What is Global Hazardous Location Lighting Fixtures Market?

The Global Hazardous Location Lighting Fixtures Market refers to the specialized segment of the lighting industry that focuses on providing illumination solutions for environments where there is a significant risk of explosions or fires due to the presence of flammable gases, vapors, dust, or fibers. These lighting fixtures are designed to operate safely in such hazardous conditions, ensuring that they do not become a source of ignition. Industries such as oil and gas, mining, chemical manufacturing, and others that operate in potentially explosive atmospheres rely heavily on these lighting solutions to maintain safety and operational efficiency. The market for these fixtures is driven by stringent safety regulations, technological advancements, and the need for reliable and durable lighting solutions in hazardous environments. As industries continue to prioritize safety and compliance, the demand for hazardous location lighting fixtures is expected to grow.

LED, Fluorescent, Incandescent, High Pressure Sodium, Others in the Global Hazardous Location Lighting Fixtures Market:

In the Global Hazardous Location Lighting Fixtures Market, various types of lighting technologies are employed to meet the specific needs of different hazardous environments. LED (Light Emitting Diode) lighting is one of the most popular choices due to its energy efficiency, long lifespan, and low maintenance requirements. LEDs are highly durable and can withstand harsh conditions, making them ideal for hazardous locations. Fluorescent lighting, although less energy-efficient than LEDs, is still widely used due to its relatively low cost and good light output. Fluorescent fixtures are often used in areas where a broad, even light distribution is needed. Incandescent lighting, while being one of the oldest technologies, is less common in hazardous locations due to its lower energy efficiency and shorter lifespan. However, it is still used in some applications where its warm light and instant-on capabilities are desired. High Pressure Sodium (HPS) lighting is known for its high efficiency and long life, making it suitable for outdoor and industrial applications. HPS lights produce a yellow-orange light, which can be beneficial in certain environments where color rendering is not a critical factor. Other types of lighting technologies used in hazardous locations include metal halide and induction lighting. Metal halide lights offer good color rendering and high light output, making them suitable for areas where visual clarity is important. Induction lighting, on the other hand, is known for its long lifespan and low maintenance requirements, making it a good choice for hard-to-reach areas. Each of these lighting technologies has its own set of advantages and disadvantages, and the choice of technology often depends on the specific requirements of the hazardous location, such as the type of hazard present, the required light levels, and the environmental conditions.

Oil, Mining & Steel, Railway, Electricity, Military & Public Safety, Others in the Global Hazardous Location Lighting Fixtures Market:

The usage of Global Hazardous Location Lighting Fixtures Market spans across various critical industries, ensuring safety and operational efficiency in environments prone to explosive hazards. In the oil industry, these lighting fixtures are essential for illuminating drilling rigs, refineries, and storage facilities where flammable gases and vapors are present. They help prevent accidents by providing reliable lighting that does not ignite these hazardous substances. In the mining and steel industries, hazardous location lighting fixtures are used to light up underground mines, processing plants, and steel mills. These environments often contain combustible dust and fibers, making explosion-proof lighting crucial for worker safety and productivity. The railway industry also relies on these specialized lighting solutions for illuminating tunnels, maintenance areas, and other critical infrastructure where explosive gases or dust may be present. In the electricity sector, hazardous location lighting fixtures are used in power plants, substations, and other facilities where flammable gases or vapors could pose a risk. These fixtures ensure that electrical operations can be carried out safely without the risk of ignition. The military and public safety sectors utilize hazardous location lighting fixtures in various applications, including ammunition storage, fuel depots, and emergency response scenarios. These fixtures provide reliable lighting in potentially explosive environments, ensuring the safety of personnel and equipment. Other industries that benefit from hazardous location lighting fixtures include chemical manufacturing, pharmaceuticals, and food processing. In these sectors, the presence of flammable substances or dust necessitates the use of explosion-proof lighting to maintain safety and compliance with regulations. Overall, the usage of hazardous location lighting fixtures is critical in ensuring the safety and efficiency of operations in various industries where explosive hazards are a concern.

Global Hazardous Location Lighting Fixtures Market Outlook:

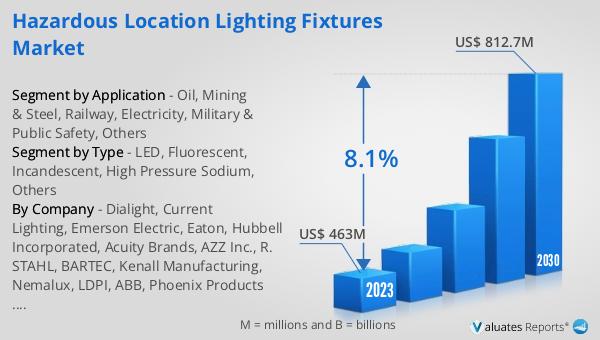

The global Hazardous Location Lighting Fixtures market was valued at US$ 463 million in 2023 and is anticipated to reach US$ 812.7 million by 2030, witnessing a CAGR of 8.1% during the forecast period 2024-2030. This significant growth reflects the increasing demand for reliable and safe lighting solutions in industries operating in hazardous environments. The market's expansion is driven by stringent safety regulations, technological advancements, and the need for durable lighting fixtures that can withstand harsh conditions. As industries such as oil and gas, mining, and chemical manufacturing continue to prioritize safety and compliance, the demand for hazardous location lighting fixtures is expected to rise. The market's growth also highlights the importance of innovation and the development of new lighting technologies that can meet the specific needs of hazardous environments. With the ongoing focus on safety and efficiency, the global Hazardous Location Lighting Fixtures market is poised for substantial growth in the coming years.

| Report Metric | Details |

| Report Name | Hazardous Location Lighting Fixtures Market |

| Accounted market size in 2023 | US$ 463 million |

| Forecasted market size in 2030 | US$ 812.7 million |

| CAGR | 8.1% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dialight, Current Lighting, Emerson Electric, Eaton, Hubbell Incorporated, Acuity Brands, AZZ Inc., R. STAHL, BARTEC, Kenall Manufacturing, Nemalux, LDPI, ABB, Phoenix Products Company, Larson Electronics, Unimar, Solas Ray Lighting, Western Technology, Lind Equipment, Warom Technology Inc, Ocean's King Lighting |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |