What is Global High-performance Computing System Market?

The Global High-performance Computing (HPC) System Market refers to the market for advanced computing systems that deliver high levels of performance through the use of parallel processing techniques. These systems are designed to solve complex computational problems that require significant processing power, memory, and storage capabilities. HPC systems are utilized in a variety of industries, including scientific research, engineering, financial modeling, and data analysis, to perform tasks that would be infeasible or too time-consuming on standard computers. The market encompasses a range of products and services, including supercomputers, clusters, and software solutions that enable efficient and effective high-performance computing. As technology continues to advance, the demand for HPC systems is expected to grow, driven by the increasing need for data processing and analysis in various sectors.

Software and Service, Hardware in the Global High-performance Computing System Market:

In the Global High-performance Computing System Market, both software and services, as well as hardware, play crucial roles. On the software and services side, HPC systems require specialized software to manage and optimize the performance of the hardware. This includes operating systems, middleware, and application software that are designed to handle parallel processing and large-scale computations. Middleware, for example, helps in managing the communication between different nodes in a cluster, ensuring that tasks are distributed efficiently. Application software, on the other hand, is tailored to specific industries and use cases, such as simulations in engineering or data analysis in finance. Services related to HPC systems include consulting, system integration, and support services. These services are essential for organizations to effectively deploy and maintain their HPC infrastructure, ensuring that they can achieve the desired performance and efficiency. On the hardware side, HPC systems are composed of various components that work together to deliver high performance. The primary components include processors, memory, storage, and networking equipment. Processors, or CPUs, are the brains of the HPC system, executing instructions and performing calculations. In many HPC systems, GPUs (Graphics Processing Units) are also used to accelerate certain types of computations, particularly those involving large-scale data processing and machine learning. Memory, or RAM, is critical for storing data that the processors need to access quickly. High-speed memory is essential for ensuring that the processors can work efficiently without being bottlenecked by slow data access. Storage solutions in HPC systems are designed to handle large volumes of data and provide fast read and write speeds. This often involves the use of SSDs (Solid State Drives) and other high-performance storage technologies. Networking equipment, such as high-speed switches and routers, is used to connect the various components of the HPC system, enabling fast data transfer between nodes. The integration of these hardware components is crucial for achieving the desired performance in HPC systems. This often involves custom configurations and optimizations to ensure that the system can handle the specific workloads it is designed for. For example, an HPC system used for scientific simulations may require a different configuration than one used for financial modeling. Additionally, cooling and power management are important considerations in HPC systems, as the high-performance hardware generates significant heat and consumes substantial amounts of power. Effective cooling solutions, such as liquid cooling, are often used to maintain optimal operating temperatures and prevent overheating. Overall, the Global High-performance Computing System Market is characterized by a complex interplay of software, services, and hardware components. Each of these elements is essential for delivering the high levels of performance required for advanced computational tasks. As the demand for HPC systems continues to grow, driven by advancements in technology and increasing data processing needs, the market is expected to see continued innovation and development in both software and hardware solutions. Organizations across various industries will continue to rely on HPC systems to solve complex problems, drive innovation, and gain a competitive edge.

Government & Defense, Banking, Financial Services, and Insurance, Earth Sciences, Education & Research, Healthcare & Life Sciences, Energy & Utilities, Gaming, Manufacturing, Others in the Global High-performance Computing System Market:

The usage of Global High-performance Computing (HPC) Systems spans across various sectors, each leveraging the immense computational power to address specific challenges and drive innovation. In Government & Defense, HPC systems are used for simulations, cryptographic analysis, and intelligence operations. These systems enable the processing of vast amounts of data to enhance national security, develop advanced defense technologies, and support strategic decision-making. In the Banking, Financial Services, and Insurance (BFSI) sector, HPC systems are employed for risk management, fraud detection, and high-frequency trading. The ability to process and analyze large datasets in real-time allows financial institutions to make informed decisions, optimize trading strategies, and mitigate risks effectively. In Earth Sciences, HPC systems play a crucial role in climate modeling, weather forecasting, and seismic analysis. These systems enable scientists to run complex simulations that predict weather patterns, study climate change, and assess natural disaster risks. The insights gained from these simulations are vital for environmental planning, disaster preparedness, and policy-making. In the field of Education & Research, HPC systems are used to support advanced research projects, from genomics to astrophysics. Universities and research institutions leverage HPC to conduct experiments, analyze large datasets, and develop new theories, driving scientific discovery and innovation. Healthcare & Life Sciences is another sector where HPC systems have a significant impact. These systems are used for drug discovery, genomics, and medical imaging. By processing large volumes of biological data, HPC systems enable researchers to identify potential drug candidates, understand genetic variations, and develop personalized medicine approaches. In Energy & Utilities, HPC systems are used for reservoir simulation, grid management, and renewable energy research. These systems help energy companies optimize resource extraction, manage energy distribution, and develop sustainable energy solutions. The Gaming industry also benefits from HPC systems, particularly in the development of complex game environments and real-time rendering. HPC systems enable game developers to create highly detailed graphics, simulate realistic physics, and provide immersive gaming experiences. In Manufacturing, HPC systems are used for product design, simulation, and optimization. These systems allow manufacturers to run simulations that test product performance, identify design flaws, and optimize production processes, leading to improved product quality and reduced time-to-market. Other sectors, such as telecommunications, retail, and transportation, also leverage HPC systems to address specific challenges and drive innovation. In telecommunications, HPC systems are used for network optimization and data analysis, enabling service providers to enhance network performance and deliver better customer experiences. In retail, HPC systems support demand forecasting, inventory management, and customer analytics, helping retailers optimize operations and improve customer satisfaction. In transportation, HPC systems are used for traffic modeling, route optimization, and autonomous vehicle development, contributing to safer and more efficient transportation systems. Overall, the usage of Global High-performance Computing Systems across these diverse sectors highlights the versatility and importance of HPC technology. By enabling the processing and analysis of large datasets, running complex simulations, and supporting advanced research, HPC systems drive innovation, improve decision-making, and address critical challenges in various industries. As technology continues to advance, the adoption of HPC systems is expected to grow, further expanding their impact and applications across different sectors.

Global High-performance Computing System Market Outlook:

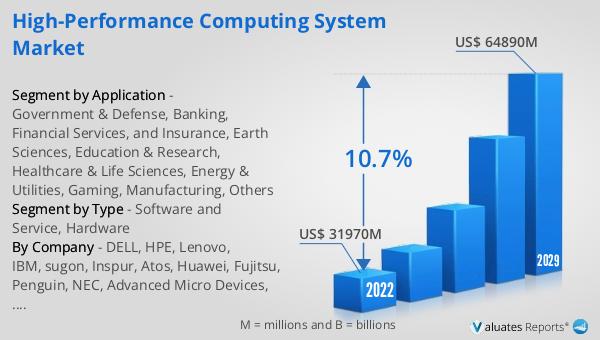

The global High-performance Computing (HPC) System market was valued at US$ 31,970 million in 2023 and is projected to reach US$ 64,890 million by 2030, reflecting a compound annual growth rate (CAGR) of 10.7% during the forecast period from 2024 to 2030. This significant growth underscores the increasing demand for advanced computing solutions across various industries. HPC systems are becoming essential tools for organizations that require substantial computational power to process large datasets, run complex simulations, and perform high-speed calculations. The market's expansion is driven by technological advancements, the growing importance of data analytics, and the need for efficient and effective computing solutions. As industries continue to evolve and face new challenges, the adoption of HPC systems is expected to rise, further fueling market growth.

| Report Metric | Details |

| Report Name | High-performance Computing System Market |

| Accounted market size in 2023 | US$ 31970 million |

| Forecasted market size in 2030 | US$ 64890 million |

| CAGR | 10.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | DELL, HPE, Lenovo, IBM, sugon, Inspur, Atos, Huawei, Fujitsu, Penguin, NEC, Advanced Micro Devices, Nvidia |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |