What is Global Tee Block Valves Market?

The global Tee Block Valves market is a specialized segment within the broader industrial valves market. Tee block valves are essential components used in various industries to control the flow of liquids and gases. These valves are designed to handle high pressure and temperature conditions, making them suitable for demanding applications. They are typically used in pipelines to regulate the flow of fluids, ensuring that the system operates efficiently and safely. The market for these valves is driven by the increasing demand for energy, the need for efficient water management systems, and the growth of the chemical and petrochemical industries. As industries continue to expand and modernize, the demand for reliable and high-performance valves like tee block valves is expected to grow. The market is characterized by the presence of several key players who are continuously innovating to improve the performance and reliability of their products.

Manual, Pneumatic in the Global Tee Block Valves Market:

Manual and pneumatic tee block valves are two primary types of valves used in various industrial applications. Manual tee block valves are operated by hand, requiring physical effort to open or close the valve. These valves are simple in design and are often used in applications where automation is not necessary or where the valve does not need to be operated frequently. They are cost-effective and easy to maintain, making them a popular choice for many industries. On the other hand, pneumatic tee block valves are operated using compressed air. These valves are more complex and are used in applications where precise control of the flow is required. Pneumatic valves are often used in automated systems where the valve needs to be operated remotely or where frequent operation is necessary. They offer several advantages over manual valves, including faster operation, greater precision, and the ability to be integrated into automated control systems. However, they are also more expensive and require a source of compressed air to operate. The choice between manual and pneumatic tee block valves depends on several factors, including the specific requirements of the application, the available budget, and the level of automation desired. In many cases, industries may use a combination of both types of valves to achieve the desired level of control and efficiency. For example, manual valves may be used for less critical applications or as backup systems, while pneumatic valves are used for more critical applications where precise control is essential. The global market for these valves is driven by the need for efficient and reliable flow control solutions in various industries, including oil and gas, chemical, water treatment, and others. As industries continue to modernize and adopt more automated systems, the demand for pneumatic valves is expected to grow. However, manual valves will continue to play an important role in many applications due to their simplicity, reliability, and cost-effectiveness.

Oil & Gas, Chemical, Water Treatment, Other in the Global Tee Block Valves Market:

Tee block valves are widely used in various industries, including oil and gas, chemical, water treatment, and others. In the oil and gas industry, these valves are used to control the flow of crude oil, natural gas, and other hydrocarbons through pipelines. They are essential for ensuring the safe and efficient operation of the pipeline system, preventing leaks, and minimizing the risk of accidents. The high pressure and temperature conditions in the oil and gas industry require valves that are robust and reliable, making tee block valves an ideal choice. In the chemical industry, tee block valves are used to control the flow of various chemicals and solvents. These valves must be resistant to corrosion and able to handle aggressive chemicals, making them suitable for use in chemical processing plants. They help ensure the safe and efficient operation of the plant, preventing leaks and minimizing the risk of chemical spills. In the water treatment industry, tee block valves are used to control the flow of water through treatment plants. They are essential for ensuring the efficient operation of the treatment process, helping to regulate the flow of water and prevent contamination. These valves are also used in the distribution of treated water, ensuring that the water supply is safe and reliable. In addition to these industries, tee block valves are used in various other applications, including power generation, pharmaceuticals, and food and beverage processing. In power generation, these valves are used to control the flow of steam and other fluids through power plants, ensuring the efficient operation of the plant. In the pharmaceutical industry, they are used to control the flow of various liquids and gases through manufacturing processes, ensuring the quality and safety of the final product. In the food and beverage industry, tee block valves are used to control the flow of ingredients and finished products through processing and packaging lines, ensuring the quality and safety of the food and beverages. Overall, the versatility and reliability of tee block valves make them an essential component in various industries, helping to ensure the safe and efficient operation of various processes.

Global Tee Block Valves Market Outlook:

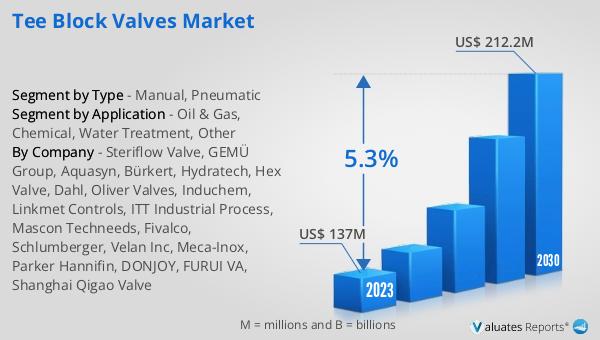

The global Tee Block Valves market was valued at US$ 137 million in 2023 and is anticipated to reach US$ 212.2 million by 2030, witnessing a CAGR of 5.3% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for efficient flow control solutions in various industries, including oil and gas, chemical, and water treatment. The market is characterized by the presence of several key players who are continuously innovating to improve the performance and reliability of their products. As industries continue to expand and modernize, the demand for reliable and high-performance valves like tee block valves is expected to grow. The market outlook for tee block valves is positive, with steady growth anticipated over the forecast period. This growth is supported by the increasing need for energy, the growth of the chemical and petrochemical industries, and the need for efficient water management systems. The market is also expected to benefit from advancements in valve technology, which are improving the performance and reliability of these valves. Overall, the global Tee Block Valves market is expected to experience steady growth over the forecast period, driven by the increasing demand for efficient and reliable flow control solutions in various industries.

| Report Metric | Details |

| Report Name | Tee Block Valves Market |

| Accounted market size in 2023 | US$ 137 million |

| Forecasted market size in 2030 | US$ 212.2 million |

| CAGR | 5.3% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Steriflow Valve, GEMÜ Group, Aquasyn, Bürkert, Hydratech, Hex Valve, Dahl, Oliver Valves, Induchem, Linkmet Controls, ITT Industrial Process, Mascon Techneeds, Fivalco, Schlumberger, Velan Inc, Meca-Inox, Parker Hannifin, DONJOY, FURUI VA, Shanghai Qigao Valve |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |