What is Global Particle Size Analyzer Market?

The Global Particle Size Analyzer Market is a specialized segment within the broader analytical instruments industry, focusing on devices that measure the size distribution of particles in various materials. These analyzers are crucial in numerous industries, including pharmaceuticals, chemicals, food and beverages, and mining, as they help ensure product quality and consistency. Particle size can significantly affect the physical and chemical properties of materials, influencing factors such as solubility, stability, and appearance. The market for particle size analyzers is driven by the increasing demand for quality control and research and development across these sectors. Technological advancements have led to the development of more sophisticated and accurate analyzers, which are capable of measuring particles ranging from nanometers to millimeters in size. The market is characterized by a variety of technologies, each suited to different applications and particle size ranges. As industries continue to innovate and develop new materials, the demand for precise particle size analysis is expected to grow, making this market an essential component of modern industrial processes.

Laser Diffraction, Dynamic Light Scattering, Flow Imaging Analyzer, Static Particle Image Analyzer, Nanoparticle Tracking Analysis, Others in the Global Particle Size Analyzer Market:

The Global Particle Size Analyzer Market encompasses several key technologies, each with its unique methodology and application. Laser Diffraction is one of the most widely used techniques, known for its ability to measure a broad range of particle sizes quickly and accurately. It works by measuring the angle and intensity of light scattered by particles as a laser beam passes through a sample. This method is highly versatile and can be used for both wet and dry samples, making it suitable for industries like pharmaceuticals and food processing. Dynamic Light Scattering (DLS) is another popular technique, particularly for analyzing nanoparticles and colloids. DLS measures the fluctuations in light scattering due to the Brownian motion of particles in a suspension, providing information about particle size distribution. This method is highly sensitive and is often used in biopharmaceuticals and nanotechnology research. Flow Imaging Analyzers provide visual and quantitative data by capturing images of particles as they flow through a detection chamber. This technique is beneficial for applications where particle shape and morphology are as important as size, such as in the analysis of emulsions and suspensions. Static Particle Image Analyzers, on the other hand, capture images of stationary particles, allowing for detailed analysis of size and shape. This method is often used in quality control processes where precise measurements are critical. Nanoparticle Tracking Analysis (NTA) is a relatively newer technology that tracks the movement of individual nanoparticles in a fluid, providing high-resolution size distribution data. NTA is particularly useful in the fields of life sciences and environmental monitoring, where understanding the behavior of nanoparticles is crucial. Other methods in the market include sedimentation techniques and electrical sensing zone methods, each offering unique advantages depending on the specific requirements of the analysis. The diversity of technologies within the Global Particle Size Analyzer Market reflects the wide range of applications and industries that rely on accurate particle size measurement. As technology continues to advance, these methods are becoming more integrated and automated, offering enhanced precision and efficiency for users across various sectors.

Chemical Industry, Biopharmaceutical Industry, Scientific Research, Mining, Minerals and Cement Industry, Food and Beverage Industry, Others in the Global Particle Size Analyzer Market:

The Global Particle Size Analyzer Market finds extensive application across a variety of industries, each with its unique requirements and challenges. In the Chemical Industry, particle size analysis is crucial for ensuring the quality and performance of products such as paints, coatings, and polymers. The size of particles can affect the viscosity, stability, and appearance of chemical products, making precise measurement essential for quality control and product development. In the Biopharmaceutical Industry, particle size analyzers are used to ensure the efficacy and safety of drugs. The size of particles in pharmaceutical formulations can influence drug delivery, solubility, and bioavailability, making accurate analysis vital for compliance with regulatory standards. Scientific Research also heavily relies on particle size analysis, particularly in fields such as materials science and nanotechnology. Researchers use these analyzers to study the properties of new materials and to develop innovative applications. In the Mining, Minerals, and Cement Industry, particle size analysis is used to optimize the extraction and processing of raw materials. The size of particles can affect the efficiency of processes such as grinding and flotation, impacting the overall productivity and cost-effectiveness of operations. The Food and Beverage Industry uses particle size analyzers to ensure the quality and consistency of products such as flour, sugar, and emulsions. The size of particles can influence the texture, taste, and stability of food products, making precise measurement essential for maintaining product standards. Other industries, such as environmental monitoring and cosmetics, also benefit from particle size analysis, using it to ensure compliance with regulations and to develop new products. The versatility and importance of particle size analyzers across these diverse sectors highlight their critical role in modern industrial processes and research.

Global Particle Size Analyzer Market Outlook:

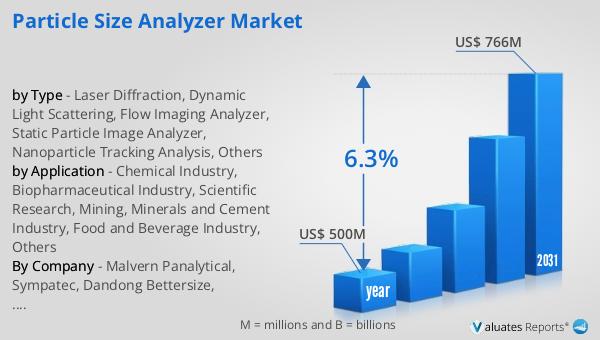

In 2024, the global market for Particle Size Analyzers was valued at approximately $500 million, with projections indicating a growth to around $766 million by 2031. This growth represents a compound annual growth rate (CAGR) of 6.3% over the forecast period. The market's expansion is driven by increasing demand for precise particle size measurement across various industries, including pharmaceuticals, chemicals, and food and beverages. In 2024, the top five players in the global market held a significant share, accounting for approximately 64.41% of the total revenue. This concentration of market share among leading companies highlights the competitive nature of the industry and the importance of technological innovation and product development in maintaining market position. As industries continue to evolve and new applications for particle size analysis emerge, the market is expected to see continued growth and diversification. The increasing focus on quality control, research and development, and regulatory compliance across various sectors will further drive the demand for advanced particle size analyzers, making this market a critical component of modern industrial and scientific processes.

| Report Metric | Details |

| Report Name | Particle Size Analyzer Market |

| Accounted market size in year | US$ 500 million |

| Forecasted market size in 2031 | US$ 766 million |

| CAGR | 6.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Malvern Panalytical, Sympatec, Dandong Bettersize, Micromeritics Instrument, Shimadzu, Anton Paar, Beckman Coulter, omec, Microtrac, Entegris, HORIBA, OTSUKA Electronics, Yokogawa Fluid Imaging Technologies, Fritsch, LS Instruments, Brookhaven Instruments, Jinan Winner Particle Instrument, Jinan Rise Science & Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |