What is Global Intelligent Hybrid Inverter Market?

The Global Intelligent Hybrid Inverter Market refers to the worldwide industry focused on the development, production, and distribution of intelligent hybrid inverters. These inverters are advanced devices that combine the functionalities of traditional inverters with smart technology to optimize energy usage. They are capable of managing multiple power sources, such as solar panels, batteries, and the grid, to ensure efficient energy distribution and storage. The intelligent aspect of these inverters allows for real-time monitoring and control, enhancing their efficiency and reliability. This market is driven by the increasing demand for renewable energy solutions, the need for energy efficiency, and the growing adoption of smart grid technologies. As more countries and industries shift towards sustainable energy practices, the demand for intelligent hybrid inverters is expected to rise, making this market a crucial component of the global energy landscape.

Low Voltage Hybrid Inverter, High Voltage Hybrid Inverter in the Global Intelligent Hybrid Inverter Market:

Low Voltage Hybrid Inverters and High Voltage Hybrid Inverters are two primary types of products within the Global Intelligent Hybrid Inverter Market. Low Voltage Hybrid Inverters typically operate at voltages below 48V and are commonly used in residential and small commercial applications. These inverters are designed to manage energy from solar panels and batteries, ensuring that homes and small businesses can efficiently use renewable energy. They are particularly popular in off-grid and backup power systems, where they provide a reliable source of electricity during power outages. On the other hand, High Voltage Hybrid Inverters operate at voltages above 48V and are used in larger commercial and industrial applications. These inverters are capable of handling higher power loads and are often integrated into large-scale solar power systems and energy storage solutions. They are essential for managing the energy needs of factories, large office buildings, and other industrial facilities. Both types of inverters play a crucial role in the transition to renewable energy by enabling efficient energy management and storage. The intelligent features of these inverters, such as real-time monitoring and control, further enhance their performance and reliability. As the demand for renewable energy continues to grow, the market for both low and high voltage hybrid inverters is expected to expand, driven by advancements in technology and increasing awareness of the benefits of sustainable energy solutions.

Split Inverter, All-in-one Energy Storage Solar System in the Global Intelligent Hybrid Inverter Market:

The Global Intelligent Hybrid Inverter Market finds significant usage in various applications, including Split Inverters and All-in-one Energy Storage Solar Systems. Split Inverters are a type of hybrid inverter system where the inverter and battery are separate units. This configuration allows for greater flexibility in system design and installation, making it easier to customize the energy solution to meet specific needs. Split Inverters are widely used in residential and commercial settings, where they help manage energy from solar panels and batteries, ensuring efficient energy use and storage. They are particularly beneficial in areas with frequent power outages, as they provide a reliable backup power source. All-in-one Energy Storage Solar Systems, on the other hand, integrate the inverter, battery, and solar charge controller into a single unit. This compact design simplifies installation and reduces the overall system cost. These systems are ideal for residential and small commercial applications, where space and budget constraints are significant considerations. All-in-one systems offer a seamless solution for managing solar energy generation, storage, and usage, making them an attractive option for homeowners and small business owners looking to adopt renewable energy. Both Split Inverters and All-in-one Energy Storage Solar Systems benefit from the intelligent features of hybrid inverters, such as real-time monitoring and control, which enhance their efficiency and reliability. As the demand for renewable energy solutions continues to grow, the usage of intelligent hybrid inverters in these applications is expected to increase, driven by the need for efficient and reliable energy management systems.

Global Intelligent Hybrid Inverter Market Outlook:

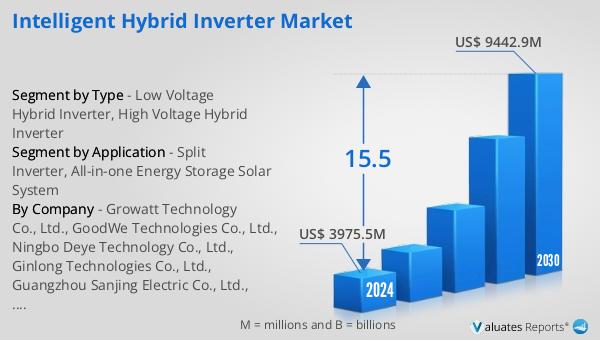

The global Intelligent Hybrid Inverter market is anticipated to expand from US$ 3975.5 million in 2024 to US$ 9442.9 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 15.5% during the forecast period. Europe dominates the market, holding the largest share at approximately 50%, followed by North America with 36%, and Asia-Pacific with 13%. The market is segmented based on battery voltage into low and high voltage hybrid inverters, with low voltage hybrid inverters accounting for over 80% of the market share. In terms of application, split inverters represent the largest segment, comprising over 90% of the market. This robust growth is driven by the increasing adoption of renewable energy solutions and the need for efficient energy management systems. The intelligent features of these inverters, such as real-time monitoring and control, further enhance their appeal, making them a critical component of modern energy systems.

| Report Metric | Details |

| Report Name | Intelligent Hybrid Inverter Market |

| Accounted market size in 2024 | US$ 3975.5 million |

| Forecasted market size in 2030 | US$ 9442.9 million |

| CAGR | 15.5 |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Growatt Technology Co., Ltd., GoodWe Technologies Co., Ltd., Ningbo Deye Technology Co., Ltd., Ginlong Technologies Co., Ltd., Guangzhou Sanjing Electric Co., Ltd., SolaX Power Network Technology (Zhejiang) Co., Ltd., Shenzhen SOFARSOLAR Co., Ltd., Huawei Digital Power Technologies Co., Ltd., AISWEI Technology Co., Ltd, SMA Solar Technology AG, KOSTAL Solar Electric GmbH, SolarEdge Technologies, Inc., KACO new energy GmbH, Fronius International GmbH, Tesla, Inc. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |