What is Global Semiconductor Precision Parts Market?

The Global Semiconductor Precision Parts Market refers to the industry that produces highly specialized components used in the manufacturing of semiconductors. These precision parts are essential for the creation of semiconductor devices, which are the building blocks of modern electronics, including computers, smartphones, and various other digital devices. The market encompasses a wide range of products, including mechanical parts, electrical appliances, mechatronics, gas/liquid/vacuum systems, instrumentation, and optical components. These parts must meet extremely high standards of accuracy and reliability, as even the smallest defect can significantly impact the performance of the final semiconductor product. The demand for these precision parts is driven by the rapid advancements in technology and the increasing complexity of semiconductor devices. As a result, the Global Semiconductor Precision Parts Market is a critical component of the broader semiconductor industry, playing a vital role in enabling the production of cutting-edge electronic devices.

Mechanical, Electrical Appliances, Mechatronics, Gas/Liquid/Vacuum System, Instrumentation, Optical, Others in the Global Semiconductor Precision Parts Market:

The Global Semiconductor Precision Parts Market includes a diverse array of components that are crucial for the manufacturing of semiconductors. Mechanical parts in this market are designed to provide structural support and precise movement within semiconductor manufacturing equipment. These parts must be manufactured with high precision to ensure the accurate alignment and operation of the machinery. Electrical appliances in this market include components such as power supplies, sensors, and actuators that are essential for the functioning of semiconductor manufacturing equipment. These appliances must be highly reliable and capable of operating under the demanding conditions of semiconductor production. Mechatronics, which combines mechanical engineering, electronics, and computer science, plays a significant role in the semiconductor precision parts market. Mechatronic systems are used to automate and control various processes in semiconductor manufacturing, improving efficiency and accuracy. Gas/liquid/vacuum systems are critical for creating the controlled environments needed for semiconductor production. These systems must be capable of maintaining precise pressure and flow rates to ensure the proper functioning of semiconductor manufacturing processes. Instrumentation in this market includes devices used for measuring and monitoring various parameters during semiconductor production. These instruments must be highly accurate and reliable to ensure the quality of the final semiconductor products. Optical components, such as lenses and mirrors, are used in various stages of semiconductor manufacturing, including photolithography and inspection. These components must be manufactured with high precision to ensure the accurate manipulation and measurement of light. Other components in the Global Semiconductor Precision Parts Market include various specialized parts that are essential for specific semiconductor manufacturing processes. These parts must meet stringent quality standards to ensure the reliability and performance of the final semiconductor products.

Photolithography, Etching, Clean, Film Deposition, Others in the Global Semiconductor Precision Parts Market:

The usage of Global Semiconductor Precision Parts Market components spans several critical areas in semiconductor manufacturing, including photolithography, etching, cleaning, film deposition, and other processes. In photolithography, precision parts such as optical lenses, mirrors, and alignment systems are used to project patterns onto semiconductor wafers. These components must be manufactured with extreme accuracy to ensure the precise transfer of patterns, which is crucial for the functionality of the final semiconductor devices. During the etching process, precision parts such as gas delivery systems, vacuum chambers, and etching tools are used to remove specific areas of material from the semiconductor wafer. These components must be capable of maintaining precise control over the etching process to ensure the accurate formation of semiconductor structures. Cleaning processes in semiconductor manufacturing require precision parts such as liquid delivery systems, ultrasonic cleaners, and filtration systems to remove contaminants from the semiconductor wafers. These components must be highly effective at removing even the smallest particles to ensure the quality of the final semiconductor products. Film deposition processes, which involve the application of thin layers of material onto semiconductor wafers, rely on precision parts such as gas flow controllers, deposition chambers, and substrate holders. These components must be capable of maintaining precise control over the deposition process to ensure the uniformity and quality of the deposited films. Other processes in semiconductor manufacturing, such as doping, annealing, and inspection, also rely on a variety of precision parts to ensure the accurate and reliable production of semiconductor devices. These components must meet stringent quality standards to ensure the performance and reliability of the final semiconductor products. Overall, the usage of precision parts in these various processes is essential for the successful manufacturing of semiconductors, enabling the production of advanced electronic devices.

Global Semiconductor Precision Parts Market Outlook:

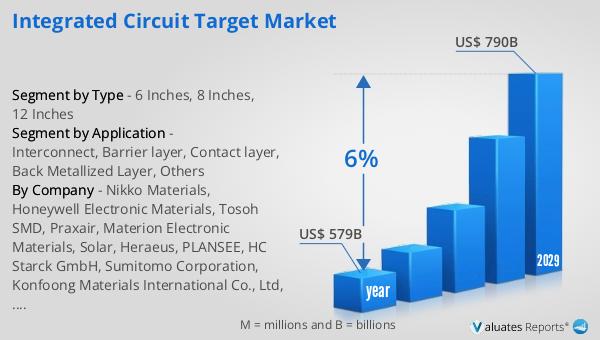

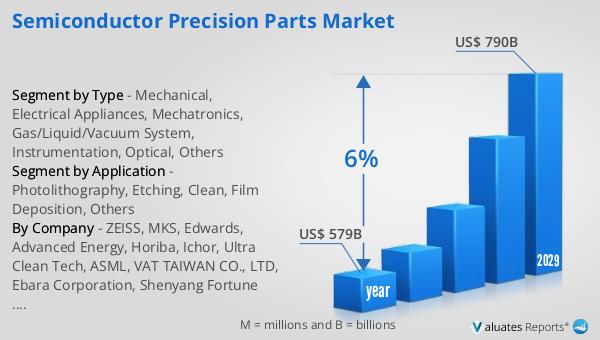

The global market for semiconductors was valued at approximately US$ 579 billion in 2022 and is anticipated to reach around US$ 790 billion by 2029, reflecting a compound annual growth rate (CAGR) of 6% over the forecast period. This growth is driven by the increasing demand for advanced electronic devices, which require highly specialized semiconductor components. The expansion of the semiconductor market underscores the critical role of precision parts in enabling the production of cutting-edge technology. As the complexity of semiconductor devices continues to increase, the demand for high-quality precision parts is expected to grow, further driving the market's expansion. The projected growth of the semiconductor market highlights the importance of ongoing innovation and investment in the development of precision parts to meet the evolving needs of the industry. This growth trajectory also emphasizes the significance of the Global Semiconductor Precision Parts Market in supporting the broader semiconductor industry and enabling the production of advanced electronic devices that are integral to modern life.

| Report Metric | Details |

| Report Name | Semiconductor Precision Parts Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | ZEISS, MKS, Edwards, Advanced Energy, Horiba, Ichor, Ultra Clean Tech, ASML, VAT TAIWAN CO., LTD, Ebara Corporation, Shenyang Fortune Precision Equipment Co., Ltd, SVG Tech Group Co.,Ltd, Kunshan Kinglai Hygienic Materials Co.,Ltd, Konfoong Materials International Co.,Ltd, Suzhou Huaya Intelligence Technology Co., Ltd, Sichuan Injet Electric Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |