What is Mobile Screening Machine - Global Market?

Mobile screening machines are versatile equipment used across various industries to separate and sort materials based on size. These machines are crucial in sectors like mining, construction, and recycling, where they help streamline operations by efficiently sorting materials. The global market for mobile screening machines is driven by the increasing demand for efficient material handling solutions. These machines are designed to be easily transported and set up, making them ideal for use in remote locations or on sites where space is limited. They come equipped with advanced technology that allows for precise screening, ensuring that only the desired material sizes are collected. The market is characterized by a range of machines with varying capacities and features, catering to different industry needs. As industries continue to prioritize efficiency and sustainability, the demand for mobile screening machines is expected to grow, with manufacturers focusing on innovation to meet evolving customer requirements. The global market is competitive, with several key players offering a wide range of products to meet the diverse needs of their clients.

Capacity Less Than 300 Ton/h, 300-500 Ton/h, Capacity More Than 500 Ton/h in the Mobile Screening Machine - Global Market:

Mobile screening machines are categorized based on their capacity, which determines the volume of material they can process per hour. Machines with a capacity of less than 300 tons per hour are typically used in smaller operations or where the material volume is not very high. These machines are compact and easy to maneuver, making them ideal for use in urban areas or sites with limited space. They are often used in construction projects where the material needs to be sorted quickly and efficiently. On the other hand, machines with a capacity of 300-500 tons per hour are suitable for medium-sized operations. These machines offer a balance between capacity and mobility, making them versatile for use in various industries. They are often used in mining operations where the material needs to be processed at a moderate pace. Machines with a capacity of more than 500 tons per hour are designed for large-scale operations where high volumes of material need to be processed quickly. These machines are robust and durable, capable of handling the toughest materials. They are often used in large mining operations or in industries where the material needs to be processed continuously. The choice of machine capacity depends on several factors, including the volume of material to be processed, the nature of the material, and the specific requirements of the operation. Manufacturers offer a range of machines with different capacities to cater to the diverse needs of their clients. The global market for mobile screening machines is expected to grow as industries continue to seek efficient and cost-effective solutions for material handling. Manufacturers are focusing on innovation and technology to enhance the performance and efficiency of these machines, ensuring they meet the evolving needs of their customers.

Mining, Aggregates in the Mobile Screening Machine - Global Market:

Mobile screening machines play a crucial role in the mining and aggregates industries by enhancing operational efficiency and productivity. In the mining sector, these machines are used to separate valuable minerals from waste material, ensuring that only the desired minerals are extracted. This process is essential for maximizing the yield and profitability of mining operations. Mobile screening machines are designed to handle the harsh conditions of mining sites, with robust construction and advanced technology that allows for precise screening. They are used in various stages of the mining process, from initial exploration to final processing, helping to streamline operations and reduce costs. In the aggregates industry, mobile screening machines are used to sort and separate different sizes of aggregates, such as sand, gravel, and crushed stone. This process is essential for producing high-quality construction materials that meet industry standards. Mobile screening machines are ideal for use in quarries and construction sites, where they can be easily transported and set up to process materials on-site. This flexibility allows for efficient material handling and reduces the need for transportation, saving time and costs. The use of mobile screening machines in these industries is driven by the need for efficient and cost-effective solutions for material processing. As industries continue to prioritize sustainability and efficiency, the demand for mobile screening machines is expected to grow, with manufacturers focusing on innovation and technology to meet the evolving needs of their customers.

Mobile Screening Machine - Global Market Outlook:

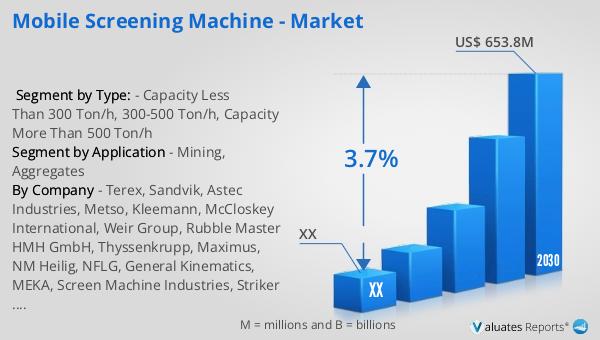

The global market for mobile screening machines was valued at approximately $515.3 million in 2023. Looking ahead, it is projected to reach an adjusted size of around $653.8 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.7% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for efficient material handling solutions across various industries. As industries continue to prioritize efficiency and sustainability, the demand for mobile screening machines is expected to grow, with manufacturers focusing on innovation to meet evolving customer requirements. The market is characterized by a range of machines with varying capacities and features, catering to different industry needs. The global market is competitive, with several key players offering a wide range of products to meet the diverse needs of their clients. The projected growth in the market reflects the increasing demand for efficient material handling solutions across various industries. As industries continue to prioritize efficiency and sustainability, the demand for mobile screening machines is expected to grow, with manufacturers focusing on innovation to meet evolving customer requirements.

| Report Metric | Details |

| Report Name | Mobile Screening Machine - Market |

| Forecasted market size in 2030 | US$ 653.8 million |

| CAGR | 3.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Terex, Sandvik, Astec Industries, Metso, Kleemann, McCloskey International, Weir Group, Rubble Master HMH GmbH, Thyssenkrupp, Maximus, NM Heilig, NFLG, General Kinematics, MEKA, Screen Machine Industries, Striker Australia |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |