What is Global Aircraft Carbon Brake Market?

The Global Aircraft Carbon Brake Market is a specialized segment within the aerospace industry that focuses on the production and distribution of carbon brakes for aircraft. These brakes are crucial components used in both commercial and military aircraft to ensure safe and efficient stopping power. Carbon brakes are preferred over traditional steel brakes due to their lighter weight, higher energy absorption capacity, and better performance under high-temperature conditions. This market is driven by the increasing demand for fuel-efficient and lightweight aircraft, as carbon brakes contribute significantly to reducing the overall weight of an aircraft, thereby enhancing fuel efficiency. Additionally, the rise in air travel and the expansion of airline fleets globally have further fueled the demand for advanced braking systems. The market is characterized by a few dominant players who hold significant market shares, and it is continuously evolving with technological advancements aimed at improving brake performance and longevity. The focus on sustainability and reducing carbon emissions in the aviation sector also plays a crucial role in the market's growth, as carbon brakes align with these environmental goals by offering improved efficiency and reduced wear and tear.

Commercial Brake, Military Brake in the Global Aircraft Carbon Brake Market:

In the realm of the Global Aircraft Carbon Brake Market, commercial and military brakes serve distinct yet overlapping purposes. Commercial brakes are primarily used in passenger and cargo aircraft operated by airlines and freight companies. These brakes are designed to handle the rigorous demands of frequent takeoffs and landings, ensuring passenger safety and operational efficiency. The commercial sector is driven by the rapid expansion of the aviation industry, with airlines continuously upgrading their fleets to more modern and efficient aircraft equipped with advanced braking systems. Carbon brakes in this sector offer significant advantages, such as reduced maintenance costs and longer lifespan compared to traditional steel brakes, making them an attractive option for commercial operators looking to optimize operational costs and enhance performance. On the other hand, military brakes are used in various types of military aircraft, including fighter jets, transport planes, and helicopters. The military sector demands brakes that can withstand extreme conditions, such as high-speed landings and rapid deceleration, often required in combat and tactical operations. Carbon brakes are particularly suited for military applications due to their superior heat dissipation properties and ability to perform under high-stress conditions. The military's focus on enhancing aircraft performance and readiness has led to increased adoption of carbon brakes, as they contribute to improved maneuverability and reduced maintenance downtime. Both commercial and military sectors benefit from the technological advancements in carbon brake systems, which include innovations in materials and design aimed at further enhancing performance and durability. The integration of smart technologies and data analytics in brake systems is also gaining traction, providing operators with real-time insights into brake health and performance, thereby enabling predictive maintenance and reducing the risk of unexpected failures. As the aviation industry continues to evolve, the demand for high-performance braking systems in both commercial and military applications is expected to grow, driven by the need for safer, more efficient, and environmentally friendly solutions. The Global Aircraft Carbon Brake Market is poised to play a pivotal role in meeting these demands, with manufacturers focusing on innovation and collaboration to deliver cutting-edge products that meet the diverse needs of the aviation sector.

Aftermarket, OEM in the Global Aircraft Carbon Brake Market:

The Global Aircraft Carbon Brake Market finds its application in two primary areas: the aftermarket and Original Equipment Manufacturer (OEM) sectors. The aftermarket segment involves the sale of carbon brakes and related components for aircraft that are already in service. This segment is crucial for maintaining the operational efficiency and safety of existing aircraft fleets. As aircraft undergo regular maintenance and overhauls, the demand for replacement brakes and components remains steady. The aftermarket is characterized by a high level of competition, with numerous suppliers offering a range of products and services to meet the diverse needs of airline operators and maintenance providers. The focus in this segment is on providing high-quality, reliable, and cost-effective solutions that ensure the continued performance and safety of aircraft. On the other hand, the OEM segment involves the supply of carbon brakes for new aircraft being manufactured. This segment is driven by the production of new aircraft models and the expansion of airline fleets. OEMs work closely with aircraft manufacturers to develop customized braking solutions that meet the specific requirements of each aircraft model. The emphasis in this segment is on innovation and collaboration, with manufacturers investing in research and development to create advanced braking systems that offer superior performance, reduced weight, and enhanced durability. The OEM market is characterized by long-term contracts and partnerships, with manufacturers striving to establish strong relationships with aircraft producers to secure a steady stream of business. Both the aftermarket and OEM segments are integral to the growth of the Global Aircraft Carbon Brake Market, with each offering unique opportunities and challenges. The aftermarket provides a stable revenue stream, driven by the ongoing need for maintenance and replacement parts, while the OEM segment offers growth potential through the production of new aircraft and the adoption of advanced technologies. As the aviation industry continues to evolve, the demand for high-performance carbon brakes in both segments is expected to increase, driven by the need for safer, more efficient, and environmentally friendly solutions. Manufacturers in the Global Aircraft Carbon Brake Market are well-positioned to capitalize on these opportunities, leveraging their expertise and innovation to deliver cutting-edge products that meet the diverse needs of the aviation sector.

Global Aircraft Carbon Brake Market Outlook:

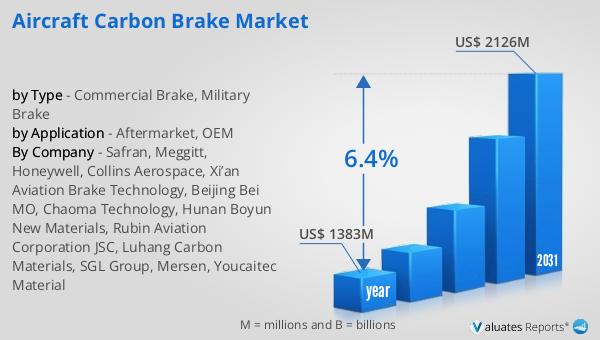

The outlook for the Global Aircraft Carbon Brake Market indicates a promising growth trajectory. In 2024, the market was valued at approximately US$ 1,383 million, and it is anticipated to expand to a revised size of US$ 2,126 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.4% over the forecast period. The market is dominated by a few key players, with the top five companies, including Safran, Meggitt, Honeywell, Collins Aerospace, and Xian Aviation Brake Technology, collectively holding about 90% of the market share. Among these, Safran stands out as the largest manufacturer, accounting for approximately 50% of the market. The production of aircraft carbon brakes is concentrated in North America and the Asia Pacific regions, which together represent more than 30% of the market. In terms of application, the aftermarket segment holds a significant share, accounting for over 90% of the market. This dominance is attributed to the continuous need for maintenance and replacement of brakes in existing aircraft fleets. The market's growth is driven by the increasing demand for lightweight and fuel-efficient aircraft, as well as the expansion of airline fleets globally. As the aviation industry continues to evolve, the Global Aircraft Carbon Brake Market is poised to play a crucial role in meeting the demands for advanced braking systems that enhance safety, performance, and sustainability.

| Report Metric | Details |

| Report Name | Aircraft Carbon Brake Market |

| Accounted market size in year | US$ 1383 million |

| Forecasted market size in 2031 | US$ 2126 million |

| CAGR | 6.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Safran, Meggitt, Honeywell, Collins Aerospace, Xi’an Aviation Brake Technology, Beijing Bei MO, Chaoma Technology, Hunan Boyun New Materials, Rubin Aviation Corporation JSC, Luhang Carbon Materials, SGL Group, Mersen, Youcaitec Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |