific industrial needs, ensuring that systems operate smoothly and safely. The versatility and durability of metallic expansion joints make them indispensable in sectors such as power generation, petrochemicals, and heavy industry, where they contribute to operational efficiency and safety. As a result, the global market for these components is poised for continued growth, driven by technological advancements and increasing industrialization worldwide.

Axial, Angular, Lateral in the Metallic Expansion Joints - Global Market:

Metallic expansion joints are categorized based on their movement capabilities, primarily axial, angular, and lateral movements, each serving distinct functions in industrial applications. Axial expansion joints are designed to accommodate changes in the length of a pipeline due to thermal expansion or contraction. These joints are crucial in systems where pipes experience significant temperature variations, as they allow for linear movement along the pipe's axis. By absorbing this movement, axial expansion joints help prevent stress and potential damage to the piping system. They are commonly used in power plants, refineries, and chemical processing facilities, where temperature fluctuations are frequent and can be substantial. Angular expansion joints, on the other hand, are engineered to handle angular deflection, allowing pipes to bend or pivot at specific points. This capability is essential in systems where pipes need to navigate around obstacles or change direction without compromising structural integrity. Angular expansion joints are often employed in complex piping networks, such as those found in petrochemical plants and large industrial facilities, where flexibility and adaptability are crucial. Lateral expansion joints are designed to accommodate lateral movement, allowing pipes to shift sideways. This type of movement is particularly important in systems where pipes are subject to external forces, such as seismic activity or ground settlement. Lateral expansion joints help maintain the alignment and stability of the piping system, preventing misalignment and potential damage. They are commonly used in infrastructure projects, such as bridges and tunnels, where external forces can impact the integrity of the piping network. Each type of metallic expansion joint plays a vital role in ensuring the safe and efficient operation of industrial systems, providing the necessary flexibility to accommodate various movements and stresses. As industries continue to evolve and face new challenges, the demand for specialized expansion joints that can meet specific requirements is expected to increase. This growth is driven by the need for reliable and adaptable solutions that can enhance the performance and longevity of piping systems in diverse industrial environments.

Power Engineering, Petrochemical, Heavy Industry, Others in the Metallic Expansion Joints - Global Market:

Metallic expansion joints are widely used across various industries due to their ability to absorb thermal expansion and contraction, ensuring the integrity and efficiency of piping systems. In power engineering, these joints are crucial for maintaining the safety and reliability of power plants. They are used in steam and gas turbines, boilers, and heat exchangers, where they accommodate thermal movements and reduce stress on the piping systems. By preventing leaks and minimizing wear and tear, metallic expansion joints help extend the lifespan of equipment and reduce maintenance costs. In the petrochemical industry, metallic expansion joints are essential for handling the complex piping networks that transport various chemicals and gases. These joints provide the necessary flexibility to accommodate temperature fluctuations and pressure changes, ensuring the safe and efficient operation of refineries and chemical plants. They help prevent leaks and ruptures, which can lead to costly downtime and environmental hazards. In heavy industry, metallic expansion joints are used in applications such as steel mills, cement plants, and mining operations. These joints help manage the thermal expansion of large-scale equipment and piping systems, reducing the risk of structural damage and improving operational efficiency. By absorbing vibrations and accommodating movement, metallic expansion joints contribute to the smooth operation of heavy machinery and equipment. Beyond these industries, metallic expansion joints are also used in various other applications, such as HVAC systems, shipbuilding, and infrastructure projects. Their versatility and durability make them suitable for a wide range of environments, where they help maintain the integrity and performance of piping systems. As industries continue to grow and evolve, the demand for reliable and efficient expansion joints is expected to increase, driving innovation and development in the global market.

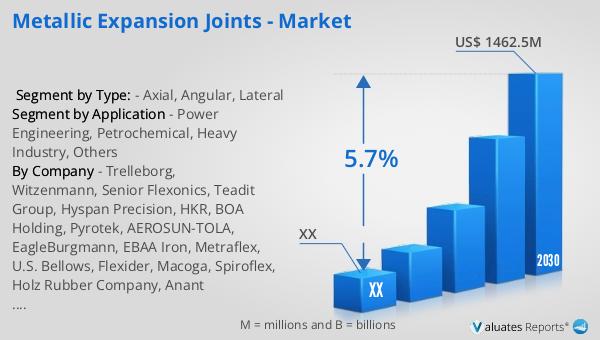

Metallic Expansion Joints - Global Market Outlook:

In 2023, the global market for metallic expansion joints was valued at approximately US$ 984.2 million. This market is projected to grow significantly, reaching an estimated size of US$ 1462.5 million by 2030, with a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2024 to 2030. Europe currently holds the largest share of the metallic expansion joints market, accounting for about 33% of the total market share. This dominance is attributed to the region's well-established industrial base and the high demand for advanced piping solutions in various sectors. Additionally, the top three companies in the metallic expansion joints market collectively occupy around 25% of the market share, highlighting the competitive nature of the industry. These leading companies are at the forefront of innovation, continuously developing new products and technologies to meet the evolving needs of their customers. As the global market for metallic expansion joints continues to expand, driven by increasing industrialization and technological advancements, companies are focusing on enhancing their product offerings and expanding their geographical presence to capture a larger share of the market. This growth presents significant opportunities for both established players and new entrants, as the demand for reliable and efficient piping solutions continues to rise across various industries worldwide.

| Report Metric | Details |

| Report Name | Metallic Expansion Joints - Market |

| Forecasted market size in 2030 | US$ 1462.5 million |

| CAGR | 5.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Trelleborg, Witzenmann, Senior Flexonics, Teadit Group, Hyspan Precision, HKR, BOA Holding, Pyrotek, AEROSUN-TOLA, EagleBurgmann, EBAA Iron, Metraflex, U.S. Bellows, Flexider, Macoga, Spiroflex, Holz Rubber Company, Anant Engineering & Fabricators, Osaka Rasenkan Kogyo, Kadant Unaflex, Microflex, Flexicraft Industries, Tofle, Viking Johnson, Romac Industries, Ditec, Teddington Engineered |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |