What is Global Raw Chicken Meat Market?

The global raw chicken meat market is a significant segment of the broader poultry industry, characterized by its vast scale and essential role in meeting the protein needs of populations worldwide. This market encompasses the production, distribution, and sale of raw chicken meat, which is a staple in many diets due to its affordability, versatility, and nutritional value. The demand for raw chicken meat is driven by various factors, including population growth, urbanization, and increasing consumer preference for lean protein sources. Additionally, the market is influenced by trends such as the rise of health-conscious eating habits and the growing popularity of high-protein diets. The global raw chicken meat market is also shaped by advancements in poultry farming techniques, improvements in supply chain logistics, and stringent food safety regulations. These factors collectively contribute to the market's dynamic nature, presenting both opportunities and challenges for producers, distributors, and retailers. As a result, stakeholders in the raw chicken meat market must continuously adapt to changing consumer preferences and regulatory landscapes to remain competitive and meet the evolving demands of the global market.

Bone-in Cut Raw Chicken Meat, Boneless Cut Raw Chicken Meat, Whole Chicken Raw Chicken Meat in the Global Raw Chicken Meat Market:

In the global raw chicken meat market, different cuts of chicken cater to diverse consumer preferences and culinary needs. Bone-in cut raw chicken meat, for instance, includes pieces like drumsticks, thighs, and wings, which are favored for their rich flavor and juiciness. These cuts are often used in traditional recipes and are popular in regions where slow-cooking methods are prevalent. The bone-in cuts are also preferred for grilling and barbecuing, as the bones help retain moisture and enhance the taste during cooking. On the other hand, boneless cut raw chicken meat, such as chicken breasts and fillets, is highly sought after for its convenience and versatility. These cuts are easy to prepare and cook quickly, making them ideal for busy households and food service establishments. Boneless chicken is often used in dishes that require uniform pieces, such as stir-fries, salads, and sandwiches. Its lean nature also appeals to health-conscious consumers who prioritize low-fat protein options. Whole chicken raw chicken meat represents another segment of the market, offering consumers the flexibility to prepare a variety of dishes from a single purchase. Whole chickens are often roasted or baked, providing a cost-effective option for families and gatherings. They also allow for the use of every part of the bird, minimizing waste and maximizing value. In the global market, the choice between bone-in, boneless, and whole chicken cuts is influenced by cultural preferences, cooking traditions, and dietary trends. Producers and retailers must understand these nuances to effectively cater to the diverse needs of their customer base. By offering a range of cuts, they can appeal to a broader audience and capitalize on the growing demand for raw chicken meat across different regions.

Food Services, Retail in the Global Raw Chicken Meat Market:

The global raw chicken meat market plays a crucial role in the food services and retail sectors, serving as a primary ingredient in a wide array of culinary offerings. In the food services industry, raw chicken meat is a staple in restaurants, catering services, and fast-food chains, where it is used to create diverse menu items that cater to various tastes and dietary preferences. Chefs and culinary professionals value chicken for its versatility, as it can be prepared using numerous cooking methods, including grilling, frying, roasting, and poaching. This adaptability allows food service providers to offer a range of dishes, from classic comfort foods to innovative gourmet creations. Additionally, the relatively low cost of chicken compared to other meats makes it an attractive option for businesses looking to manage food costs while maintaining quality. In the retail sector, raw chicken meat is a popular choice among consumers shopping for home-cooked meals. Supermarkets and grocery stores stock a variety of chicken cuts, including bone-in, boneless, and whole chickens, to meet the diverse needs of their customers. The convenience of pre-packaged and portioned chicken products appeals to busy shoppers seeking quick and easy meal solutions. Moreover, the rise of health-conscious eating habits has led to increased demand for organic and free-range chicken options, prompting retailers to expand their offerings to include these premium products. The global raw chicken meat market's influence on food services and retail is further amplified by trends such as the growing popularity of meal kits and online grocery shopping, which provide consumers with convenient access to fresh ingredients, including chicken. As these sectors continue to evolve, the demand for raw chicken meat is expected to remain strong, driven by its essential role in both commercial and home kitchens.

Global Raw Chicken Meat Market Outlook:

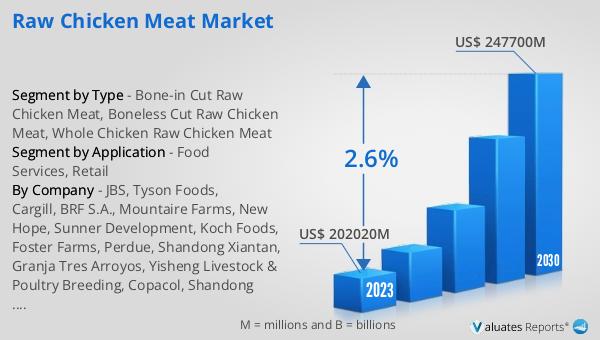

In 2024, the global market for raw chicken meat was valued at approximately $217.75 billion, with projections indicating a growth to around $259.25 billion by 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 2.6% over the forecast period. Such expansion underscores the increasing demand for raw chicken meat across various regions, driven by factors such as population growth, urbanization, and changing dietary preferences. A significant player in this market is JBS, one of the largest manufacturers of raw chicken meat globally, commanding a market share exceeding 70%. This dominance highlights JBS's extensive production capabilities, efficient supply chain management, and ability to meet diverse consumer needs. The company's strong market presence is a testament to its strategic investments in technology, sustainability, and innovation, which have enabled it to maintain a competitive edge in the industry. As the global raw chicken meat market continues to evolve, companies like JBS are likely to play a pivotal role in shaping its future, leveraging their expertise and resources to capitalize on emerging opportunities and address challenges in the sector.

| Report Metric | Details |

| Report Name | Raw Chicken Meat Market |

| Accounted market size in year | US$ 217750 million |

| Forecasted market size in 2031 | US$ 259250 million |

| CAGR | 2.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | JBS, Tyson Foods, Cargill, BRF S.A., Mountaire Farms, New Hope, Sunner Development, Koch Foods, Foster Farms, Perdue, Shandong Xiantan, Granja Tres Arroyos, Yisheng Livestock & Poultry Breeding, Copacol, Shandong Minhe Animal Husbandry, Bello Alimentos, Prosavic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |