What is Global Decoration Moisture-proof Board Market?

The Global Decoration Moisture-proof Board Market is a specialized segment within the construction and interior design industries, focusing on boards that resist moisture and are used for decorative purposes. These boards are essential in environments where humidity and moisture are prevalent, such as bathrooms, kitchens, and basements. They are designed to prevent the growth of mold and mildew, which can cause structural damage and health issues. The market for these boards is driven by the increasing demand for durable and aesthetically pleasing building materials. As consumers and businesses become more aware of the benefits of moisture-proof boards, the demand continues to grow. These boards are available in various materials, including gypsum, cement, and fiber, each offering different levels of moisture resistance and decorative appeal. The market is also influenced by advancements in technology, which have led to the development of more efficient and cost-effective moisture-proof solutions. As a result, the Global Decoration Moisture-proof Board Market is expected to see continued growth, driven by both residential and commercial construction projects.

Ordinary Moisture-Resistant Plasterboards, Locating Point Moisture-Resistant Plasterboards in the Global Decoration Moisture-proof Board Market:

Ordinary Moisture-Resistant Plasterboards and Locating Point Moisture-Resistant Plasterboards are two key products within the Global Decoration Moisture-proof Board Market. Ordinary Moisture-Resistant Plasterboards are designed to withstand environments with moderate humidity levels. They are typically used in areas like kitchens and bathrooms, where moisture exposure is frequent but not excessive. These boards are made by adding water-repellent additives to the core of the plasterboard, which helps to prevent moisture absorption. This makes them an ideal choice for residential and commercial applications where moisture resistance is necessary but not extreme. On the other hand, Locating Point Moisture-Resistant Plasterboards are engineered for areas with high moisture exposure. These boards are often used in basements, laundry rooms, and other spaces where moisture levels are consistently high. They are constructed with a more robust core and additional water-repellent treatments, providing superior moisture resistance compared to ordinary plasterboards. The choice between these two types of plasterboards depends on the specific requirements of the project and the level of moisture exposure expected. In the Global Decoration Moisture-proof Board Market, both types of plasterboards play a crucial role in ensuring the longevity and durability of structures. As the demand for moisture-resistant building materials continues to rise, manufacturers are focusing on developing innovative solutions that offer enhanced performance and aesthetic appeal. This includes the introduction of new materials and technologies that improve the moisture resistance and decorative qualities of plasterboards. Additionally, the market is seeing a trend towards eco-friendly and sustainable products, as consumers and businesses become more environmentally conscious. This has led to the development of plasterboards made from recycled materials and those that have a lower environmental impact. Overall, the Global Decoration Moisture-proof Board Market is characterized by a diverse range of products that cater to different needs and preferences. Whether it's for residential or commercial use, moisture-resistant plasterboards provide a reliable solution for protecting structures from the damaging effects of moisture.

Household, Commercial in the Global Decoration Moisture-proof Board Market:

The usage of Global Decoration Moisture-proof Board Market products extends across various areas, including household and commercial applications. In households, moisture-proof boards are commonly used in areas prone to moisture exposure, such as bathrooms, kitchens, and basements. These boards help to prevent the growth of mold and mildew, which can cause health issues and structural damage. By using moisture-proof boards, homeowners can ensure that their living spaces remain safe and healthy. Additionally, these boards are available in a variety of decorative finishes, allowing homeowners to enhance the aesthetic appeal of their interiors while also providing practical benefits. In commercial settings, moisture-proof boards are used in a wide range of applications, from office buildings to retail spaces. These boards are essential in environments where moisture exposure is a concern, such as restrooms, kitchens, and storage areas. By using moisture-proof boards, businesses can protect their properties from moisture-related damage and maintain a clean and professional appearance. Furthermore, the durability and low maintenance requirements of these boards make them a cost-effective choice for commercial applications. The Global Decoration Moisture-proof Board Market also caters to specialized industries, such as hospitality and healthcare, where hygiene and moisture resistance are critical. In hotels and restaurants, moisture-proof boards are used in kitchens and bathrooms to ensure a safe and sanitary environment for guests and staff. In healthcare facilities, these boards are used in areas like operating rooms and laboratories, where moisture control is essential for maintaining a sterile environment. Overall, the Global Decoration Moisture-proof Board Market offers a wide range of products that cater to the diverse needs of both household and commercial users. Whether it's for enhancing the aesthetic appeal of a home or ensuring the durability and safety of a commercial property, moisture-proof boards provide a reliable solution for managing moisture-related challenges.

Global Decoration Moisture-proof Board Market Outlook:

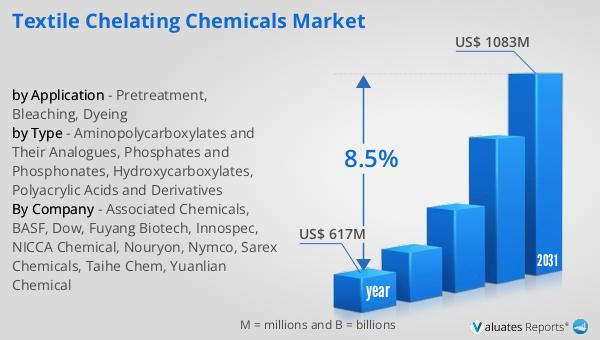

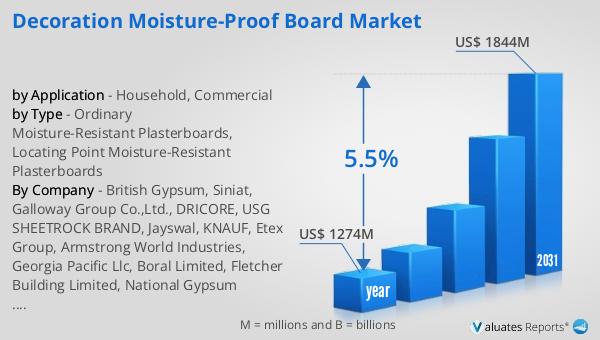

The global market for Decoration Moisture-proof Boards was valued at $1,274 million in 2024 and is anticipated to grow to a revised size of $1,844 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.5% during the forecast period. This growth is indicative of the increasing demand for moisture-resistant building materials across various sectors. As awareness of the benefits of moisture-proof boards continues to rise, more consumers and businesses are opting for these products to enhance the durability and aesthetic appeal of their properties. The market's expansion is also driven by technological advancements that have led to the development of more efficient and cost-effective moisture-proof solutions. These innovations have made it possible for manufacturers to offer a wider range of products that cater to different needs and preferences. Additionally, the trend towards eco-friendly and sustainable building materials is contributing to the market's growth, as more consumers and businesses seek products that have a lower environmental impact. Overall, the Global Decoration Moisture-proof Board Market is poised for continued growth, driven by the increasing demand for durable and aesthetically pleasing building materials.

| Report Metric | Details |

| Report Name | Decoration Moisture-proof Board Market |

| Accounted market size in year | US$ 1274 million |

| Forecasted market size in 2031 | US$ 1844 million |

| CAGR | 5.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | British Gypsum, Siniat, Galloway Group Co.,Ltd., DRICORE, USG SHEETROCK BRAND, Jayswal, KNAUF, Etex Group, Armstrong World Industries, Georgia Pacific Llc, Boral Limited, Fletcher Building Limited, National Gypsum Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |