What is Global Light Weight Wall Panels Market?

The Global Light Weight Wall Panels Market is a dynamic and rapidly evolving sector within the construction industry. These panels are designed to be lighter than traditional wall materials, offering a range of benefits such as ease of installation, reduced transportation costs, and improved energy efficiency. Light weight wall panels are typically made from materials like gypsum, concrete, and composites, which are engineered to provide structural integrity while minimizing weight. This market is driven by the increasing demand for sustainable and energy-efficient building solutions, as well as the growing trend towards modular construction. As urbanization continues to rise globally, the need for quick and efficient building methods has become more pronounced, making light weight wall panels an attractive option for builders and developers. Additionally, these panels are often used in both residential and commercial construction, providing versatility and adaptability to various architectural designs. The market is also influenced by technological advancements that enhance the performance and durability of these panels, further boosting their adoption across different regions. As a result, the Global Light Weight Wall Panels Market is poised for significant growth, driven by the need for innovative and sustainable building solutions.

Hollow Slats, Solid Slats, Composite Slats in the Global Light Weight Wall Panels Market:

In the realm of the Global Light Weight Wall Panels Market, hollow slats, solid slats, and composite slats play crucial roles, each offering unique benefits and applications. Hollow slats are characterized by their lightweight nature, as they are designed with a hollow core that reduces material usage without compromising structural integrity. This makes them an ideal choice for projects where weight reduction is a priority, such as high-rise buildings or structures in seismic zones. The hollow design also provides excellent thermal and acoustic insulation properties, making them suitable for both residential and commercial applications. On the other hand, solid slats are known for their robustness and durability. These slats are made from dense materials, providing superior strength and resistance to impact and wear. Solid slats are often used in areas that require high load-bearing capacity or where additional security is needed, such as in industrial buildings or public infrastructure projects. Despite being heavier than hollow slats, their strength and durability make them a preferred choice for many construction projects. Composite slats, meanwhile, offer a blend of the benefits of both hollow and solid slats. They are typically made from a combination of materials, such as wood fibers and plastic, which are engineered to provide enhanced performance characteristics. Composite slats are known for their versatility, as they can be designed to mimic the appearance of natural materials like wood or stone while offering superior resistance to moisture, insects, and UV radiation. This makes them an excellent choice for outdoor applications, such as facades or cladding, where exposure to the elements is a concern. Furthermore, composite slats are often more environmentally friendly, as they can be made from recycled materials and are designed to be long-lasting, reducing the need for frequent replacements. In summary, the choice between hollow, solid, and composite slats in the Global Light Weight Wall Panels Market depends on the specific requirements of a project, including factors such as weight, strength, durability, and environmental considerations. Each type of slat offers distinct advantages, making them suitable for a wide range of applications in the construction industry.

Building Construction, Transportation Industry in the Global Light Weight Wall Panels Market:

The Global Light Weight Wall Panels Market finds extensive usage in various sectors, particularly in building construction and the transportation industry. In building construction, these panels are favored for their ability to streamline the construction process, reduce labor costs, and enhance energy efficiency. Light weight wall panels are often used in both residential and commercial buildings, providing a quick and efficient solution for creating walls, partitions, and facades. Their lightweight nature makes them easy to transport and install, reducing the overall construction time and costs. Additionally, these panels offer excellent thermal and acoustic insulation properties, contributing to the energy efficiency and comfort of buildings. In the transportation industry, light weight wall panels are used in the construction of vehicles, such as buses, trains, and airplanes, where weight reduction is crucial for improving fuel efficiency and performance. These panels help to reduce the overall weight of the vehicle, leading to lower fuel consumption and emissions. Moreover, the use of light weight wall panels in transportation can enhance the safety and durability of vehicles, as they are designed to withstand impact and wear. The versatility and adaptability of light weight wall panels make them an attractive option for various applications in the construction and transportation industries, driving their demand in the global market.

Global Light Weight Wall Panels Market Outlook:

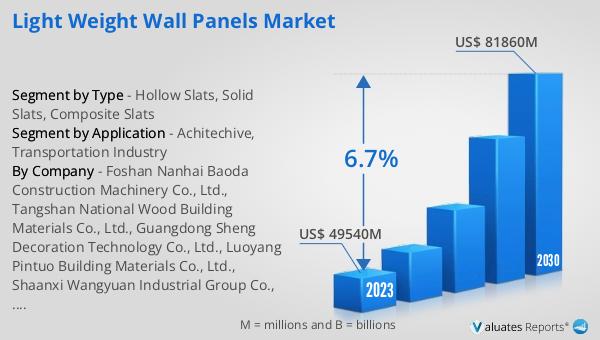

The global market for Light Weight Wall Panels was valued at $58,820 million in 2024 and is anticipated to expand to a revised size of $92,030 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.7% over the forecast period. This growth trajectory underscores the increasing demand for innovative and sustainable building solutions across the globe. The market's expansion is driven by several factors, including the rising trend of urbanization, the need for energy-efficient construction materials, and the growing popularity of modular construction methods. As more regions around the world experience rapid urban development, the demand for quick and efficient building solutions has become more pronounced. Light weight wall panels offer a viable solution to meet these demands, providing a balance between structural integrity and ease of installation. Additionally, advancements in technology have led to the development of more durable and high-performance panels, further boosting their adoption in various sectors. The projected growth of the Global Light Weight Wall Panels Market highlights the importance of these panels in shaping the future of construction and infrastructure development.

| Report Metric | Details |

| Report Name | Light Weight Wall Panels Market |

| Accounted market size in year | US$ 58820 million |

| Forecasted market size in 2031 | US$ 92030 million |

| CAGR | 6.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Foshan Nanhai Baoda Construction Machinery Co., Ltd., Tangshan National Wood Building Materials Co., Ltd., Guangdong Sheng Decoration Technology Co., Ltd., Luoyang Pintuo Building Materials Co., Ltd., Shaanxi Wangyuan Industrial Group Co., Ltd., Lanzhou Tongda Building Materials Co., Ltd., INDIA PRECAST, TSSC, Light Weight Building Factory (LWBF), Fusion, Laminex, Nudo Products, Architonic, GreenEdge IBS, Ober Surfaces |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |