What is Global Magnetic Reed Switch Market?

The Global Magnetic Reed Switch Market is a fascinating segment within the electronics industry, characterized by its unique functionality and wide range of applications. A magnetic reed switch is a small, yet highly effective device that operates by opening or closing an electrical circuit in response to a magnetic field. These switches are composed of two ferrous reeds encased in a glass tube, which come into contact when exposed to a magnetic field, thus completing the circuit. The simplicity and reliability of magnetic reed switches make them a preferred choice in various applications, from consumer electronics to industrial machinery. The global market for these switches is driven by their increasing use in automation and control systems, where precision and reliability are paramount. Additionally, the growing demand for smart home devices and automotive electronics further propels the market. As industries continue to innovate and integrate more automated solutions, the magnetic reed switch market is poised for significant growth, offering opportunities for manufacturers and suppliers to expand their reach and enhance their product offerings. The market's expansion is also supported by advancements in technology, which have led to the development of more efficient and durable reed switches, catering to the evolving needs of various sectors.

Form A, Form B, Form C in the Global Magnetic Reed Switch Market:

In the realm of the Global Magnetic Reed Switch Market, the terms Form A, Form B, and Form C refer to different configurations of reed switches, each serving distinct purposes based on their contact arrangements. Form A, also known as a normally open (NO) configuration, is the most common type of reed switch. In this setup, the contacts are open when there is no magnetic field present, and they close when a magnetic field is applied. This configuration is widely used in applications where the circuit needs to be completed only when a specific condition is met, such as in security systems for door and window sensors. Form A switches are valued for their simplicity and reliability, making them a staple in many electronic devices. Form B, or normally closed (NC) configuration, operates in the opposite manner. In this arrangement, the contacts are closed in the absence of a magnetic field and open when a magnetic field is applied. This type of switch is less common than Form A but is crucial in applications where the circuit needs to be interrupted under certain conditions, such as in safety systems that require immediate disconnection in the presence of a magnetic field. Form B switches are often used in fail-safe mechanisms, where maintaining a closed circuit is essential until a specific event triggers the opening of the circuit. Form C, also known as a changeover or single-pole double-throw (SPDT) configuration, is more complex than Forms A and B. It features three contact points: a common contact, a normally open contact, and a normally closed contact. In the absence of a magnetic field, the common contact is connected to the normally closed contact. When a magnetic field is applied, the common contact switches to connect with the normally open contact. This configuration allows for more versatile applications, as it can be used to switch between two circuits or control multiple functions within a single device. Form C switches are commonly found in applications that require toggling between different states or functions, such as in automotive systems where they might control both the activation and deactivation of a particular feature. The choice between Form A, Form B, and Form C configurations depends largely on the specific requirements of the application, including the desired default state of the circuit and the nature of the control needed. Each form offers unique advantages, and understanding these differences is crucial for selecting the appropriate reed switch for a given application. As the Global Magnetic Reed Switch Market continues to grow, the demand for these various configurations is expected to rise, driven by the increasing complexity and sophistication of modern electronic systems. Manufacturers are continually innovating to enhance the performance and durability of reed switches, ensuring they meet the evolving needs of industries ranging from automotive to consumer electronics.

Automotive, Home Appliance, Office Automation, Industrial Control, Others in the Global Magnetic Reed Switch Market:

The Global Magnetic Reed Switch Market finds extensive usage across various sectors, including automotive, home appliances, office automation, industrial control, and others, each benefiting from the unique properties of reed switches. In the automotive industry, magnetic reed switches are integral to the functioning of numerous systems, such as anti-lock braking systems (ABS), airbags, and seatbelt sensors. Their ability to operate reliably under harsh conditions makes them ideal for automotive applications, where safety and precision are paramount. Reed switches are also used in vehicle security systems, providing reliable detection of unauthorized access. In the realm of home appliances, reed switches are employed in devices like washing machines, refrigerators, and dishwashers. They are used to detect the position of doors and lids, ensuring that appliances operate safely and efficiently. For instance, a reed switch in a washing machine can prevent the machine from starting if the door is not securely closed, thus preventing water spillage and potential damage. Office automation systems also benefit from the use of magnetic reed switches, particularly in printers, copiers, and other office equipment. These switches help in detecting paper jams, monitoring ink levels, and ensuring that devices operate smoothly without interruptions. Their reliability and low power consumption make them an ideal choice for office environments where efficiency and cost-effectiveness are crucial. In industrial control applications, reed switches are used in machinery and equipment to monitor and control various processes. They are often employed in position sensing, level detection, and flow measurement, providing accurate and reliable data that is essential for maintaining optimal operational efficiency. The robustness and durability of reed switches make them suitable for use in harsh industrial environments, where they can withstand extreme temperatures, vibrations, and other challenging conditions. Beyond these specific sectors, magnetic reed switches are also used in a variety of other applications, including medical devices, telecommunications, and consumer electronics. Their versatility and adaptability make them a valuable component in any system that requires reliable and precise control. As technology continues to advance, the demand for magnetic reed switches is expected to grow, driven by the increasing need for automation and smart solutions across various industries. The Global Magnetic Reed Switch Market is poised to expand, offering opportunities for innovation and development in the design and application of these essential components.

Global Magnetic Reed Switch Market Outlook:

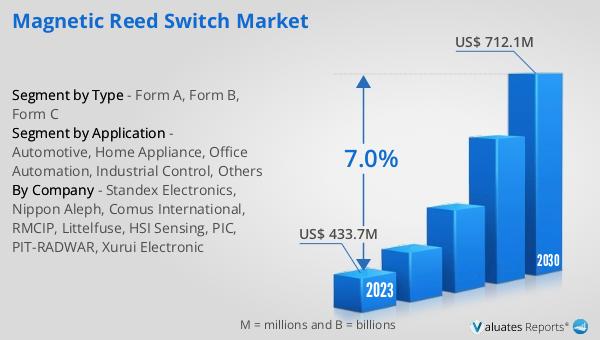

In 2024, the global market for Magnetic Reed Switches was valued at approximately US$ 552 million. Looking ahead, this market is projected to experience significant growth, reaching an estimated value of around US$ 881 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 7.0% during the forecast period from 2025 to 2031. This upward trend is indicative of the increasing demand for magnetic reed switches across various industries, driven by the need for reliable and efficient control solutions. The market's expansion is fueled by advancements in technology and the growing adoption of automation in sectors such as automotive, home appliances, and industrial control. As industries continue to innovate and integrate more sophisticated systems, the demand for magnetic reed switches is expected to rise, offering opportunities for manufacturers and suppliers to capitalize on this growing market. The projected growth of the Global Magnetic Reed Switch Market underscores the importance of these components in modern electronic systems, highlighting their role in enhancing the functionality and efficiency of a wide range of applications. As the market evolves, companies that invest in research and development to improve the performance and durability of reed switches are likely to gain a competitive edge, positioning themselves for success in this dynamic and expanding market.

| Report Metric | Details |

| Report Name | Magnetic Reed Switch Market |

| Forecasted market size in 2031 | approximately US$ 881 million |

| CAGR | 7.0% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Standex Electronics, Nippon Aleph, Comus International, RMCIP, Littelfuse, HSI Sensing, PIC, PIT-RADWAR, Xurui Electronic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |