What is Global Commercial Aircraft Battery Market?

The Global Commercial Aircraft Battery Market is a crucial segment within the aviation industry, focusing on the development and supply of batteries used in commercial aircraft. These batteries are essential for various functions, including starting engines, powering auxiliary power units (APUs), and serving as backup power sources for critical systems. As the aviation industry continues to evolve with advancements in technology and a growing emphasis on sustainability, the demand for efficient and reliable aircraft batteries is on the rise. The market encompasses a range of battery types, including lithium-based, nickel-based, and lead-acid batteries, each offering distinct advantages and applications. With the increasing adoption of electric and hybrid-electric aircraft, the market is poised for significant growth, driven by the need for lightweight, high-performance batteries that can support longer flight durations and reduce carbon emissions. As airlines and manufacturers strive to enhance operational efficiency and meet stringent environmental regulations, the Global Commercial Aircraft Battery Market is expected to play a pivotal role in shaping the future of aviation. The market's growth is further supported by ongoing research and development efforts aimed at improving battery technology and performance, ensuring that the aviation industry can meet the demands of a rapidly changing world.

Lithium-Based Battery, Nickel-Based Battery, Lead Acid Battery in the Global Commercial Aircraft Battery Market:

Lithium-based batteries are at the forefront of the Global Commercial Aircraft Battery Market due to their high energy density, lightweight nature, and long cycle life. These characteristics make them ideal for modern aircraft, where weight reduction and efficiency are paramount. Lithium-ion batteries, a subset of lithium-based batteries, are particularly popular because they offer a high power-to-weight ratio, which is crucial for aircraft applications. They are used in various systems, including main batteries and auxiliary power units (APUs), providing reliable power for starting engines and supporting electrical systems during flight. However, safety concerns related to thermal runaway and the need for robust battery management systems are challenges that manufacturers must address. Nickel-based batteries, such as nickel-cadmium (NiCd) and nickel-metal hydride (NiMH) batteries, have been used in aviation for decades. They are known for their durability, reliability, and ability to perform well in extreme temperatures. NiCd batteries, in particular, have a long history of use in commercial aircraft, offering a proven track record of safety and performance. Despite their advantages, nickel-based batteries are heavier than lithium-based alternatives, which can impact fuel efficiency and overall aircraft performance. Lead-acid batteries, one of the oldest battery technologies, are still used in some aircraft applications due to their low cost and reliability. They are typically used in smaller aircraft or as backup power sources in larger commercial planes. While lead-acid batteries are robust and easy to maintain, their heavy weight and lower energy density compared to lithium and nickel-based batteries limit their use in modern aviation. As the industry moves towards more sustainable and efficient solutions, the focus is increasingly shifting towards advanced battery technologies that can meet the demands of next-generation aircraft. Overall, each battery type offers unique benefits and challenges, and the choice of battery depends on specific aircraft requirements, operational conditions, and cost considerations. As technology continues to advance, the Global Commercial Aircraft Battery Market is likely to see further innovations that enhance battery performance, safety, and sustainability.

Main Battery, APU Battery in the Global Commercial Aircraft Battery Market:

In the Global Commercial Aircraft Battery Market, batteries serve critical roles in various areas, including as main batteries and auxiliary power unit (APU) batteries. Main batteries are essential for starting the aircraft's engines and providing power to essential systems during flight. They act as a primary power source when the aircraft is on the ground and the engines are not running, ensuring that systems such as lighting, avionics, and communication equipment remain operational. The reliability and performance of main batteries are crucial, as any failure can lead to significant operational disruptions and safety concerns. Lithium-based batteries are increasingly favored for main battery applications due to their high energy density and lightweight properties, which contribute to overall fuel efficiency and aircraft performance. APU batteries, on the other hand, are used to power the auxiliary power unit, a critical component that provides energy for systems such as air conditioning, lighting, and avionics when the main engines are not running. The APU is particularly important during ground operations, allowing the aircraft to maintain essential functions without relying on external power sources. Nickel-based batteries, such as nickel-cadmium, have traditionally been used for APU applications due to their robustness and ability to perform well in various environmental conditions. However, as the industry shifts towards more sustainable and efficient solutions, there is a growing interest in exploring advanced battery technologies for APU applications. The choice of battery for both main and APU applications depends on factors such as weight, energy density, cost, and environmental impact. As airlines and manufacturers strive to enhance operational efficiency and reduce carbon emissions, the demand for high-performance, reliable batteries in these areas is expected to grow. The Global Commercial Aircraft Battery Market is poised to play a significant role in supporting the aviation industry's transition towards more sustainable and efficient operations, with ongoing research and development efforts aimed at improving battery technology and performance.

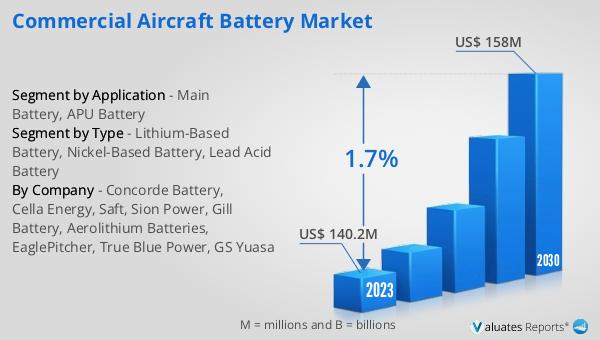

Global Commercial Aircraft Battery Market Outlook:

The worldwide market for Commercial Aircraft Batteries was valued at approximately $745 million in 2024. It is anticipated to expand to a revised size of around $923 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.5% over the forecast period. This growth trajectory underscores the increasing demand for advanced battery technologies in the aviation sector, driven by the need for more efficient, reliable, and environmentally friendly power solutions. As the aviation industry continues to evolve, the role of batteries becomes increasingly critical, particularly with the rise of electric and hybrid-electric aircraft. The projected growth in the market highlights the importance of ongoing research and development efforts aimed at enhancing battery performance, safety, and sustainability. With airlines and manufacturers seeking to improve operational efficiency and meet stringent environmental regulations, the Global Commercial Aircraft Battery Market is expected to play a pivotal role in shaping the future of aviation. The market's expansion is further supported by technological advancements and innovations that are driving the development of new battery solutions capable of meeting the demands of next-generation aircraft. As the industry continues to prioritize sustainability and efficiency, the demand for high-performance batteries is likely to grow, contributing to the overall growth of the Global Commercial Aircraft Battery Market.

| Report Metric | Details |

| Report Name | Commercial Aircraft Battery Market |

| Accounted market size in year | US$ 745 million |

| Forecasted market size in 2031 | US$ 923 million |

| CAGR | 3.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Concorde Battery, Cella Energy, Saft, Sion Power, Gill Battery, Aerolithium Batteries, Eagle-Picher, True Blue Power, GS Yuasa, Safran Power Units, Honeywell, GE Aviation, Lithium Balance |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |