What is Global Electronic Grade Polyimide Varnish Market?

The Global Electronic Grade Polyimide Varnish Market is a specialized segment within the broader chemical and materials industry, focusing on the production and distribution of high-performance varnishes used primarily in electronic applications. These varnishes are derived from polyimide, a polymer known for its exceptional thermal stability, chemical resistance, and electrical insulating properties. Electronic grade polyimide varnishes are crucial in manufacturing advanced electronic components, as they provide a protective coating that enhances the durability and performance of these components under extreme conditions. The market for these varnishes is driven by the increasing demand for miniaturized and high-performance electronic devices across various industries, including consumer electronics, automotive, aerospace, and telecommunications. As technology continues to evolve, the need for reliable and efficient materials like electronic grade polyimide varnish is expected to grow, making it a vital component in the development of next-generation electronic devices. The market is characterized by continuous innovation and development, with manufacturers focusing on enhancing the properties of these varnishes to meet the ever-changing demands of the electronics industry.

Thermoplastic Varnish, Thermosetting Varnish in the Global Electronic Grade Polyimide Varnish Market:

Thermoplastic and thermosetting varnishes are two primary types of electronic grade polyimide varnishes, each with distinct characteristics and applications within the Global Electronic Grade Polyimide Varnish Market. Thermoplastic varnishes are known for their ability to soften when heated and harden upon cooling, allowing for easy reshaping and reprocessing. This property makes them ideal for applications where flexibility and adaptability are crucial, such as in flexible electronics and certain types of coatings that require frequent adjustments or repairs. Thermoplastic varnishes are often used in applications where the varnish needs to be applied in layers or where the final product may need to be reshaped or reworked. On the other hand, thermosetting varnishes undergo a chemical change when heated, resulting in a rigid and inflexible structure that cannot be reshaped once set. This makes them suitable for applications requiring high thermal stability and mechanical strength, such as in the insulation of high-performance electronic components and the protection of sensitive circuits. Thermosetting varnishes are often used in environments where the varnish must withstand high temperatures and harsh conditions without degrading. Both types of varnishes play a critical role in the electronics industry, providing essential protective coatings that enhance the performance and longevity of electronic components. The choice between thermoplastic and thermosetting varnishes depends on the specific requirements of the application, including factors such as temperature resistance, mechanical strength, and flexibility. Manufacturers in the Global Electronic Grade Polyimide Varnish Market continue to innovate and develop new formulations to meet the diverse needs of the electronics industry, ensuring that these varnishes remain a vital component in the production of advanced electronic devices.

Semiconductors, Display Panels, Electric Vehicles, Aerospace, Others in the Global Electronic Grade Polyimide Varnish Market:

The Global Electronic Grade Polyimide Varnish Market finds extensive usage across various sectors, including semiconductors, display panels, electric vehicles, aerospace, and others, each benefiting from the unique properties of these varnishes. In the semiconductor industry, electronic grade polyimide varnishes are used as insulating layers and protective coatings for chips and other components. Their excellent thermal stability and electrical insulation properties make them ideal for protecting sensitive semiconductor devices from heat and environmental damage, ensuring reliable performance and longevity. In display panels, these varnishes are used to enhance the durability and performance of screens, providing a protective layer that resists scratches, moisture, and other environmental factors. This is particularly important in the production of high-resolution displays for smartphones, tablets, and televisions, where clarity and durability are paramount. In the electric vehicle industry, electronic grade polyimide varnishes are used to insulate and protect various components, including batteries and electronic control units. Their ability to withstand high temperatures and harsh conditions makes them ideal for use in electric vehicles, where reliability and safety are critical. In the aerospace sector, these varnishes are used to protect electronic components from extreme temperatures and environmental conditions, ensuring the reliability and safety of aerospace systems. The unique properties of electronic grade polyimide varnishes make them an essential material in the production of advanced aerospace technologies, where performance and durability are critical. Beyond these industries, electronic grade polyimide varnishes are also used in various other applications, including telecommunications, medical devices, and industrial equipment, where their protective and insulating properties are highly valued. As technology continues to advance, the demand for high-performance materials like electronic grade polyimide varnish is expected to grow, driving innovation and development in this dynamic market.

Global Electronic Grade Polyimide Varnish Market Outlook:

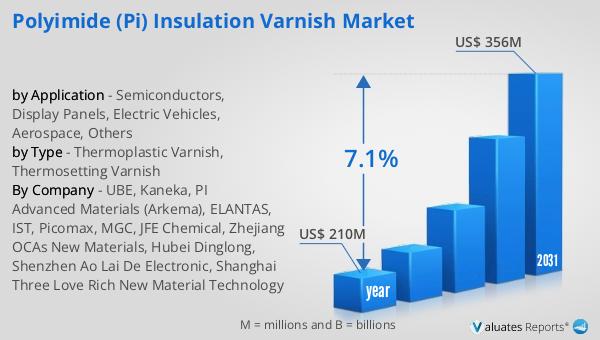

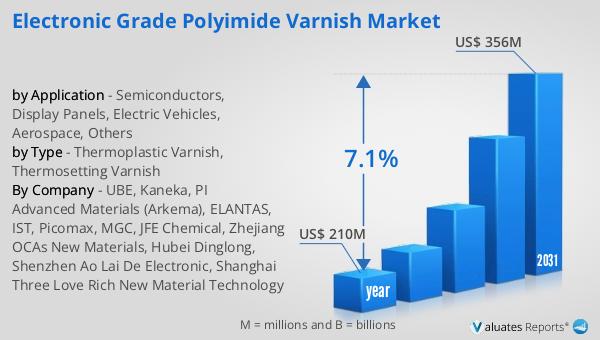

The global market for Electronic Grade Polyimide Varnish was valued at $210 million in 2024 and is anticipated to expand to a revised size of $356 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.1% over the forecast period. This growth trajectory underscores the increasing demand for high-performance varnishes in various industries, driven by the rapid advancement of technology and the need for reliable and efficient materials. The market's expansion is fueled by the growing adoption of electronic devices across multiple sectors, including consumer electronics, automotive, aerospace, and telecommunications. As these industries continue to evolve, the demand for materials that can withstand extreme conditions and enhance the performance of electronic components is expected to rise. The projected growth of the Electronic Grade Polyimide Varnish Market highlights the importance of these varnishes in the development of next-generation electronic devices and systems. Manufacturers are focusing on innovation and development to meet the diverse needs of the electronics industry, ensuring that electronic grade polyimide varnishes remain a vital component in the production of advanced technologies. The market's growth is a testament to the critical role these varnishes play in enhancing the performance and longevity of electronic components, making them an essential material in the modern electronics landscape.

| Report Metric |

Details |

| Report Name |

Electronic Grade Polyimide Varnish Market |

| Accounted market size in year |

US$ 210 million |

| Forecasted market size in 2031 |

US$ 356 million |

| CAGR |

7.1% |

| Base Year |

year |

| Forecasted years |

2025 - 2031 |

| by Type |

- Thermoplastic Varnish

- Thermosetting Varnish

|

| by Application |

- Semiconductors

- Display Panels

- Electric Vehicles

- Aerospace

- Others

|

| Production by Region |

- North America

- Europe

- China

- Japan

|

| Consumption by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia)

- Asia-Pacific (China, Japan, South Korea, Taiwan)

- Southeast Asia (India)

- Latin America (Mexico, Brazil)

|

| By Company |

UBE, Kaneka, PI Advanced Materials (Arkema), ELANTAS, IST, Picomax, MGC, JFE Chemical, Zhejiang OCAs New Materials, Hubei Dinglong, Shenzhen Ao Lai De Electronic, Shanghai Three Love Rich New Material Technology |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |