What is Global Vehicle LCD Screen Market?

The Global Vehicle LCD Screen Market refers to the worldwide industry focused on the production, distribution, and sale of liquid crystal display (LCD) screens specifically designed for vehicles. These screens are used in various applications within vehicles, such as infotainment systems, navigation systems, instrument clusters, and rear-seat entertainment systems. The market encompasses a wide range of screen sizes and types, catering to different vehicle models and consumer preferences. The increasing demand for advanced in-car entertainment and information systems, coupled with the growing trend of connected vehicles, is driving the growth of this market. Additionally, technological advancements in display technologies, such as higher resolution, better color accuracy, and improved durability, are further propelling the adoption of LCD screens in vehicles. The market is highly competitive, with numerous players striving to innovate and offer superior products to gain a competitive edge. The global vehicle LCD screen market is poised for significant growth in the coming years, driven by the continuous evolution of automotive technologies and the rising consumer demand for enhanced in-car experiences.

2.5-4 Inch, 5 Inch, 7 Inch, 8-10 Inch, 11-15 Inch, 16-42 Inch, Others in the Global Vehicle LCD Screen Market:

The Global Vehicle LCD Screen Market is segmented based on screen sizes, ranging from small to large displays, each serving different purposes and vehicle types. The 2.5-4 inch screens are typically used in compact cars and entry-level vehicles, primarily for basic functions like displaying time, temperature, and simple navigation instructions. These screens are cost-effective and provide essential information without overwhelming the driver. The 5-inch screens are a step up, often found in mid-range vehicles, offering more detailed navigation, multimedia controls, and basic infotainment features. They strike a balance between functionality and affordability, making them popular among budget-conscious consumers. The 7-inch screens are commonly used in higher-end vehicles and offer a more immersive experience with advanced navigation, multimedia playback, and connectivity features. These screens are large enough to display detailed maps and multimedia content without being too obtrusive. The 8-10 inch screens are typically found in luxury vehicles and high-end SUVs, providing a premium experience with high-resolution displays, advanced infotainment systems, and seamless connectivity options. These screens often support touch functionality and can be integrated with voice control systems for a more intuitive user experience. The 11-15 inch screens are used in premium and luxury vehicles, offering a cinematic experience with ultra-high resolution, advanced graphics, and extensive connectivity options. These screens are designed to provide a seamless and immersive experience, often supporting split-screen functionality to display multiple types of information simultaneously. The 16-42 inch screens are primarily used in commercial vehicles, buses, and recreational vehicles, providing entertainment and information to passengers. These large screens are ideal for displaying movies, TV shows, and other multimedia content, making long journeys more enjoyable for passengers. Other screen sizes and types cater to specific needs and applications, such as heads-up displays (HUDs) that project information onto the windshield, providing critical information without distracting the driver. Each screen size and type serves a unique purpose, catering to different vehicle types, consumer preferences, and market segments. The continuous advancements in display technologies, such as OLED and QLED, are further enhancing the capabilities and applications of vehicle LCD screens, driving the growth of this market.

Corporate, Retail in the Global Vehicle LCD Screen Market:

The usage of Global Vehicle LCD Screen Market in corporate and retail sectors highlights the versatility and wide-ranging applications of these screens. In the corporate sector, vehicle LCD screens are increasingly being used in company fleets, executive cars, and corporate shuttles. These screens provide essential information such as navigation, real-time traffic updates, and vehicle diagnostics, enhancing the efficiency and productivity of corporate travel. For executive cars, high-end LCD screens offer a premium experience with advanced infotainment systems, seamless connectivity, and personalized settings, catering to the needs of busy executives who require constant access to information and entertainment on the go. In corporate shuttles, larger screens provide entertainment and information to passengers, making the commute more enjoyable and productive. The retail sector also benefits significantly from vehicle LCD screens, particularly in the automotive sales and service industry. Car dealerships use these screens to showcase vehicle features, specifications, and promotional videos, providing potential buyers with a detailed and interactive experience. In service centers, LCD screens display real-time service updates, estimated wait times, and promotional offers, enhancing the customer experience and streamlining operations. Additionally, ride-sharing services and taxis are increasingly incorporating LCD screens to provide passengers with navigation information, entertainment options, and advertisements, creating new revenue streams and improving the overall ride experience. The versatility of vehicle LCD screens allows them to be customized and integrated into various applications, catering to the specific needs of corporate and retail sectors. The continuous advancements in display technologies, such as touch functionality, voice control, and high-resolution displays, are further expanding the applications and benefits of vehicle LCD screens in these sectors.

Global Vehicle LCD Screen Market Outlook:

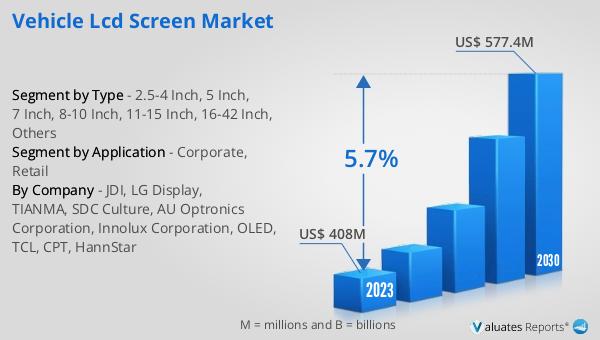

The global Vehicle LCD Screen market, valued at US$ 408 million in 2023, is projected to grow significantly, reaching an estimated US$ 577.4 million by 2030. This growth trajectory represents a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2024 to 2030. The market's expansion is driven by the increasing demand for advanced in-car entertainment and information systems, coupled with the growing trend of connected vehicles. Technological advancements in display technologies, such as higher resolution, better color accuracy, and improved durability, are also contributing to the market's growth. The competitive landscape of the market is characterized by numerous players striving to innovate and offer superior products to gain a competitive edge. The continuous evolution of automotive technologies and the rising consumer demand for enhanced in-car experiences are expected to further propel the growth of the global vehicle LCD screen market in the coming years.

| Report Metric | Details |

| Report Name | Vehicle LCD Screen Market |

| Accounted market size in 2023 | US$ 408 million |

| Forecasted market size in 2030 | US$ 577.4 million |

| CAGR | 5.7% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | JDI, LG Display, TIANMA, SDC Culture, AU Optronics Corporation, Innolux Corporation, OLED, TCL, CPT, HannStar |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |