What is Global Zinc Rich Marine Coating Market?

The Global Zinc Rich Marine Coating Market is a specialized segment within the broader marine coatings industry, focusing on coatings that contain a high percentage of zinc dust. These coatings are primarily used to protect marine vessels and structures from corrosion, which is a significant concern in the harsh marine environment. Zinc-rich coatings work by providing a sacrificial layer that corrodes in place of the underlying metal, thereby extending the life of the structure. This market is driven by the increasing demand for durable and long-lasting coatings that can withstand the rigors of saltwater exposure, as well as the need for environmentally friendly solutions that comply with stringent regulations. The market encompasses a variety of products, including epoxy and inorganic zinc-rich primers, each offering unique benefits and applications. As global trade and maritime activities continue to grow, the demand for effective marine coatings is expected to rise, making this a dynamic and evolving market. The market is characterized by technological advancements and innovations aimed at improving the performance and sustainability of zinc-rich coatings. Companies operating in this space are continually investing in research and development to enhance their product offerings and meet the diverse needs of their customers.

Epoxy Zinc-rich Primer, Inorganic Zinc-rich Primer in the Global Zinc Rich Marine Coating Market:

Epoxy zinc-rich primers and inorganic zinc-rich primers are two primary types of coatings within the Global Zinc Rich Marine Coating Market, each serving distinct purposes and offering unique advantages. Epoxy zinc-rich primers are formulated with epoxy resins and a high concentration of zinc dust, providing excellent adhesion and corrosion resistance. These primers are particularly valued for their durability and ability to form a tough, protective layer that can withstand mechanical damage and harsh environmental conditions. Epoxy zinc-rich primers are often used as a base coat in multi-layer coating systems, offering a robust foundation that enhances the overall performance of the coating system. They are suitable for a wide range of applications, including ship hulls, offshore platforms, and other marine structures exposed to aggressive environments. The epoxy resin component provides flexibility and impact resistance, making these primers ideal for surfaces that experience frequent movement or stress. On the other hand, inorganic zinc-rich primers are based on silicate binders and also contain a high percentage of zinc dust. These primers offer superior heat resistance and are often used in high-temperature environments where organic coatings may fail. Inorganic zinc-rich primers provide excellent cathodic protection, similar to epoxy primers, but with the added benefit of being able to withstand higher temperatures. This makes them suitable for use on structures such as exhaust stacks, boilers, and other areas exposed to extreme heat. Inorganic zinc-rich primers are also known for their exceptional durability and long service life, making them a cost-effective solution for protecting valuable marine assets. Both types of primers play a crucial role in the Global Zinc Rich Marine Coating Market, offering tailored solutions to meet the specific needs of different marine applications. The choice between epoxy and inorganic zinc-rich primers depends on various factors, including the environmental conditions, the type of structure being coated, and the desired performance characteristics. As the market continues to evolve, manufacturers are focusing on developing advanced formulations that combine the benefits of both epoxy and inorganic zinc-rich primers, providing enhanced protection and performance. This ongoing innovation is driven by the need to address the challenges posed by increasingly stringent environmental regulations and the demand for more sustainable and efficient coating solutions. By leveraging the unique properties of zinc-rich primers, the Global Zinc Rich Marine Coating Market is poised to continue its growth trajectory, offering valuable protection for marine structures worldwide.

Bulk Carriers, Tankers, Container Ships, Passenger and Cruise Ships, Others in the Global Zinc Rich Marine Coating Market:

The Global Zinc Rich Marine Coating Market finds extensive usage across various types of vessels, including bulk carriers, tankers, container ships, passenger and cruise ships, and others. Bulk carriers, which transport large quantities of unpackaged bulk cargo such as grains, coal, and ore, require robust coatings to protect their hulls from the corrosive effects of seawater and the abrasive nature of the cargo. Zinc-rich marine coatings provide an effective barrier, ensuring the structural integrity and longevity of these vessels. Tankers, which carry liquid cargoes like oil, chemicals, and liquefied natural gas, also benefit significantly from zinc-rich coatings. The coatings protect the tanks and hulls from corrosion, which is crucial given the hazardous nature of the cargo and the potential for environmental contamination. Container ships, which transport goods in large containers, rely on zinc-rich coatings to protect their hulls from the harsh marine environment and the constant loading and unloading of cargo. These coatings help maintain the vessel's performance and efficiency, reducing maintenance costs and downtime. Passenger and cruise ships, which prioritize safety and aesthetics, use zinc-rich coatings to ensure the structural integrity of the vessel while maintaining a visually appealing appearance. The coatings protect against corrosion and wear, contributing to the safety and comfort of passengers. Other vessels, such as fishing boats, ferries, and naval ships, also utilize zinc-rich marine coatings to protect against the harsh conditions of the sea. These coatings are essential for maintaining the operational readiness and longevity of the vessels, ensuring they can perform their intended functions effectively. The versatility and effectiveness of zinc-rich marine coatings make them a preferred choice for a wide range of marine applications, providing reliable protection and extending the service life of valuable marine assets. As the demand for maritime transportation and activities continues to grow, the Global Zinc Rich Marine Coating Market is expected to expand, driven by the need for durable and efficient coating solutions that can withstand the challenges of the marine environment.

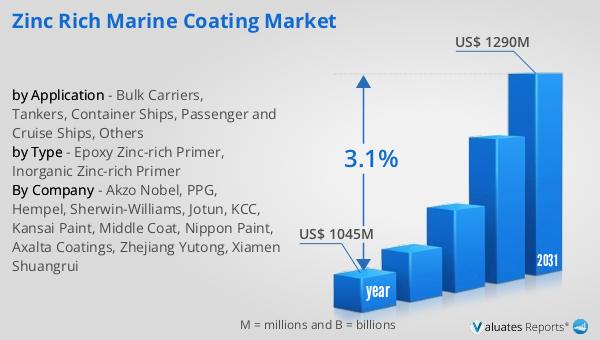

Global Zinc Rich Marine Coating Market Outlook:

In 2024, the global market for Zinc Rich Marine Coating was valued at approximately $1,045 million. Looking ahead, this market is anticipated to grow, reaching an estimated size of $1,290 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.1% over the forecast period. This steady growth can be attributed to several factors, including the increasing demand for durable and long-lasting coatings that can protect marine vessels and structures from the harsh conditions of the sea. As global maritime activities continue to expand, driven by international trade and the need for efficient transportation solutions, the demand for effective marine coatings is expected to rise. The market is also influenced by technological advancements and innovations aimed at improving the performance and sustainability of zinc-rich coatings. Companies operating in this space are investing in research and development to enhance their product offerings and meet the diverse needs of their customers. As a result, the Global Zinc Rich Marine Coating Market is poised for continued growth, offering valuable protection for marine structures worldwide. This market outlook highlights the importance of zinc-rich coatings in ensuring the longevity and performance of marine vessels, making them an essential component of the maritime industry.

| Report Metric | Details |

| Report Name | Zinc Rich Marine Coating Market |

| Accounted market size in year | US$ 1045 million |

| Forecasted market size in 2031 | US$ 1290 million |

| CAGR | 3.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

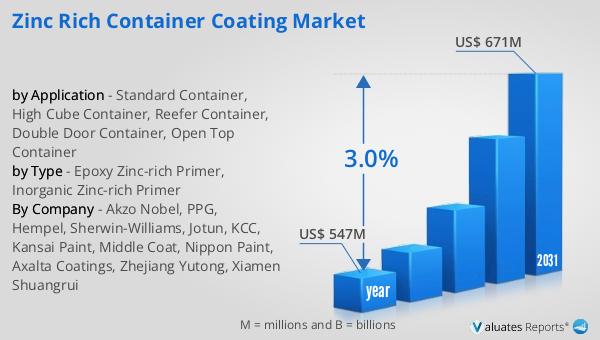

| By Company | Akzo Nobel, PPG, Hempel, Sherwin-Williams, Jotun, KCC, Kansai Paint, Middle Coat, Nippon Paint, Axalta Coatings, Zhejiang Yutong, Xiamen Shuangrui |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |