What is Global Biological Data Visualization Market?

The Global Biological Data Visualization Market is a rapidly evolving sector that focuses on the graphical representation of biological data. This market encompasses a wide range of tools and software designed to help scientists, researchers, and healthcare professionals interpret complex biological information. The primary goal is to transform raw data into visual formats that are easier to understand and analyze. This includes everything from simple charts and graphs to more sophisticated 3D models and interactive platforms. The market is driven by the increasing volume of biological data generated from various sources such as genomics, proteomics, and metabolomics. As the complexity and volume of data grow, so does the need for advanced visualization tools that can provide meaningful insights. These tools are essential for various applications, including drug discovery, disease research, and personalized medicine. The market is also influenced by technological advancements in data analytics and machine learning, which are making it easier to handle and interpret large datasets. Overall, the Global Biological Data Visualization Market plays a crucial role in advancing our understanding of biological processes and improving healthcare outcomes.

Microscopy, Magnetic Resonance Imaging, Sequencing, X-ray Crystallography, Others in the Global Biological Data Visualization Market:

Microscopy, Magnetic Resonance Imaging (MRI), Sequencing, X-ray Crystallography, and other techniques are integral components of the Global Biological Data Visualization Market. Microscopy involves the use of microscopes to view small-scale structures that are not visible to the naked eye. This technique is essential for studying cellular structures, tissues, and microorganisms. Advanced forms of microscopy, such as confocal and electron microscopy, provide high-resolution images that are crucial for detailed analysis. Magnetic Resonance Imaging (MRI) is a non-invasive imaging technique that uses magnetic fields and radio waves to create detailed images of the body's internal structures. It is widely used in medical diagnostics to visualize organs, tissues, and even metabolic processes. Sequencing, particularly DNA sequencing, involves determining the precise order of nucleotides within a DNA molecule. This technique is fundamental for genomics research, enabling scientists to identify genetic variations and understand their implications for health and disease. X-ray Crystallography is a technique used to determine the atomic and molecular structure of a crystal. By measuring the angles and intensities of X-ray beams diffracted by the crystal, researchers can create a 3D model of the molecular structure. This is particularly useful in drug design and understanding protein functions. Other techniques in the market include flow cytometry, which analyzes the physical and chemical characteristics of particles in a fluid, and mass spectrometry, which identifies the composition of a sample by measuring the mass-to-charge ratio of its ions. Each of these techniques generates vast amounts of data that require sophisticated visualization tools to interpret. These tools help in converting complex datasets into visual formats that are easier to understand, thereby facilitating better decision-making in research and clinical settings. The integration of these techniques with advanced data visualization tools is driving innovation in the field, enabling more accurate and comprehensive analysis of biological data.

Academic Research, Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Other Users in the Global Biological Data Visualization Market:

The usage of the Global Biological Data Visualization Market spans various sectors, including academic research, hospitals and clinics, pharmaceutical and biotechnology companies, and other users. In academic research, these visualization tools are indispensable for interpreting complex biological data generated from experiments and studies. Researchers use these tools to create visual representations of their data, making it easier to identify patterns, trends, and anomalies. This not only aids in hypothesis testing and validation but also enhances the communication of findings through publications and presentations. In hospitals and clinics, biological data visualization tools are used to improve patient care and outcomes. For instance, MRI and other imaging techniques generate detailed visual data that help clinicians diagnose and monitor diseases. Visualization tools enable the integration of various data types, such as genetic information and imaging results, providing a comprehensive view of a patient's health. This holistic approach facilitates personalized treatment plans and more accurate prognoses. Pharmaceutical and biotechnology companies leverage these tools in drug discovery and development. Visualization of biological data helps in understanding the mechanisms of action of potential drug candidates, identifying biomarkers, and predicting drug responses. This accelerates the drug development process and increases the likelihood of successful outcomes. Additionally, these tools are used in quality control and regulatory compliance, ensuring that products meet the required standards. Other users of biological data visualization tools include government agencies, non-profit organizations, and private research institutions. These entities use visualization tools for various purposes, such as public health monitoring, environmental research, and policy-making. For example, government agencies may use these tools to visualize epidemiological data, helping to track disease outbreaks and plan interventions. Non-profit organizations might use them to analyze data from conservation projects, aiding in the protection of endangered species. Overall, the Global Biological Data Visualization Market is a vital resource across multiple sectors, enhancing the ability to interpret complex biological data and make informed decisions.

Global Biological Data Visualization Market Outlook:

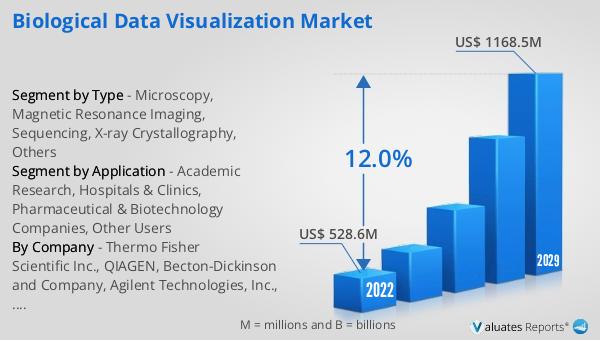

The global Biological Data Visualization market was valued at US$ 528.6 million in 2023 and is anticipated to reach US$ 1168.5 million by 2030, witnessing a CAGR of 12.0% during the forecast period 2024-2030. This significant growth reflects the increasing demand for advanced visualization tools to handle the ever-growing volume of biological data. As the field of biological research continues to expand, the need for sophisticated tools that can transform complex datasets into understandable visual formats becomes more critical. These tools are not only essential for researchers and clinicians but also for pharmaceutical companies and other stakeholders who rely on accurate data interpretation for decision-making. The projected growth in the market underscores the importance of continuous innovation and development in data visualization technologies. With advancements in areas such as machine learning and artificial intelligence, the capabilities of these tools are expected to improve, offering even more precise and comprehensive insights. This growth trajectory highlights the vital role that biological data visualization plays in advancing scientific research, improving healthcare outcomes, and driving innovation in the pharmaceutical and biotechnology industries.

| Report Metric | Details |

| Report Name | Biological Data Visualization Market |

| Accounted market size in 2023 | US$ 528.6 million |

| Forecasted market size in 2030 | US$ 1168.5 million |

| CAGR | 12.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Thermo Fisher Scientific Inc., QIAGEN, Becton-Dickinson and Company, Agilent Technologies, Inc., 3M, Carl Zeiss AG, Oxford Instruments, Olympus Corporation, GE Healthcare, Clarivate Analytics, arivis AG, Scientific Volume Imaging B.V., Media Cybernetics, Inc., Molecular Devices, LLC, Danaher |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |