What is Global Auto Retractable Box Cutters Market?

The Global Auto Retractable Box Cutters Market refers to the worldwide industry focused on the production, distribution, and sale of box cutters that feature an automatic retractable blade mechanism. These tools are designed to enhance safety by automatically retracting the blade when not in use, reducing the risk of accidental cuts and injuries. The market encompasses a variety of products tailored for different applications, including packaging, shipping, warehousing, retail, construction, and general office use. The demand for these safety-enhanced tools is driven by the increasing emphasis on workplace safety and efficiency across various industries. As businesses and consumers alike become more aware of the benefits of using safer cutting tools, the market for auto retractable box cutters continues to grow. This market includes a range of products from basic models to more advanced versions with additional features such as ergonomic designs, adjustable blade lengths, and durable materials. The global reach of this market means that these products are available and utilized in numerous countries, catering to a diverse set of needs and preferences.

Carbon Steel Blades, Stainless Steel Blades, Ceramic Blades, Other in the Global Auto Retractable Box Cutters Market:

In the Global Auto Retractable Box Cutters Market, the types of blades used play a crucial role in determining the performance and suitability of the cutters for various tasks. Carbon steel blades are known for their sharpness and durability. They are often preferred for heavy-duty cutting tasks because they can maintain a sharp edge for a longer period. However, they are prone to rust if not properly maintained, which can be a drawback in environments where moisture is present. Stainless steel blades, on the other hand, offer a good balance between sharpness and corrosion resistance. They are less likely to rust, making them ideal for use in humid or wet conditions. These blades are commonly used in settings where hygiene is a priority, such as in food packaging and medical supplies. Ceramic blades are another option available in the market. These blades are extremely hard and maintain their sharpness longer than metal blades. They are also non-conductive and chemically inert, which makes them suitable for specialized applications where metal blades might not be appropriate. However, ceramic blades can be more brittle and prone to chipping compared to their metal counterparts. Other types of blades include those made from specialized alloys or coated with materials to enhance their performance. These blades might offer unique benefits such as increased wear resistance or reduced friction, catering to specific needs in various industries. The choice of blade material can significantly impact the efficiency, safety, and longevity of the auto retractable box cutters, making it an important consideration for both manufacturers and users.

Packaging and Shipping, Warehouse and Logistics, Retail and Merchandising, Construction and Maintenance, Office and General Use, Others in the Global Auto Retractable Box Cutters Market:

The usage of Global Auto Retractable Box Cutters spans across several key areas, each with its unique requirements and benefits. In packaging and shipping, these cutters are indispensable tools for opening and sealing boxes, cutting packing materials, and preparing shipments. The automatic retraction feature enhances safety, reducing the risk of injuries during the fast-paced activities typical in these environments. In warehouse and logistics operations, auto retractable box cutters are used for tasks such as breaking down boxes, cutting strapping, and handling various packaging materials. The efficiency and safety provided by these tools help in maintaining smooth and accident-free operations. In retail and merchandising, these cutters are essential for tasks like opening stock, preparing displays, and managing inventory. The safety features are particularly important in retail settings where employees may not have specialized training in handling cutting tools. In construction and maintenance, auto retractable box cutters are used for cutting materials like drywall, insulation, and flooring. The durability and safety of these tools make them suitable for the demanding conditions of construction sites. For office and general use, these cutters are handy for everyday tasks such as opening mail, cutting paper, and handling office supplies. The convenience and safety of auto retractable blades make them a preferred choice in office environments. Other areas where these cutters are used include arts and crafts, DIY projects, and various industrial applications. The versatility and safety of auto retractable box cutters make them valuable tools across a wide range of activities, contributing to their growing popularity in the global market.

Global Auto Retractable Box Cutters Market Outlook:

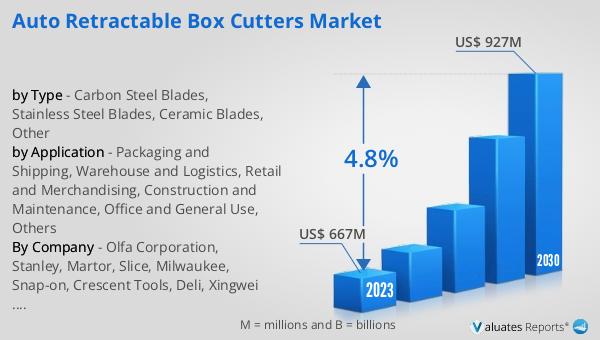

The global Auto Retractable Box Cutters market was valued at US$ 667 million in 2023 and is anticipated to reach US$ 927 million by 2030, witnessing a CAGR of 4.8% during the forecast period from 2024 to 2030. This significant growth reflects the increasing demand for safer and more efficient cutting tools across various industries. The market's expansion is driven by factors such as the rising awareness of workplace safety, the need for efficient packaging and shipping solutions, and the growing adoption of these tools in diverse sectors including retail, construction, and logistics. The automatic retraction feature of these box cutters addresses a critical need for safety, reducing the risk of accidental injuries and enhancing overall productivity. As businesses continue to prioritize safety and efficiency, the demand for auto retractable box cutters is expected to grow, contributing to the market's robust growth trajectory. The market's valuation and projected growth underscore the importance of these tools in modern industrial and commercial operations, highlighting their role in promoting safer and more efficient work environments.

| Report Metric | Details |

| Report Name | Auto Retractable Box Cutters Market |

| Accounted market size in 2023 | US$ 667 million |

| Forecasted market size in 2030 | US$ 927 million |

| CAGR | 4.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Olfa Corporation, Stanley, Martor, Slice, Milwaukee, Snap-on, Crescent Tools, Deli, Xingwei Cutting-Tools Technology, Pacific Handy Cutter |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |