What is Global Gallic Acid (CAS 149-91-7) Market?

The Global Gallic Acid (CAS 149-91-7) Market refers to the worldwide trade and utilization of gallic acid, a naturally occurring organic compound found in various plants. Gallic acid is known for its antioxidant properties and is used in a variety of industries, including pharmaceuticals, food, and cosmetics. The market for gallic acid is driven by its diverse applications and the increasing demand for natural and organic products. It is used as a precursor for the synthesis of other chemicals, as well as in the production of inks, dyes, and photographic developers. The market is characterized by the presence of several key players who are involved in the production and distribution of gallic acid. The demand for gallic acid is expected to grow due to its wide range of applications and the increasing awareness of its benefits.

Industrial Grade, Pharmaceutical Grade, Food Grade in the Global Gallic Acid (CAS 149-91-7) Market:

Gallic acid is available in different grades, including industrial grade, pharmaceutical grade, and food grade, each catering to specific applications. Industrial grade gallic acid is primarily used in the manufacturing of inks, dyes, and photographic developers. It is also used as a precursor for the synthesis of other chemicals, such as pyrogallol and gallic acid esters. The industrial grade is characterized by its high purity and consistency, making it suitable for various industrial processes. Pharmaceutical grade gallic acid is used in the production of medicines and dietary supplements. It is known for its antioxidant properties and is used to treat various health conditions, including inflammation, diabetes, and cancer. The pharmaceutical grade is characterized by its high purity and compliance with regulatory standards, ensuring its safety and efficacy for medical use. Food grade gallic acid is used as a food additive and preservative. It is known for its ability to prevent the oxidation of fats and oils, thereby extending the shelf life of food products. The food grade is characterized by its high purity and compliance with food safety standards, ensuring its suitability for use in food products. The demand for gallic acid in different grades is driven by its diverse applications and the increasing awareness of its benefits. The market for gallic acid is expected to grow due to the increasing demand for natural and organic products, as well as the growing awareness of the health benefits of gallic acid.

Antioxidants, Biological Activity, Medical Applications, Other in the Global Gallic Acid (CAS 149-91-7) Market:

Gallic acid is used in various applications, including antioxidants, biological activity, medical applications, and other uses. As an antioxidant, gallic acid is known for its ability to neutralize free radicals and prevent oxidative damage to cells. This property makes it a valuable ingredient in the production of cosmetics and skincare products, where it helps to protect the skin from damage caused by environmental factors such as UV radiation and pollution. In terms of biological activity, gallic acid has been shown to exhibit antimicrobial, antiviral, and anti-inflammatory properties. These properties make it a valuable ingredient in the production of pharmaceuticals and dietary supplements, where it is used to treat various health conditions, including infections, inflammation, and chronic diseases. In medical applications, gallic acid is used in the production of medicines and dietary supplements. It is known for its ability to inhibit the growth of cancer cells and reduce the risk of chronic diseases such as diabetes and cardiovascular diseases. Gallic acid is also used in the production of diagnostic reagents and as a standard for the calibration of analytical instruments. Other uses of gallic acid include its use as a precursor for the synthesis of other chemicals, such as pyrogallol and gallic acid esters. It is also used in the production of inks, dyes, and photographic developers. The diverse applications of gallic acid and its wide range of benefits make it a valuable ingredient in various industries. The demand for gallic acid is expected to grow due to its wide range of applications and the increasing awareness of its benefits.

Global Gallic Acid (CAS 149-91-7) Market Outlook:

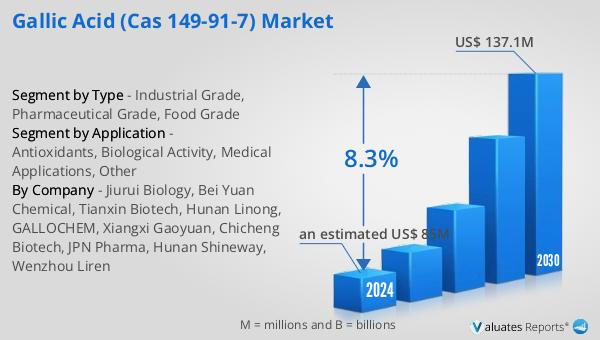

The global Gallic Acid (CAS 149-91-7) market is anticipated to grow significantly, with projections indicating it will reach US$ 137.1 million by 2030, up from an estimated US$ 85 million in 2024, reflecting a compound annual growth rate (CAGR) of 8.3% between 2024 and 2030. The market is dominated by the top three companies, which collectively hold over 60% of the market share. The Asia Pacific region is the largest market for gallic acid, accounting for approximately 45% of the global market share, followed by North America and Europe, which hold about 30% and 20% of the market share, respectively. In terms of product segmentation, industrial grade gallic acid is the largest segment, comprising over 65% of the market share. This significant market share is attributed to the extensive use of industrial grade gallic acid in various applications, including the manufacturing of inks, dyes, and photographic developers. The growing demand for natural and organic products, coupled with the increasing awareness of the health benefits of gallic acid, is expected to drive the growth of the global gallic acid market in the coming years.

| Report Metric | Details |

| Report Name | Gallic Acid (CAS 149-91-7) Market |

| Accounted market size in 2024 | an estimated US$ 85 in million |

| Forecasted market size in 2030 | US$ 137.1 million |

| CAGR | 8.3% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Jiurui Biology, Bei Yuan Chemical, Tianxin Biotech, Hunan Linong, GALLOCHEM, Xiangxi Gaoyuan, Chicheng Biotech, JPN Pharma, Hunan Shineway, Wenzhou Liren |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |