What is Global Dental Composite Opaquer Market?

The Global Dental Composite Opaquer Market refers to the worldwide industry focused on the production and distribution of dental composite opaquers. These are specialized materials used in dentistry to mask the underlying color of dental structures, ensuring a more natural and aesthetically pleasing appearance of dental restorations. Dental composite opaquers are essential in procedures such as fillings, crowns, and veneers, where they help in achieving a seamless blend with the natural teeth. The market encompasses various types of opaquers, including those in different forms and compositions, catering to the diverse needs of dental professionals. The demand for these products is driven by the increasing emphasis on dental aesthetics, advancements in dental materials, and the growing number of dental procedures worldwide. As dental health awareness rises and more people seek cosmetic dental treatments, the market for dental composite opaquers is expected to expand further.

Injection Type, Bottled Type, Other in the Global Dental Composite Opaquer Market:

In the Global Dental Composite Opaquer Market, products are categorized based on their form and application methods, including Injection Type, Bottled Type, and Other types. Injection Type opaquers are typically delivered using syringes, allowing for precise application and control. This type is favored for its ease of use and the ability to apply the material directly to the desired area without wastage. Dental professionals often prefer injection type opaquers for intricate procedures where precision is paramount. Bottled Type opaquers, on the other hand, come in liquid form and are dispensed from bottles. These are usually applied using brushes or other applicators. Bottled opaquers offer flexibility in terms of the amount used and are ideal for larger surface areas or when a more extensive application is required. They are also beneficial in situations where the dental professional needs to mix the opaquer with other materials to achieve a specific consistency or shade. The 'Other' category includes various forms of opaquers that do not fit into the injection or bottled types. This can include paste forms, pre-mixed capsules, or even powder forms that need to be mixed with a liquid before application. Each type has its own set of advantages and is chosen based on the specific needs of the dental procedure and the preference of the dental professional. The choice of opaquer type can significantly impact the efficiency and outcome of dental restorations. For instance, paste forms might be preferred for their thicker consistency and ease of manipulation, while pre-mixed capsules offer convenience and consistency in every application. The versatility in the types of dental composite opaquers available in the market ensures that dental professionals can select the most appropriate product for their specific needs, enhancing the quality and aesthetics of dental treatments.

Hospital, Clinic in the Global Dental Composite Opaquer Market:

The usage of Global Dental Composite Opaquer Market products is prevalent in both hospitals and clinics, each setting having its unique requirements and applications. In hospitals, dental composite opaquers are used extensively in the dental departments for a variety of restorative procedures. Hospitals often handle complex dental cases that require advanced materials and techniques. The availability of high-quality opaquers in hospitals ensures that patients receive the best possible care, especially in cases involving significant dental damage or cosmetic restoration. The use of opaquers in hospitals is also crucial for procedures that require a high degree of precision and customization, such as in the creation of dental prosthetics and implants. In clinics, the use of dental composite opaquers is equally important but often focuses more on routine dental care and cosmetic enhancements. Clinics cater to a wide range of patients seeking treatments for dental issues ranging from cavities to aesthetic improvements. The use of opaquers in clinics helps in achieving natural-looking results, which is a significant factor for patient satisfaction. Clinics often perform procedures like fillings, crowns, and veneers, where the ability to mask the underlying tooth color is essential for a seamless finish. The accessibility of various types of opaquers in clinics allows dental professionals to provide tailored treatments that meet the specific needs and preferences of their patients. Both hospitals and clinics benefit from the advancements in dental composite opaquer technology, which has led to products that offer better adhesion, durability, and aesthetic outcomes. The continuous improvement in these materials ensures that dental professionals can deliver high-quality care, whether in a hospital setting dealing with complex cases or in a clinic focusing on routine and cosmetic dental procedures.

Global Dental Composite Opaquer Market Outlook:

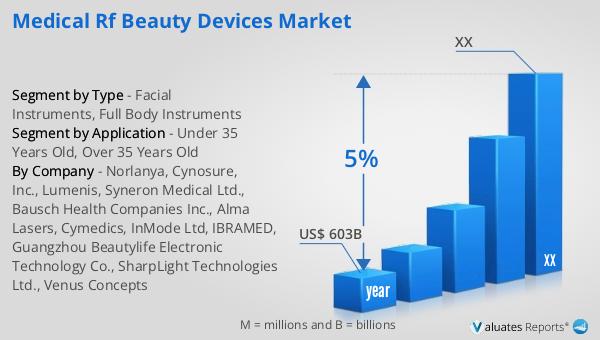

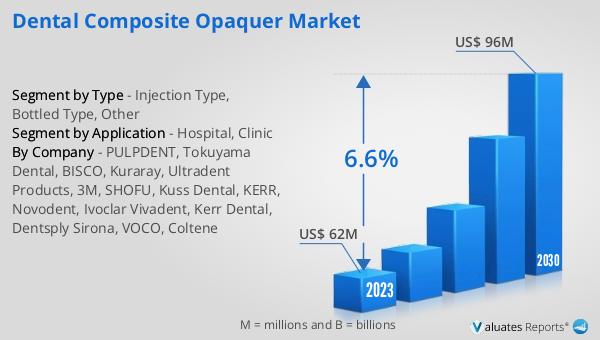

The global Dental Composite Opaquer market was valued at US$ 62 million in 2023 and is anticipated to reach US$ 96 million by 2030, witnessing a CAGR of 6.6% during the forecast period from 2024 to 2030. According to our research, the global market for medical devices is estimated at US$ 603 billion in the year 2023 and will be growing at a CAGR of 5% over the next six years. This growth in the dental composite opaquer market reflects the increasing demand for advanced dental materials and the rising awareness of dental aesthetics. The market's expansion is driven by technological advancements, the growing number of dental procedures, and the increasing focus on cosmetic dentistry. As more people seek to improve their dental appearance and health, the demand for high-quality dental composite opaquers is expected to rise, contributing to the overall growth of the medical devices market.

| Report Metric | Details |

| Report Name | Dental Composite Opaquer Market |

| Accounted market size in 2023 | US$ 62 million |

| Forecasted market size in 2030 | US$ 96 million |

| CAGR | 6.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | PULPDENT, Tokuyama Dental, BISCO, Kuraray, Ultradent Products, 3M, SHOFU, Kuss Dental, KERR, Novodent, Ivoclar Vivadent, Kerr Dental, Dentsply Sirona, VOCO, Coltene |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |