What is Global MEMS Active Resonator Market?

The Global MEMS Active Resonator Market refers to the market for Micro-Electro-Mechanical Systems (MEMS) active resonators, which are tiny devices that use mechanical vibrations to generate precise frequencies. These resonators are crucial components in various electronic devices, providing stable and accurate frequency references. MEMS technology allows these resonators to be extremely small, reliable, and energy-efficient, making them ideal for modern applications. The market encompasses the production, distribution, and utilization of these resonators across different industries, including telecommunications, automotive, and consumer electronics. As technology advances and the demand for more compact and efficient electronic devices grows, the Global MEMS Active Resonator Market is expected to expand significantly, driven by innovations and increasing applications in various fields.

Series Resonance Type, Parallel Resonance Type in the Global MEMS Active Resonator Market:

In the Global MEMS Active Resonator Market, there are two primary types of resonators: Series Resonance Type and Parallel Resonance Type. Series Resonance Type resonators operate by creating a condition where the inductive and capacitive reactances cancel each other out, resulting in a minimal impedance path at a specific frequency. This type is often used in applications requiring high precision and stability, such as in communication devices and high-frequency oscillators. On the other hand, Parallel Resonance Type resonators work by creating a condition where the inductive and capacitive reactances are equal but opposite, resulting in a high impedance path at a specific frequency. This type is typically used in filter circuits and frequency selection applications. Both types of resonators are integral to the functioning of various electronic devices, providing the necessary frequency stability and accuracy required in modern technology. The choice between series and parallel resonance types depends on the specific requirements of the application, such as the desired frequency range, stability, and power consumption. As the demand for more advanced and efficient electronic devices continues to grow, the Global MEMS Active Resonator Market is expected to see increased adoption of both series and parallel resonance types, driven by their unique advantages and applications.

5G Field, IoT Field, Automotive Field, Others in the Global MEMS Active Resonator Market:

The Global MEMS Active Resonator Market finds extensive usage in several key areas, including the 5G field, IoT field, automotive field, and others. In the 5G field, MEMS active resonators are crucial for providing the high-frequency stability and precision required for 5G networks. These resonators help ensure reliable communication and data transfer, supporting the high-speed and low-latency requirements of 5G technology. In the IoT field, MEMS active resonators are used in various IoT devices to provide accurate timing and frequency references, enabling seamless connectivity and data synchronization among devices. The small size and low power consumption of MEMS resonators make them ideal for IoT applications, where compactness and energy efficiency are critical. In the automotive field, MEMS active resonators are used in various electronic systems, including navigation, communication, and safety systems. These resonators provide the necessary frequency stability and precision required for the reliable operation of automotive electronics. Additionally, MEMS active resonators are used in other fields, such as consumer electronics, healthcare, and industrial applications, where precise frequency control and stability are essential. The versatility and reliability of MEMS active resonators make them indispensable in modern technology, driving their widespread adoption across various industries.

Global MEMS Active Resonator Market Outlook:

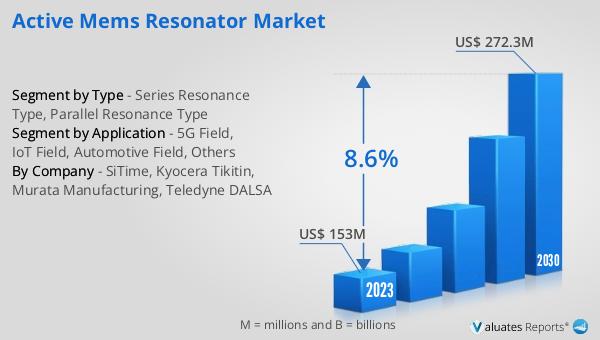

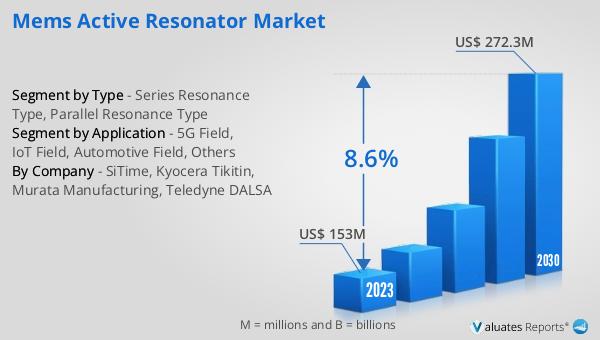

The global MEMS Active Resonator market was valued at US$ 153 million in 2023 and is anticipated to reach US$ 272.3 million by 2030, witnessing a CAGR of 8.6% during the forecast period 2024-2030. This significant growth is driven by the increasing demand for compact, reliable, and energy-efficient electronic devices across various industries. As technology continues to advance, the need for precise frequency control and stability becomes more critical, further propelling the adoption of MEMS active resonators. The market's expansion is also supported by the growing applications of MEMS resonators in emerging fields such as 5G, IoT, and automotive electronics. With their unique advantages, including small size, low power consumption, and high precision, MEMS active resonators are poised to play a crucial role in the future of electronic devices and systems.

| Report Metric | Details |

| Report Name | MEMS Active Resonator Market |

| Accounted market size in 2023 | US$ 153 million |

| Forecasted market size in 2030 | US$ 272.3 million |

| CAGR | 8.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | SiTime, Kyocera Tikitin, Murata Manufacturing, Teledyne DALSA |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |