What is Global Car Door Panel Sound Insulation Cotton Market?

The Global Car Door Panel Sound Insulation Cotton Market is a specialized segment within the automotive industry that focuses on enhancing the acoustic comfort inside vehicles. This market revolves around the production and distribution of sound insulation materials specifically designed for car door panels. These materials, often made from various types of cotton and foam, are engineered to reduce noise, vibration, and harshness (NVH) levels within the vehicle cabin. By absorbing and dampening external sounds, these insulation materials contribute to a quieter and more comfortable driving experience. The demand for such products is driven by the increasing consumer preference for quieter vehicles and the growing awareness of the importance of acoustic comfort in enhancing overall vehicle quality. As automotive manufacturers strive to improve the in-cabin experience, the market for car door panel sound insulation cotton is expected to witness steady growth. This market is characterized by continuous innovation, with manufacturers exploring new materials and technologies to improve sound insulation performance while maintaining cost-effectiveness and sustainability. The global reach of this market is evident as it caters to various regions, each with its unique automotive industry dynamics and consumer preferences.

White Cotton, High Density Cotton, Memory Foam in the Global Car Door Panel Sound Insulation Cotton Market:

In the realm of the Global Car Door Panel Sound Insulation Cotton Market, three primary materials stand out: White Cotton, High Density Cotton, and Memory Foam. Each of these materials offers distinct properties that cater to different aspects of sound insulation and vehicle comfort. White Cotton is a traditional material known for its natural sound-absorbing qualities. It is lightweight, eco-friendly, and provides a basic level of sound insulation. Its natural fibers are effective in dampening mid to high-frequency noises, making it a popular choice for entry-level and mid-range vehicles. However, its performance may be limited in more demanding acoustic environments, where higher levels of noise reduction are required. High Density Cotton, on the other hand, is engineered to offer superior sound insulation capabilities. By increasing the density of the cotton fibers, manufacturers can enhance the material's ability to absorb and block sound waves. This makes High Density Cotton an ideal choice for premium vehicles where a higher degree of acoustic comfort is desired. Its robust performance in reducing low-frequency noises, such as engine and road noise, makes it a preferred option for luxury car manufacturers aiming to provide a serene cabin environment. Memory Foam, a more advanced material, is gaining popularity in the sound insulation market due to its unique properties. Originally developed for the aerospace industry, Memory Foam is known for its ability to conform to shapes and provide excellent sound absorption. Its viscoelastic nature allows it to effectively dampen vibrations and reduce noise transmission through car door panels. This makes it particularly suitable for high-performance vehicles where both sound insulation and weight reduction are critical considerations. Memory Foam's adaptability also allows it to be used in various configurations, providing manufacturers with flexibility in design and application. As the Global Car Door Panel Sound Insulation Cotton Market continues to evolve, these materials are likely to see further advancements. Manufacturers are investing in research and development to enhance the performance of these materials, focusing on improving their sound absorption capabilities, durability, and environmental sustainability. Innovations such as hybrid materials, which combine the properties of different insulation materials, are also being explored to achieve optimal sound insulation performance. Additionally, the growing emphasis on sustainability is driving the development of eco-friendly insulation materials, with manufacturers seeking to reduce the environmental impact of their products. This includes the use of recycled materials and the development of biodegradable insulation options. As consumer expectations for quieter and more comfortable vehicles continue to rise, the demand for advanced sound insulation materials like White Cotton, High Density Cotton, and Memory Foam is expected to grow. These materials play a crucial role in enhancing the overall driving experience, contributing to the market's expansion and the continuous pursuit of innovation in the automotive industry.

Passenger Car, Commercial Vehicle in the Global Car Door Panel Sound Insulation Cotton Market:

The usage of Global Car Door Panel Sound Insulation Cotton Market materials extends across various vehicle types, including Passenger Cars and Commercial Vehicles, each with its unique requirements and challenges. In Passenger Cars, the focus is primarily on enhancing the in-cabin experience for drivers and passengers. Sound insulation materials are used to create a quieter and more comfortable environment by reducing the intrusion of external noises such as traffic, wind, and road noise. This is particularly important in urban settings where noise pollution is prevalent. By improving acoustic comfort, manufacturers can enhance the perceived quality of their vehicles, making them more appealing to consumers. In this context, materials like High Density Cotton and Memory Foam are often preferred due to their superior sound absorption capabilities. These materials help create a serene cabin environment, allowing occupants to enjoy music, conversations, and other in-car entertainment without the distraction of external noise. In Commercial Vehicles, the application of sound insulation materials serves a slightly different purpose. While comfort is still a consideration, the primary focus is often on improving driver concentration and reducing fatigue during long hours on the road. Commercial vehicles, such as trucks and buses, are typically exposed to higher levels of noise due to their larger engines and the nature of their operation. Sound insulation materials help mitigate these noise levels, contributing to a safer and more comfortable driving experience. In this segment, durability and cost-effectiveness are key considerations, as commercial vehicles are subject to more demanding operating conditions. High Density Cotton is often used in commercial vehicles due to its robust performance and ability to withstand harsh environments. Additionally, the use of sound insulation materials in commercial vehicles can have economic benefits. By reducing noise levels, drivers can communicate more effectively, leading to improved operational efficiency and safety. Furthermore, a quieter cabin environment can contribute to better driver retention, as it enhances job satisfaction and reduces stress. As the Global Car Door Panel Sound Insulation Cotton Market continues to grow, the application of these materials in both Passenger Cars and Commercial Vehicles is expected to expand. Manufacturers are likely to explore new materials and technologies to meet the evolving demands of consumers and the automotive industry. This includes the development of lightweight and eco-friendly insulation options that align with the industry's sustainability goals. As a result, the market is poised for continued innovation and growth, driven by the increasing emphasis on acoustic comfort and the overall driving experience.

Global Car Door Panel Sound Insulation Cotton Market Outlook:

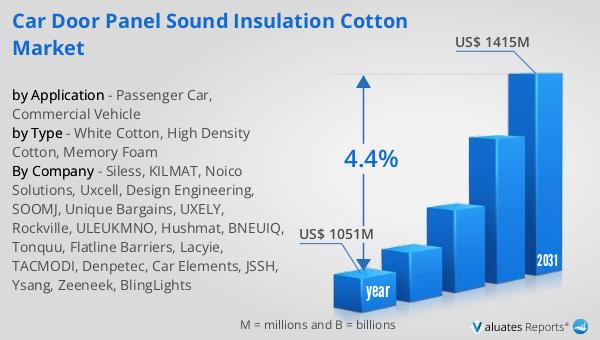

In 2024, the Global Car Door Panel Sound Insulation Cotton Market was valued at approximately $1,051 million. Looking ahead, it is anticipated to grow to a revised size of $1,415 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.4% over the forecast period. This growth trajectory underscores the increasing demand for sound insulation materials in the automotive industry, driven by consumer preferences for quieter and more comfortable vehicles. Among the key players in this market, China stands out as the world's largest automobile producer, accounting for about 32% of global production. This significant share highlights China's pivotal role in shaping the dynamics of the automotive industry and, by extension, the market for car door panel sound insulation cotton. The country's robust automotive manufacturing sector, coupled with its focus on enhancing vehicle quality and consumer satisfaction, positions it as a major contributor to the market's growth. As the industry continues to evolve, the Global Car Door Panel Sound Insulation Cotton Market is expected to witness further advancements in materials and technologies, driven by the pursuit of improved acoustic comfort and sustainability. This outlook reflects the ongoing commitment of manufacturers to meet the changing needs of consumers and the automotive industry, ensuring a quieter and more enjoyable driving experience for all.

| Report Metric | Details |

| Report Name | Car Door Panel Sound Insulation Cotton Market |

| Accounted market size in year | US$ 1051 million |

| Forecasted market size in 2031 | US$ 1415 million |

| CAGR | 4.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Siless, KILMAT, Noico Solutions, Uxcell, Design Engineering, SOOMJ, Unique Bargains, UXELY, Rockville, ULEUKMNO, Hushmat, BNEUIQ, Tonquu, Flatline Barriers, Lacyie, TACMODI, Denpetec, Car Elements, JSSH, Ysang, Zeeneek, BlingLights |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |