What is Global High Purity Lidocaine Market?

The Global High Purity Lidocaine Market refers to the worldwide demand and supply of lidocaine that meets high purity standards, typically used in medical and pharmaceutical applications. Lidocaine is a local anesthetic and antiarrhythmic drug that is essential in various medical procedures to numb tissue in a specific area. The high purity lidocaine market is driven by the increasing need for effective pain management solutions and the growing prevalence of chronic diseases that require surgical interventions. High purity lidocaine is preferred because it ensures better efficacy and safety in medical applications, reducing the risk of side effects and complications. The market encompasses various forms of lidocaine, including injections, topical solutions, and patches, catering to different medical needs. The demand for high purity lidocaine is also influenced by advancements in medical technology and the rising number of outpatient surgeries. As healthcare systems across the globe continue to evolve, the need for high-quality anesthetics like lidocaine is expected to grow, making the global high purity lidocaine market a critical component of the healthcare industry.

Purity > 99%, Purity 95% - 99% in the Global High Purity Lidocaine Market:

In the Global High Purity Lidocaine Market, products are often categorized based on their purity levels, such as Purity > 99% and Purity 95% - 99%. Lidocaine with a purity greater than 99% is considered the highest quality and is typically used in applications where maximum efficacy and minimal side effects are crucial. This level of purity ensures that the lidocaine is free from impurities that could potentially cause adverse reactions or reduce the effectiveness of the drug. High purity lidocaine is often used in sensitive medical procedures, including spinal anesthesia, epidural anesthesia, and in the preparation of intravenous regional anesthesia. It is also preferred in the formulation of topical anesthetics used in dermatological procedures and minor surgeries. On the other hand, lidocaine with a purity range of 95% - 99% is still considered high quality but may contain slightly more impurities compared to the > 99% purity grade. This grade of lidocaine is commonly used in less critical applications where the presence of minimal impurities does not significantly impact the drug's performance. For instance, it may be used in dental procedures, minor surgical interventions, and in the formulation of over-the-counter topical pain relief products. The choice between these two purity levels depends on the specific medical requirements and the potential risks associated with impurities. Both grades play a vital role in the healthcare industry, ensuring that patients receive effective and safe pain management solutions. The production of high purity lidocaine involves stringent quality control measures to ensure that the final product meets the required standards. Manufacturers invest in advanced purification technologies and rigorous testing protocols to achieve the desired purity levels. The demand for high purity lidocaine is also driven by regulatory requirements that mandate the use of high-quality anesthetics in medical procedures. As a result, the market for high purity lidocaine continues to grow, with increasing applications in various medical fields. The availability of different purity grades allows healthcare providers to choose the most appropriate product for their specific needs, ensuring optimal patient outcomes.

Hospital, Clinics in the Global High Purity Lidocaine Market:

The usage of high purity lidocaine in hospitals and clinics is extensive and varied, reflecting its importance in modern medical practice. In hospitals, high purity lidocaine is primarily used in surgical procedures to provide local anesthesia. This includes major surgeries where lidocaine is used as an adjunct to general anesthesia to manage pain and reduce the need for higher doses of systemic anesthetics. High purity lidocaine is also used in emergency departments for procedures such as suturing wounds, where quick and effective pain relief is essential. In addition, it is used in the management of acute pain conditions, such as those resulting from trauma or severe burns. The high purity of the lidocaine ensures that it acts quickly and effectively, minimizing the risk of complications and side effects. In clinics, high purity lidocaine is commonly used in minor surgical procedures and diagnostic tests. For example, it is used in dermatological clinics for procedures such as mole removal, biopsies, and laser treatments. The high purity of the lidocaine ensures that patients experience minimal discomfort during these procedures, enhancing the overall patient experience. In dental clinics, high purity lidocaine is used for procedures such as tooth extractions, root canals, and cavity fillings. The rapid onset of action and prolonged duration of effect make high purity lidocaine an ideal choice for dental anesthesia. Additionally, high purity lidocaine is used in pain management clinics for the treatment of chronic pain conditions. This includes conditions such as neuropathic pain, where lidocaine patches or injections are used to provide long-lasting pain relief. The high purity of the lidocaine ensures that it is well-tolerated by patients, reducing the risk of adverse reactions. Overall, the use of high purity lidocaine in hospitals and clinics is essential for providing effective and safe pain management solutions. The availability of high purity lidocaine in various forms, such as injections, topical solutions, and patches, allows healthcare providers to choose the most appropriate product for their specific needs. This ensures that patients receive the best possible care, with minimal discomfort and maximum efficacy.

Global High Purity Lidocaine Market Outlook:

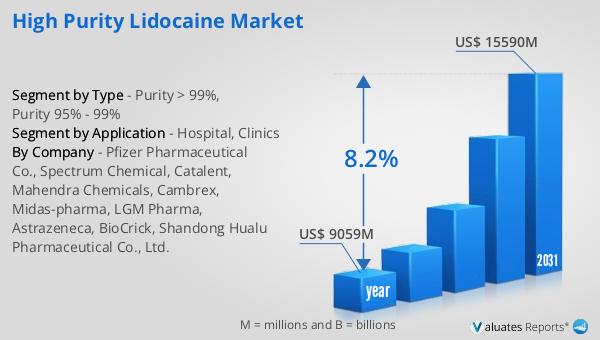

The global High Purity Lidocaine market was valued at US$ 8149 million in 2023 and is anticipated to reach US$ 13520 million by 2030, witnessing a CAGR of 8.2% during the forecast period 2024-2030. This significant growth reflects the increasing demand for high-quality anesthetics in medical and pharmaceutical applications. The market's expansion is driven by factors such as the rising prevalence of chronic diseases, advancements in medical technology, and the growing number of surgical procedures worldwide. High purity lidocaine is preferred for its superior efficacy and safety profile, making it a critical component in various medical treatments. The market's growth trajectory indicates a strong future for high purity lidocaine, with continued innovation and development expected to further enhance its applications and benefits.

| Report Metric | Details |

| Report Name | High Purity Lidocaine Market |

| Accounted market size in 2023 | US$ 8149 million |

| Forecasted market size in 2030 | US$ 13520 million |

| CAGR | 8.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Pfizer Pharmaceutical Co., Spectrum Chemical, Catalent, Mahendra Chemicals, Cambrex, Midas-pharma, LGM Pharma, Astrazeneca, BioCrick, Shandong Hualu Pharmaceutical Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |