What is Global Automotive LED Driver ICs Market?

The Global Automotive LED Driver ICs Market is a rapidly evolving sector that plays a crucial role in the automotive industry. LED Driver ICs, or Integrated Circuits, are essential components that manage the power and control of LED lighting systems in vehicles. These drivers ensure that LEDs operate efficiently, providing the necessary current and voltage to maintain optimal performance. The market for these components is driven by the increasing demand for energy-efficient and durable lighting solutions in automobiles. As vehicles become more advanced, the need for sophisticated lighting systems that enhance safety and aesthetics grows. LED Driver ICs are pivotal in this transformation, offering benefits such as lower energy consumption, longer lifespan, and improved light quality. The global market is witnessing significant growth due to technological advancements and the rising adoption of electric vehicles, which often incorporate advanced LED lighting systems. This market's expansion is further fueled by stringent regulations on vehicle emissions and energy efficiency, prompting manufacturers to adopt LED technology. As a result, the Global Automotive LED Driver ICs Market is poised for continued growth, driven by innovation and the increasing integration of LEDs in automotive applications.

Boost LED Driver, Buck-Boost LED Driver, Buck LED Driver, Linear Current Sources LED Driver in the Global Automotive LED Driver ICs Market:

In the realm of Global Automotive LED Driver ICs, several types of drivers are pivotal in ensuring the efficient operation of LED systems in vehicles. The Boost LED Driver is designed to increase the voltage from a lower input level to a higher output level, making it ideal for applications where the LED requires a higher voltage than what is available from the power source. This type of driver is particularly useful in automotive lighting systems where consistent brightness is crucial, such as in headlights. By boosting the voltage, these drivers ensure that the LEDs receive the necessary power to function optimally, even when the vehicle's battery voltage fluctuates. On the other hand, the Buck LED Driver operates by reducing the input voltage to a lower output level, which is suitable for applications where the LED operates at a lower voltage than the power source. This driver is commonly used in taillights and interior lighting systems, where the power requirements are less demanding. The Buck-Boost LED Driver combines the functionalities of both boost and buck drivers, offering versatility in applications where the input voltage can vary above or below the desired output voltage. This adaptability makes it a preferred choice for automotive systems that require stable performance across a range of operating conditions. Lastly, Linear Current Sources LED Drivers provide a constant current to the LEDs, ensuring uniform brightness and preventing damage due to overcurrent. These drivers are often used in applications where precise control over the LED current is necessary, such as in infotainment systems and ambient lighting. Each type of LED driver plays a critical role in the automotive industry, contributing to the overall efficiency, reliability, and performance of LED lighting systems in vehicles. As the demand for advanced lighting solutions continues to rise, the importance of these drivers in the Global Automotive LED Driver ICs Market cannot be overstated.

Headlights, Taillights/Interior Lights, Infotainment Systems, Others in the Global Automotive LED Driver ICs Market:

The usage of Global Automotive LED Driver ICs Market extends across various areas in vehicles, significantly enhancing functionality and aesthetics. In headlights, LED Driver ICs are crucial for providing the necessary power and control to ensure optimal brightness and energy efficiency. Headlights are essential for safe driving, especially at night or in adverse weather conditions, and LED technology offers superior illumination compared to traditional lighting solutions. The precise control offered by LED Driver ICs allows for adaptive lighting systems that can adjust the beam pattern based on driving conditions, improving visibility and safety. In taillights and interior lights, LED Driver ICs contribute to energy savings and longer lifespan. Taillights are vital for signaling and safety, and the reliability of LED technology ensures that they function effectively over the vehicle's lifetime. Interior lights, on the other hand, enhance the comfort and ambiance of the vehicle's cabin, and LED Driver ICs enable customizable lighting solutions that can be tailored to the driver's preferences. In infotainment systems, LED Driver ICs play a role in backlighting displays and enhancing the visual experience. These systems are becoming increasingly sophisticated, with high-resolution screens and dynamic lighting effects that require precise control and power management. LED Driver ICs ensure that these systems operate efficiently, providing clear and vibrant displays that enhance the overall driving experience. Beyond these applications, LED Driver ICs are also used in other automotive systems, such as ambient lighting and exterior accent lights, where they contribute to the vehicle's aesthetic appeal and brand identity. The versatility and efficiency of LED Driver ICs make them indispensable in modern automotive design, supporting the industry's shift towards more sustainable and technologically advanced vehicles.

Global Automotive LED Driver ICs Market Outlook:

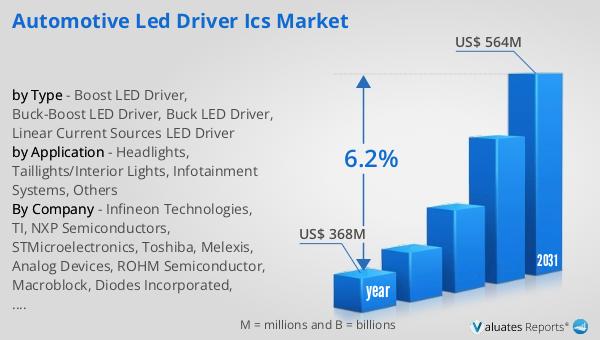

The global market for Automotive LED Driver ICs was valued at $368 million in 2024 and is anticipated to grow to a revised size of $564 million by 2031, reflecting a compound annual growth rate (CAGR) of 6.2% during the forecast period. This growth is indicative of the increasing demand for energy-efficient and advanced lighting solutions in the automotive sector. In 2022, China's production and sales of new energy vehicles reached 7.058 million and 6.887 million units, respectively, marking a significant year-on-year increase of 96.9% and 93.4%. This surge in production and sales highlights the rapid adoption of new energy vehicles, which often incorporate advanced LED lighting systems. Similarly, in Europe, the sales of pure electric vehicles rose by 29% year-on-year to 1.58 million units in 2022, underscoring the region's commitment to sustainable transportation solutions. The growing popularity of electric vehicles, coupled with stringent regulations on vehicle emissions and energy efficiency, is driving the demand for LED Driver ICs in the automotive industry. As manufacturers continue to innovate and integrate advanced lighting technologies into their vehicles, the market for Automotive LED Driver ICs is expected to expand further, supporting the industry's transition towards more sustainable and efficient transportation solutions.

| Report Metric | Details |

| Report Name | Automotive LED Driver ICs Market |

| Accounted market size in year | US$ 368 million |

| Forecasted market size in 2031 | US$ 564 million |

| CAGR | 6.2% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Infineon Technologies, TI, NXP Semiconductors, STMicroelectronics, Toshiba, Melexis, Analog Devices, ROHM Semiconductor, Macroblock, Diodes Incorporated, Nexperia, Princeton Technology Corporation, Renesas Electronics Corporation, onsemi, Microchip Technology, Suzhou Novosense Microelectronics Co.,Ltd, Monolithic Power Systems, SG Micro, Indie Inc |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |