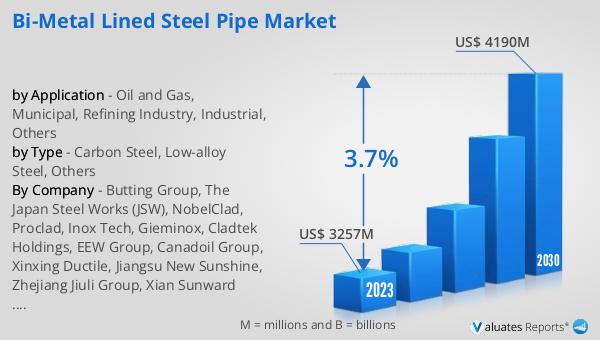

What is Global Bi-Metal Lined Steel Pipe Market?

The Global Bi-Metal Lined Steel Pipe Market is a specialized segment within the broader steel pipe industry, focusing on pipes that combine two different metals to enhance performance and durability. These pipes are designed with an outer layer of steel and an inner lining of a different metal, often chosen for its resistance to corrosion or wear. This combination allows the pipes to withstand harsh environments and extend their lifespan, making them ideal for industries that require robust and reliable piping solutions. The market for these pipes is driven by the need for advanced infrastructure in sectors such as oil and gas, municipal water systems, and industrial applications. As industries continue to seek materials that offer both strength and resistance to environmental factors, the demand for bi-metal lined steel pipes is expected to grow. This market is characterized by technological advancements and innovations aimed at improving the efficiency and effectiveness of these pipes, ensuring they meet the evolving needs of various industries. The global reach of this market highlights its importance in supporting critical infrastructure projects worldwide, making it a key component in the development of modern industrial and municipal systems.

Carbon Steel, Low-alloy Steel, Others in the Global Bi-Metal Lined Steel Pipe Market:

Carbon steel, low-alloy steel, and other materials play a significant role in the Global Bi-Metal Lined Steel Pipe Market, each offering unique properties that cater to different industrial needs. Carbon steel is one of the most commonly used materials in the production of bi-metal lined steel pipes due to its strength, durability, and cost-effectiveness. It is composed primarily of iron and carbon, which gives it excellent tensile strength and the ability to withstand high pressure. This makes carbon steel an ideal choice for applications in the oil and gas industry, where pipes are often subjected to extreme conditions. Additionally, carbon steel's versatility allows it to be used in a variety of other industries, including construction and manufacturing, where its strength and affordability are highly valued.

Oil and Gas, Municipal, Refining Industry, Industrial, Others in the Global Bi-Metal Lined Steel Pipe Market:

Low-alloy steel, on the other hand, is a type of steel that contains small amounts of alloying elements, such as chromium, nickel, and molybdenum, which enhance its mechanical properties. These elements improve the steel's resistance to corrosion and wear, making low-alloy steel a preferred choice for applications that require enhanced durability and longevity. In the context of bi-metal lined steel pipes, low-alloy steel is often used as the outer layer, providing a strong and resilient shell that protects the inner lining from external damage. This combination of materials ensures that the pipes can withstand harsh environmental conditions, such as those found in chemical processing plants and refineries, where exposure to corrosive substances is common.

Global Bi-Metal Lined Steel Pipe Market Outlook:

Other materials used in the production of bi-metal lined steel pipes include stainless steel and various non-ferrous metals, each offering distinct advantages depending on the specific application. Stainless steel, for example, is known for its exceptional resistance to corrosion and staining, making it an ideal choice for applications in the food and beverage industry, where hygiene and cleanliness are paramount. Non-ferrous metals, such as copper and aluminum, are also used in certain applications where their unique properties, such as electrical conductivity and lightweight, are required. The choice of material for the inner lining of a bi-metal lined steel pipe is often determined by the specific requirements of the application, ensuring that the pipe can deliver optimal performance and reliability.

| Report Metric | Details |

| Report Name | Bi-Metal Lined Steel Pipe Market |

| Accounted market size in 2024 | US$ 3370 million |

| Forecasted market size in 2031 | US$ 4330 million |

| CAGR | 3.7% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Butting Group, The Japan Steel Works (JSW), NobelClad, Proclad, Inox Tech, Gieminox, Cladtek Holdings, EEW Group, Canadoil Group, Xinxing Ductile, Jiangsu New Sunshine, Zhejiang Jiuli Group, Xian Sunward Aeromat, Jiangsu Shunlong, Jiangsu Zhongxin |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |