What is Global Functional Additives for Feed Market?

The Global Functional Additives for Feed Market refers to a specialized segment within the broader animal feed industry that focuses on enhancing the nutritional value, safety, and overall quality of animal feed. These additives are incorporated into animal feed to promote better health, improve growth rates, and enhance the overall productivity of livestock. Functional additives can include a variety of substances such as antibiotics, immune boosters, antioxidants, probiotics, preservatives, adhesives, colorants, and other specialized compounds. These additives are essential for ensuring that animals receive a balanced diet that meets their nutritional needs, supports their immune systems, and protects them from diseases. The market for these additives is driven by the increasing demand for high-quality animal products, such as meat, poultry, and eggs, as well as the growing awareness of the importance of animal health and welfare. As a result, the Global Functional Additives for Feed Market is expected to continue expanding, driven by advancements in animal nutrition science and the ongoing need for sustainable and efficient livestock production practices.

Antibiotic, Immune Booster, Antioxidants, Probiotics, Preservative, Adhesive, Colorant, Others in the Global Functional Additives for Feed Market:

Antibiotics are one of the most commonly used functional additives in animal feed, primarily to prevent and treat bacterial infections in livestock. They help in maintaining animal health, reducing mortality rates, and improving feed efficiency. However, the use of antibiotics in animal feed has become a controversial topic due to concerns about antibiotic resistance. Immune boosters are another critical category of functional additives. These substances enhance the immune system of animals, making them more resistant to diseases and infections. They can include vitamins, minerals, and other bioactive compounds that support overall health. Antioxidants are added to animal feed to protect the feed from oxidative damage, which can degrade its nutritional quality. They also help in maintaining the health of animals by neutralizing harmful free radicals in their bodies. Probiotics are beneficial bacteria that are added to animal feed to improve gut health and digestion. They help in maintaining a healthy balance of gut microbiota, which is essential for nutrient absorption and overall health. Preservatives are used to extend the shelf life of animal feed by preventing the growth of mold, bacteria, and other microorganisms. This ensures that the feed remains safe and nutritious for a longer period. Adhesives are added to feed to improve its texture and binding properties, making it easier for animals to consume. Colorants are used to enhance the visual appeal of feed, which can be important for certain types of livestock. Other functional additives can include enzymes, amino acids, and flavor enhancers, each serving a specific purpose in improving the quality and effectiveness of animal feed. The use of these additives is regulated by various governmental and industry standards to ensure their safety and efficacy. Overall, the diverse range of functional additives available in the Global Functional Additives for Feed Market plays a crucial role in supporting the health and productivity of livestock, contributing to the sustainability and efficiency of animal agriculture.

Meat Poultry, Egg Poultry, Others in the Global Functional Additives for Feed Market:

The usage of Global Functional Additives for Feed Market in meat poultry is significant, as these additives help in improving the growth rates, feed efficiency, and overall health of broiler chickens. Antibiotics, for instance, are often used to prevent and treat bacterial infections, ensuring that the chickens remain healthy and productive. Immune boosters and probiotics are also commonly used in meat poultry feed to enhance the immune system and improve gut health, respectively. These additives help in reducing the incidence of diseases and improving nutrient absorption, leading to better growth and higher meat yields. Antioxidants and preservatives are added to meat poultry feed to protect the feed from oxidative damage and microbial contamination, ensuring that the feed remains safe and nutritious. Adhesives and colorants are used to improve the texture and visual appeal of the feed, making it more palatable for the chickens. In egg poultry, functional additives play a crucial role in enhancing the health and productivity of laying hens. Antibiotics and immune boosters are used to prevent and treat infections, while probiotics help in maintaining a healthy gut microbiota. Antioxidants are added to protect the feed from oxidative damage and improve the overall health of the hens. Preservatives are used to extend the shelf life of the feed, ensuring that it remains safe and nutritious. Adhesives and colorants are used to improve the texture and visual appeal of the feed, making it more palatable for the hens. In other livestock, such as cattle, pigs, and aquaculture, functional additives are used to improve growth rates, feed efficiency, and overall health. Antibiotics, immune boosters, probiotics, antioxidants, preservatives, adhesives, and colorants are all commonly used in these types of feed to ensure that the animals receive a balanced diet that meets their nutritional needs and supports their overall health. The use of functional additives in these areas is essential for ensuring the sustainability and efficiency of livestock production, as they help in improving the health and productivity of the animals, reducing the incidence of diseases, and enhancing the overall quality of animal products.

Global Functional Additives for Feed Market Outlook:

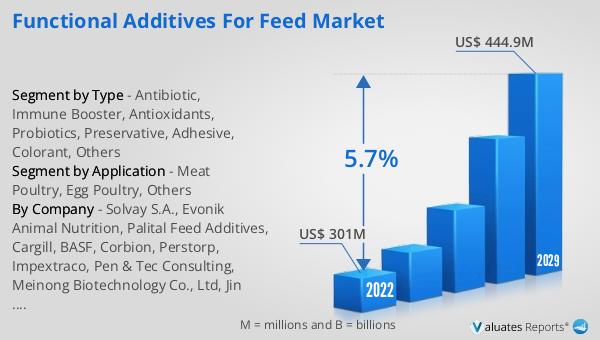

The global Functional Additives for Feed market was valued at US$ 301 million in 2023 and is anticipated to reach US$ 444.9 million by 2030, witnessing a CAGR of 5.7% during the forecast period 2024-2030. This significant growth can be attributed to the increasing demand for high-quality animal products and the growing awareness of the importance of animal health and welfare. As consumers become more conscious of the quality and safety of the food they consume, there is a rising demand for meat, poultry, and eggs that are produced using sustainable and efficient practices. Functional additives play a crucial role in meeting this demand by enhancing the nutritional value, safety, and overall quality of animal feed. The market is also driven by advancements in animal nutrition science, which have led to the development of new and innovative functional additives that can improve the health and productivity of livestock. Additionally, the increasing focus on reducing the environmental impact of livestock production is expected to further drive the demand for functional additives, as they can help in improving feed efficiency and reducing waste. Overall, the Global Functional Additives for Feed Market is poised for significant growth in the coming years, driven by the increasing demand for high-quality animal products and the ongoing advancements in animal nutrition science.

| Report Metric | Details |

| Report Name | Functional Additives for Feed Market |

| Accounted market size in 2023 | US$ 301 million |

| Forecasted market size in 2030 | US$ 444.9 million |

| CAGR | 5.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Solvay S.A., Evonik Animal Nutrition, Palital Feed Additives, Cargill, BASF, Corbion, Perstorp, Impextraco, Pen & Tec Consulting, Meinong Biotechnology Co., Ltd, Jin Xinnong, VTR BioTech |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |