What is Coordinate Measuring Machines - Global Market?

Coordinate Measuring Machines (CMMs) are sophisticated devices used in the field of metrology to measure the physical geometrical characteristics of an object. These machines are pivotal in ensuring precision and accuracy in manufacturing processes across various industries. The global market for CMMs is witnessing significant growth due to the increasing demand for high-quality products and the need for precise measurements in manufacturing. CMMs come in various types, including bridge, gantry, and horizontal arm, each designed for specific applications and measurement needs. The versatility of CMMs allows them to be used in a wide range of industries, from automotive to aerospace, where precise measurements are crucial. The integration of advanced technologies such as software enhancements and automation has further propelled the adoption of CMMs globally. As industries continue to evolve and demand higher precision, the role of CMMs in quality control and assurance becomes increasingly important. The global market for CMMs is poised for growth, driven by technological advancements and the need for precision in manufacturing processes.

CNC, Manually-Controlled in the Coordinate Measuring Machines - Global Market:

CNC (Computer Numerical Control) and manually-controlled coordinate measuring machines are two primary types of CMMs used in the global market, each with distinct features and applications. CNC CMMs are automated systems that use computer software to control the movement of the measuring probe, allowing for high precision and repeatability in measurements. These machines are ideal for complex and repetitive measurement tasks, as they can be programmed to perform specific measurement routines without human intervention. The automation of CNC CMMs reduces the likelihood of human error, increases efficiency, and allows for the measurement of intricate geometries that would be challenging to measure manually. On the other hand, manually-controlled CMMs require an operator to manually guide the probe to the points of interest on the object being measured. While these machines may not offer the same level of precision and speed as CNC CMMs, they are often more cost-effective and suitable for smaller operations or less complex measurement tasks. Manually-controlled CMMs provide flexibility and are often used in situations where the measurement task is straightforward or when the cost of a CNC machine cannot be justified. The choice between CNC and manually-controlled CMMs depends on various factors, including the complexity of the measurement task, the required precision, the volume of measurements, and budget constraints. In the global market, CNC CMMs are gaining popularity due to their ability to handle complex measurements with high accuracy and efficiency. However, manually-controlled CMMs continue to hold a significant share of the market, particularly in regions or industries where cost is a major consideration. The global market for CMMs is characterized by a diverse range of products catering to different needs and applications, with manufacturers continuously innovating to improve the capabilities and performance of both CNC and manually-controlled machines. As technology advances, the line between CNC and manually-controlled CMMs is becoming increasingly blurred, with many modern machines offering a combination of both manual and automated features. This hybrid approach allows users to benefit from the precision and efficiency of CNC systems while retaining the flexibility and cost-effectiveness of manual control. The global market for CMMs is expected to continue evolving, driven by the need for precision and efficiency in manufacturing processes across various industries.

Automotive Industry, Equipment Manufacturing, Aeronautical Industry, Others in the Coordinate Measuring Machines - Global Market:

Coordinate Measuring Machines (CMMs) play a crucial role in various industries, including the automotive, equipment manufacturing, aeronautical, and others, by ensuring precision and quality in the production process. In the automotive industry, CMMs are used extensively for inspecting and measuring components to ensure they meet the stringent quality standards required for vehicle safety and performance. The ability of CMMs to provide accurate and repeatable measurements makes them indispensable in the production of complex automotive parts, such as engine components, transmission systems, and body panels. In equipment manufacturing, CMMs are used to verify the dimensions and tolerances of machinery parts, ensuring they fit together correctly and function as intended. The precision offered by CMMs helps manufacturers maintain high-quality standards and reduce the risk of defects, leading to improved product reliability and customer satisfaction. In the aeronautical industry, where precision and safety are paramount, CMMs are used to measure and inspect critical components such as turbine blades, fuselage sections, and landing gear. The ability of CMMs to measure complex geometries with high accuracy is essential in ensuring the safety and performance of aircraft. Beyond these industries, CMMs are also used in sectors such as electronics, medical devices, and consumer goods, where precision and quality are critical. The versatility of CMMs allows them to be adapted for various applications, making them a valuable tool in any industry that requires precise measurements. As industries continue to demand higher precision and quality, the role of CMMs in ensuring product integrity and performance becomes increasingly important. The global market for CMMs is expected to grow as more industries recognize the benefits of using these machines to enhance their manufacturing processes and improve product quality.

Coordinate Measuring Machines - Global Market Outlook:

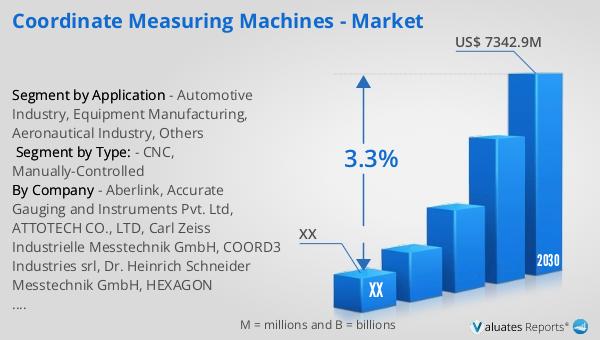

In 2023, the global market for Coordinate Measuring Machines was valued at approximately US$ 5,842 million. This market is projected to expand to a revised size of US$ 7,342.9 million by the year 2030, reflecting a compound annual growth rate (CAGR) of 3.3% during the forecast period from 2024 to 2030. Europe stands out as the leading manufacturing region, accounting for about 28% of the market share. This growth trajectory indicates a steady increase in demand for CMMs, driven by advancements in technology and the need for precision in various industries. The European market's dominance can be attributed to the region's strong industrial base and emphasis on quality and precision in manufacturing processes. As industries continue to evolve and demand higher precision, the role of CMMs in quality control and assurance becomes increasingly important. The global market for CMMs is poised for growth, driven by technological advancements and the need for precision in manufacturing processes. The increasing adoption of CMMs across various industries, including automotive, aerospace, and equipment manufacturing, is expected to contribute to the market's expansion. As manufacturers seek to improve product quality and reduce defects, the demand for CMMs is likely to continue growing, further driving the market's growth.

| Report Metric | Details |

| Report Name | Coordinate Measuring Machines - Market |

| Forecasted market size in 2030 | US$ 7342.9 million |

| CAGR | 3.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Aberlink, Accurate Gauging and Instruments Pvt. Ltd, ATTOTECH CO., LTD, Carl Zeiss Industrielle Messtechnik GmbH, COORD3 Industries srl, Dr. Heinrich Schneider Messtechnik GmbH, HEXAGON MANUFACTURING INTELLIGENCE, Innovalia-Metrology, MITUTOYO, Optical Gaging Products, Stiefelmayer, TARUS, Tesa, THOME, Walter Maschinenbau, WENZEL, WERTH MESSTECHNIK |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |