What is Global Anti-Counterfeit Electronics and Automobiles Packaging Market?

The Global Anti-Counterfeit Electronics and Automobiles Packaging Market is a specialized sector focused on developing and implementing packaging solutions to prevent the counterfeiting of electronic and automotive products. Counterfeiting is a significant issue that affects the integrity and safety of products, leading to financial losses and potential safety hazards for consumers. This market encompasses a range of technologies and strategies designed to authenticate genuine products and trace their origins throughout the supply chain. By employing advanced packaging techniques, companies aim to protect their brands, ensure consumer safety, and comply with regulatory standards. The market is driven by the increasing demand for secure packaging solutions in the electronics and automotive industries, where the authenticity of components is crucial for performance and safety. As technology evolves, the market continues to innovate, offering more sophisticated and reliable anti-counterfeit measures. These solutions not only help in safeguarding products but also enhance consumer trust and brand reputation. The market's growth is fueled by the rising awareness of counterfeit risks and the need for robust protection mechanisms in a globalized economy.

Authentication Technology, Trace Technology in the Global Anti-Counterfeit Electronics and Automobiles Packaging Market:

Authentication Technology and Trace Technology are two pivotal components of the Global Anti-Counterfeit Electronics and Automobiles Packaging Market. Authentication Technology involves the use of various methods to verify the authenticity of a product. This can include holograms, watermarks, and digital codes that are difficult to replicate. These technologies are integrated into the packaging to provide a visible or hidden mark of authenticity, ensuring that consumers and retailers can easily identify genuine products. The use of such technologies is crucial in the electronics and automotive sectors, where counterfeit components can lead to significant safety risks and financial losses. On the other hand, Trace Technology focuses on tracking the product throughout its supply chain journey. This involves the use of barcodes, RFID tags, and QR codes that store information about the product's origin, manufacturing process, and distribution path. By implementing trace technology, companies can monitor their products in real-time, ensuring that they reach their intended destination without being tampered with or replaced by counterfeit items. This technology not only aids in preventing counterfeiting but also enhances supply chain transparency and efficiency. Both Authentication and Trace Technologies work in tandem to provide a comprehensive anti-counterfeit solution. While authentication ensures the product's genuineness, trace technology provides a detailed account of its journey, making it easier to identify and address any discrepancies. The integration of these technologies into packaging solutions is becoming increasingly sophisticated, with advancements in digital technology paving the way for more secure and reliable methods. For instance, blockchain technology is being explored as a means to create an immutable record of a product's journey, further enhancing traceability and authenticity. The adoption of these technologies is driven by the growing awareness of the risks associated with counterfeit products and the need for robust protection mechanisms. As the market continues to evolve, companies are investing in research and development to create innovative solutions that can effectively combat counterfeiting. This includes the development of smart packaging solutions that incorporate sensors and IoT devices to provide real-time data on the product's condition and location. The use of such advanced technologies not only helps in preventing counterfeiting but also adds value to the product by enhancing its safety and reliability. In conclusion, Authentication and Trace Technologies are integral to the Global Anti-Counterfeit Electronics and Automobiles Packaging Market. They provide a multi-layered approach to combating counterfeiting, ensuring that products are genuine and traceable throughout their lifecycle. As technology continues to advance, these solutions are becoming more sophisticated, offering greater protection and peace of mind for consumers and manufacturers alike.

Two Wheelers, Passenger Cars, Commercial Vehicles in the Global Anti-Counterfeit Electronics and Automobiles Packaging Market:

The usage of Global Anti-Counterfeit Electronics and Automobiles Packaging Market solutions is particularly significant in the areas of Two Wheelers, Passenger Cars, and Commercial Vehicles. In the realm of Two Wheelers, the market plays a crucial role in ensuring the authenticity of various components such as engines, brakes, and electronic systems. Counterfeit parts in two-wheelers can lead to severe safety risks, including brake failure and engine malfunctions. By employing anti-counterfeit packaging solutions, manufacturers can safeguard their products and ensure that consumers receive genuine and reliable components. This not only enhances the safety and performance of two-wheelers but also builds consumer trust in the brand. In the Passenger Cars segment, the market's solutions are vital in protecting a wide range of components, from electronic systems to mechanical parts. The complexity of modern passenger cars, with their advanced electronic and safety systems, makes them particularly vulnerable to counterfeiting. Anti-counterfeit packaging solutions help in verifying the authenticity of these components, ensuring that they meet the required safety and performance standards. This is crucial for maintaining the integrity of the vehicle and ensuring the safety of passengers. Additionally, these solutions aid in protecting the brand's reputation by preventing counterfeit products from entering the market. In the Commercial Vehicles sector, the market's solutions are essential in safeguarding critical components such as engines, transmissions, and electronic control systems. Commercial vehicles, which are often used for transporting goods and passengers, require high levels of reliability and safety. Counterfeit parts can compromise the vehicle's performance and safety, leading to potential accidents and financial losses. By implementing anti-counterfeit packaging solutions, manufacturers can ensure that their products are genuine and meet the necessary quality standards. This not only enhances the safety and reliability of commercial vehicles but also reduces the risk of costly recalls and repairs. Overall, the Global Anti-Counterfeit Electronics and Automobiles Packaging Market plays a vital role in ensuring the authenticity and safety of components in Two Wheelers, Passenger Cars, and Commercial Vehicles. By providing robust packaging solutions, the market helps in preventing counterfeiting, protecting brand reputation, and ensuring consumer safety. As the automotive industry continues to evolve, the demand for secure and reliable anti-counterfeit solutions is expected to grow, driving further innovation and development in the market.

Global Anti-Counterfeit Electronics and Automobiles Packaging Market Outlook:

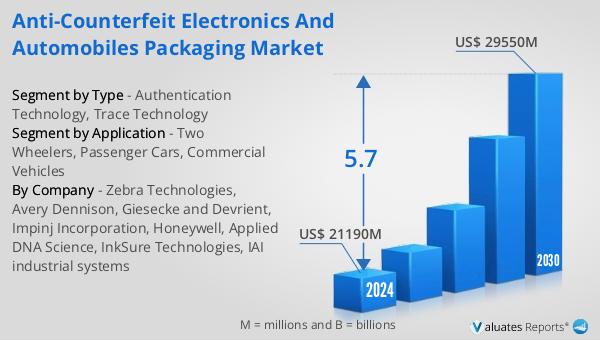

The outlook for the Global Anti-Counterfeit Electronics and Automobiles Packaging Market indicates a promising growth trajectory. The market is anticipated to expand from $21,190 million in 2024 to $29,550 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 5.7% over the forecast period. This growth is driven by the increasing need for secure packaging solutions to combat the rising threat of counterfeiting in the electronics and automotive sectors. As counterfeit products pose significant risks to consumer safety and brand reputation, companies are investing in advanced packaging technologies to ensure product authenticity and traceability. The projected growth underscores the importance of anti-counterfeit measures in safeguarding products and enhancing consumer trust. With the continuous evolution of technology, the market is expected to witness the development of more sophisticated and reliable solutions, further boosting its growth prospects. The increasing awareness of counterfeit risks and the need for robust protection mechanisms are key factors contributing to the market's expansion. As companies strive to protect their brands and ensure consumer safety, the demand for innovative anti-counterfeit packaging solutions is set to rise, driving the market's growth in the coming years.

| Report Metric | Details |

| Report Name | Anti-Counterfeit Electronics and Automobiles Packaging Market |

| Accounted market size in 2024 | US$ 21190 in million |

| Forecasted market size in 2030 | US$ 29550 million |

| CAGR | 5.7 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Segment by Region |

|

| By Company | Zebra Technologies, Avery Dennison, Giesecke and Devrient, Impinj Incorporation, Honeywell, Applied DNA Science, InkSure Technologies, IAI industrial systems |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |