What is Global Ready-made Flour Market?

The Global Ready-made Flour Market encompasses a wide range of pre-mixed flour products that are designed to simplify the cooking and baking process for consumers and businesses alike. These products include various types of flour blends that are pre-mixed with other ingredients such as leavening agents, salt, and sometimes even flavorings. The convenience offered by ready-made flour products has made them increasingly popular among busy households, professional bakers, and food processing companies. These products save time and effort, ensuring consistent quality and results. The market for ready-made flour is driven by the growing demand for convenience foods, the increasing number of working women, and the rising trend of home baking. Additionally, the market is also influenced by the growing awareness of health and wellness, leading to the introduction of healthier flour blends, such as whole grain and gluten-free options. The global ready-made flour market is expected to continue its growth trajectory, driven by these factors and the increasing penetration of these products in emerging markets.

Batter Mixes, Bread Mixes, Pastry Mixes in the Global Ready-made Flour Market:

Batter mixes, bread mixes, and pastry mixes are essential components of the global ready-made flour market, each catering to different culinary needs and preferences. Batter mixes are pre-mixed flour blends designed for making a variety of batters, such as those used for pancakes, waffles, and tempura. These mixes typically contain flour, leavening agents, sugar, and sometimes flavorings, making it easy for consumers to prepare consistent and delicious batters with minimal effort. Bread mixes, on the other hand, are formulated to simplify the bread-making process. They usually include flour, yeast, salt, and sometimes additional ingredients like seeds, nuts, or dried fruits. Bread mixes are popular among home bakers and small bakeries, as they ensure consistent results and save time compared to making bread from scratch. Pastry mixes are designed for making a variety of pastries, such as pie crusts, tarts, and puff pastries. These mixes often contain flour, fat, sugar, and other ingredients that help achieve the desired texture and flavor of the pastry. The convenience offered by these ready-made mixes has made them popular among both amateur and professional bakers. The global market for these products is driven by the increasing demand for convenience foods, the growing popularity of home baking, and the rising number of small bakeries and cafes. Additionally, the introduction of healthier and specialty mixes, such as gluten-free and whole grain options, has further expanded the market. As consumers continue to seek convenience and quality in their baking endeavors, the demand for batter mixes, bread mixes, and pastry mixes is expected to grow.

Household, Bakery Shop, Food Processing, Others in the Global Ready-made Flour Market:

The usage of ready-made flour products spans various areas, including households, bakery shops, food processing, and other sectors. In households, ready-made flour products are a boon for busy individuals and families who want to prepare home-cooked meals and baked goods without spending too much time on preparation. These products simplify the cooking and baking process, allowing even novice cooks to achieve consistent and delicious results. Ready-made flour products are also popular among home bakers who enjoy making bread, cakes, and pastries but prefer the convenience of pre-mixed ingredients. In bakery shops, ready-made flour products are used to streamline operations and ensure consistent quality in baked goods. Small bakeries and cafes often rely on these products to save time and reduce the complexity of their baking processes. Ready-made flour products also help bakery shops maintain a consistent flavor and texture in their offerings, which is crucial for customer satisfaction. In the food processing industry, ready-made flour products are used to produce a wide range of convenience foods, such as pre-packaged baked goods, snacks, and ready-to-eat meals. These products help food manufacturers achieve consistent quality and reduce production time, making them an essential component of the food processing industry. Other sectors that use ready-made flour products include restaurants, catering services, and institutional kitchens. These establishments benefit from the convenience and consistency offered by ready-made flour products, allowing them to serve high-quality meals and baked goods to their customers. The versatility and convenience of ready-made flour products make them a valuable addition to various culinary applications, driving their demand across different sectors.

Global Ready-made Flour Market Outlook:

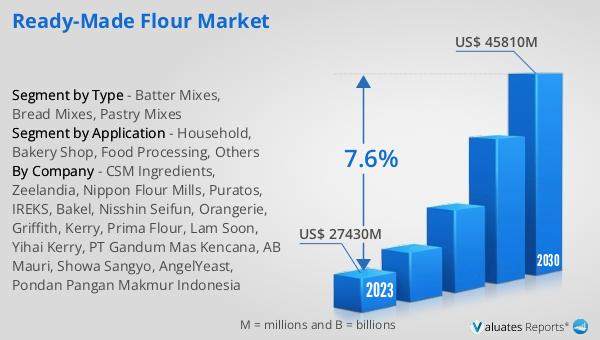

The global ready-made flour market was valued at approximately US$ 27.43 billion in 2023 and is projected to reach around US$ 45.81 billion by 2030, reflecting a compound annual growth rate (CAGR) of 7.6% during the forecast period from 2024 to 2030. This significant growth is driven by several factors, including the increasing demand for convenience foods, the rising number of working women, and the growing trend of home baking. The market is also influenced by the growing awareness of health and wellness, leading to the introduction of healthier flour blends, such as whole grain and gluten-free options. The increasing penetration of ready-made flour products in emerging markets is another factor contributing to the market's growth. As consumers continue to seek convenience and quality in their cooking and baking endeavors, the demand for ready-made flour products is expected to rise. The market's growth trajectory is further supported by the expanding distribution channels, including online retail, which makes these products more accessible to a broader audience. Overall, the global ready-made flour market is poised for significant growth in the coming years, driven by the increasing demand for convenience and quality in the culinary world.

| Report Metric | Details |

| Report Name | Ready-made Flour Market |

| Accounted market size in 2023 | US$ 27430 million |

| Forecasted market size in 2030 | US$ 45810 million |

| CAGR | 7.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | CSM Ingredients, Zeelandia, Nippon Flour Mills, Puratos, IREKS, Bakel, Nisshin Seifun, Orangerie, Griffith, Kerry, Prima Flour, Lam Soon, Yihai Kerry, PT Gandum Mas Kencana, AB Mauri, Showa Sangyo, AngelYeast, Pondan Pangan Makmur Indonesia |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |