What is Medical and Food Grade Stainless Steel Springs - Global Market?

Medical and food grade stainless steel springs are specialized components designed to meet the stringent requirements of the healthcare and food industries. These springs are crafted from high-quality stainless steel, which is known for its excellent corrosion resistance, durability, and ability to withstand extreme temperatures. In the global market, these springs are essential for various applications, ensuring safety and reliability in medical devices and food processing equipment. The demand for these springs is driven by the need for hygienic and safe materials that can endure rigorous cleaning and sterilization processes. Stainless steel springs are used in a wide range of products, from surgical instruments and diagnostic equipment to food processing machinery and packaging systems. Their versatility and reliability make them indispensable in maintaining the integrity and functionality of critical systems in both the medical and food sectors. As industries continue to prioritize safety and efficiency, the global market for medical and food grade stainless steel springs is expected to grow, reflecting the increasing emphasis on quality and compliance with international standards. These springs play a crucial role in ensuring that medical and food products are safe for consumption and use, highlighting their importance in the global market landscape.

Tension Spring, Compressed Spring, Torsion Spring, Precision Spring, Others in the Medical and Food Grade Stainless Steel Springs - Global Market:

Tension springs, compressed springs, torsion springs, precision springs, and other types of springs are integral components in the medical and food grade stainless steel springs market. Tension springs, also known as extension springs, are designed to absorb and store energy by resisting a pulling force. They are commonly used in medical devices such as ventilators and infusion pumps, where precise control and reliability are crucial. In the food industry, tension springs are employed in machinery that requires consistent tension to function effectively, such as conveyor belts and packaging equipment. Compressed springs, on the other hand, are designed to resist a compressive force and are widely used in applications where space is limited. In the medical field, compressed springs are found in devices like syringes and inhalers, where they provide the necessary force to deliver medication accurately. In food processing, these springs are used in equipment that requires precise pressure control, such as sealing machines and pressure cookers. Torsion springs are designed to work by twisting and are used in applications that require rotational force. In the medical industry, torsion springs are used in surgical instruments and orthopedic devices, where they provide the necessary torque for precise movements. In the food sector, torsion springs are used in equipment like mixers and blenders, where they help in achieving the desired consistency and texture of food products. Precision springs are specialized springs that are manufactured to exact specifications, ensuring high performance and reliability. In the medical industry, precision springs are used in devices like pacemakers and hearing aids, where accuracy and dependability are paramount. In the food industry, precision springs are used in equipment that requires precise control, such as dosing machines and filling systems. Other types of springs, such as leaf springs and wave springs, also play a significant role in the medical and food grade stainless steel springs market. Leaf springs are used in applications that require a smooth and consistent force, such as in prosthetic devices and food processing equipment. Wave springs, known for their compact design and ability to provide high force in a small space, are used in applications where space is limited, such as in medical implants and compact food processing machinery. The global market for these springs is driven by the increasing demand for high-quality, reliable components that meet the stringent requirements of the medical and food industries. As these industries continue to evolve and innovate, the demand for specialized springs is expected to grow, reflecting the need for components that can withstand the challenges of modern applications.

Medical, Food and Beverages, Others in the Medical and Food Grade Stainless Steel Springs - Global Market:

Medical and food grade stainless steel springs are used extensively in the medical, food and beverages, and other industries due to their unique properties and versatility. In the medical field, these springs are crucial components in a wide range of devices and equipment. They are used in surgical instruments, where their corrosion resistance and durability ensure that they can withstand repeated sterilization processes without compromising performance. Stainless steel springs are also used in diagnostic equipment, such as MRI machines and CT scanners, where they provide the necessary force and precision for accurate results. In addition, these springs are used in medical implants, such as stents and pacemakers, where their biocompatibility and strength are essential for patient safety and long-term performance. In the food and beverages industry, stainless steel springs are used in various applications to ensure the safety and quality of food products. They are used in food processing equipment, such as mixers, blenders, and conveyor systems, where their resistance to corrosion and ability to withstand high temperatures are crucial for maintaining hygiene and efficiency. Stainless steel springs are also used in packaging machinery, where they provide the necessary tension and compression to ensure that food products are securely packaged and protected from contamination. In addition to the medical and food industries, stainless steel springs are used in other sectors, such as automotive and aerospace, where their strength, durability, and resistance to harsh environments make them ideal for demanding applications. In the automotive industry, stainless steel springs are used in suspension systems, where they provide the necessary support and stability for vehicles. In the aerospace industry, these springs are used in various components, such as landing gear and control systems, where their reliability and performance are critical for safety and efficiency. The global market for medical and food grade stainless steel springs is driven by the increasing demand for high-quality, reliable components that meet the stringent requirements of these industries. As technology continues to advance and industries evolve, the demand for specialized springs is expected to grow, reflecting the need for components that can withstand the challenges of modern applications.

Medical and Food Grade Stainless Steel Springs - Global Market Outlook:

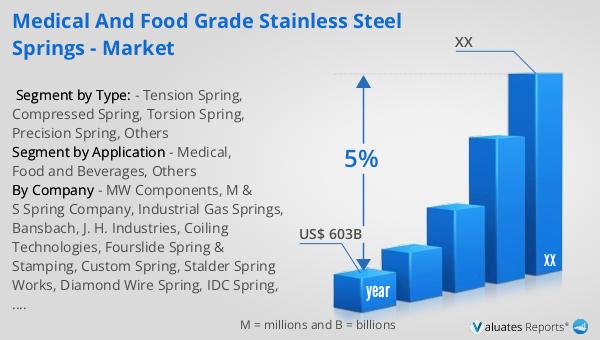

The global market for medical devices is experiencing significant growth, with an estimated value of $603 billion in 2023. This growth is expected to continue at a compound annual growth rate (CAGR) of 5% over the next six years. This expansion is driven by several factors, including the increasing demand for advanced medical technologies, the rising prevalence of chronic diseases, and the growing aging population. As healthcare systems worldwide strive to improve patient outcomes and reduce costs, the demand for innovative medical devices is expected to rise. This growth presents significant opportunities for manufacturers and suppliers of medical and food grade stainless steel springs, as these components are essential for the development and production of high-quality medical devices. The increasing focus on safety, reliability, and compliance with international standards is also driving the demand for these specialized springs, as they play a crucial role in ensuring the performance and longevity of medical devices. As the global market for medical devices continues to expand, the demand for medical and food grade stainless steel springs is expected to grow, reflecting the increasing emphasis on quality and innovation in the healthcare industry.

| Report Metric | Details |

| Report Name | Medical and Food Grade Stainless Steel Springs - Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | MW Components, M & S Spring Company, Industrial Gas Springs, Bansbach, J. H. Industries, Coiling Technologies, Fourslide Spring & Stamping, Custom Spring, Stalder Spring Works, Diamond Wire Spring, IDC Spring, R&L Spring Company, Airedale Springs |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |