What is Global Military Submarine Photonics Mast and Antenna Market?

The Global Military Submarine Photonics Mast and Antenna Market is a specialized segment within the defense industry that focuses on the development and deployment of advanced photonics masts and antennas for submarines. These components are crucial for modern submarines as they replace traditional periscopes with more sophisticated systems that use electronic imaging and communication technologies. The market is driven by the need for enhanced surveillance, communication, and navigation capabilities in military submarines. Photonics masts, unlike traditional periscopes, do not require a physical connection to the submarine's hull, allowing for greater flexibility and reduced risk of detection. Antennas, on the other hand, are essential for maintaining communication with other military assets and command centers. The market is characterized by continuous technological advancements, with key players investing in research and development to improve the performance and reliability of these systems. As global tensions and the need for advanced military capabilities increase, the demand for photonics masts and antennas is expected to grow, making this market a critical component of modern naval defense strategies.

Photonics Mast, Antenna in the Global Military Submarine Photonics Mast and Antenna Market:

Photonics masts are a revolutionary advancement in submarine technology, replacing the traditional periscope with a more versatile and efficient system. Unlike periscopes, which require a direct line of sight and a physical connection to the submarine, photonics masts use electronic imaging to capture and transmit visual data. This allows submarines to remain submerged at greater depths while still gathering crucial information about their surroundings. The mast is equipped with high-resolution cameras and sensors that provide a 360-degree view, enhancing situational awareness and reducing the risk of detection by enemy forces. Additionally, photonics masts can be retracted into the submarine's hull, minimizing the vessel's acoustic and visual signature. Antennas play a vital role in the Global Military Submarine Photonics Mast and Antenna Market by ensuring seamless communication between the submarine and other military assets. These antennas are designed to operate in various frequency bands, enabling secure and reliable transmission of data, voice, and video. They are also equipped with advanced encryption technologies to protect sensitive information from interception. The integration of photonics masts and antennas into submarines enhances their operational capabilities, allowing them to perform a wide range of missions, from intelligence gathering to combat operations. The market for these technologies is driven by the increasing demand for stealthy and efficient naval platforms that can operate in diverse environments. As countries invest in modernizing their naval fleets, the adoption of photonics masts and antennas is expected to rise, offering significant opportunities for manufacturers and suppliers in this sector. The continuous evolution of these technologies is likely to lead to further improvements in submarine performance, making them an indispensable part of modern naval warfare.

Military Reconnaissance, Military Strike in the Global Military Submarine Photonics Mast and Antenna Market:

The usage of Global Military Submarine Photonics Mast and Antenna Market technologies in military reconnaissance and strike operations is pivotal for modern naval strategies. In military reconnaissance, photonics masts provide submarines with the ability to gather intelligence without surfacing, thus maintaining stealth. The high-resolution cameras and sensors on the mast capture detailed images and data, which are crucial for assessing enemy positions, movements, and capabilities. This information is transmitted via secure antennas to command centers, where it is analyzed to inform strategic decisions. The ability to conduct reconnaissance while submerged gives submarines a significant tactical advantage, allowing them to operate undetected in hostile waters. In military strike operations, the integration of photonics masts and antennas enhances the submarine's ability to engage targets with precision. The real-time data gathered by the mast's sensors is used to identify and track enemy vessels or installations. This information is relayed to the submarine's weapons systems, enabling accurate targeting and engagement. The antennas ensure continuous communication with other military units, facilitating coordinated strikes and minimizing the risk of friendly fire. The stealth capabilities provided by photonics masts allow submarines to approach targets undetected, increasing the likelihood of a successful strike. The combination of reconnaissance and strike capabilities makes submarines equipped with photonics masts and antennas a formidable asset in naval warfare. As global military forces seek to enhance their operational effectiveness, the demand for these advanced technologies is expected to grow, driving further innovation and development in the Global Military Submarine Photonics Mast and Antenna Market.

Global Military Submarine Photonics Mast and Antenna Market Outlook:

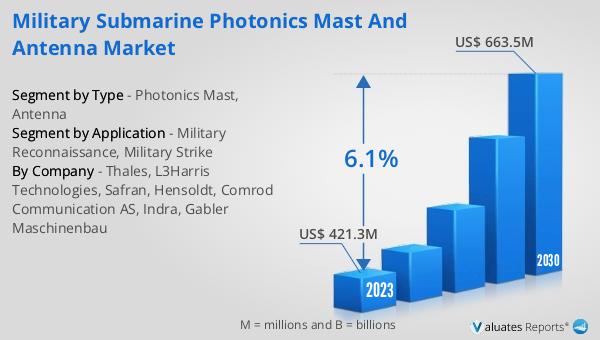

In 2024, the global market for Military Submarine Photonics Mast and Antenna was valued at approximately $490 million. By 2031, it is anticipated to expand to a revised size of $739 million, reflecting a compound annual growth rate (CAGR) of 6.1% over the forecast period. In 2023, the top five players in the market accounted for about 58% of the total revenue, indicating a significant concentration of market power among leading companies. This growth trajectory underscores the increasing importance of advanced photonics masts and antennas in modern naval operations. The market's expansion is driven by the need for enhanced surveillance, communication, and navigation capabilities in military submarines. As global tensions rise and the demand for sophisticated military technologies increases, the market for these components is expected to continue its upward trend. The concentration of market share among the top players highlights the competitive nature of the industry, with companies investing heavily in research and development to maintain their positions. This competitive landscape is likely to spur further innovation, leading to the development of more advanced and efficient photonics masts and antennas. As countries around the world seek to modernize their naval fleets, the Global Military Submarine Photonics Mast and Antenna Market is poised for significant growth, offering substantial opportunities for manufacturers and suppliers in this sector.

| Report Metric | Details |

| Report Name | Military Submarine Photonics Mast and Antenna Market |

| Accounted market size in year | US$ 490 million |

| Forecasted market size in 2031 | US$ 739 million |

| CAGR | 6.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Thales, L3Harris Technologies, Safran, Hensoldt, Comrod Communication AS, Indra, Gabler Maschinenbau |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |