What is Zinc Sulfide Raw Material - Global Market?

Zinc sulfide is a versatile raw material that plays a significant role in various industries worldwide. It is a chemical compound with the formula ZnS and is primarily used in the production of phosphors, pigments, and optical materials. The global market for zinc sulfide raw material is driven by its extensive applications in different sectors, including electronics, optics, and coatings. This compound is known for its excellent luminescent properties, making it a popular choice in the manufacturing of display screens, X-ray screens, and other optical devices. Additionally, zinc sulfide is used as a pigment in paints and plastics due to its ability to provide a bright white color. The demand for zinc sulfide is also fueled by its use in the semiconductor industry, where it serves as a crucial component in the production of various electronic devices. As industries continue to innovate and expand, the global market for zinc sulfide raw material is expected to grow, driven by its diverse applications and the increasing demand for advanced materials.

in the Zinc Sulfide Raw Material - Global Market:

Zinc sulfide raw material is utilized in various forms to cater to the diverse needs of different customers across the global market. One of the primary forms of zinc sulfide is its use as a phosphor material. Phosphors are substances that exhibit the phenomenon of luminescence, and zinc sulfide is widely used in this capacity due to its ability to emit light when exposed to ultraviolet or electron beam excitation. This property makes it an essential component in the production of cathode ray tubes, electroluminescent panels, and other display technologies. Another significant form of zinc sulfide is its use as a pigment. In this application, zinc sulfide is valued for its bright white color and is often used in combination with other pigments to enhance the opacity and brightness of paints, coatings, and plastics. This makes it a popular choice in the automotive, construction, and consumer goods industries, where high-quality finishes are required. Additionally, zinc sulfide is used in the production of optical materials. Its high refractive index and transparency in the infrared spectrum make it suitable for use in lenses, windows, and other optical components. This is particularly important in the defense and aerospace industries, where advanced optical systems are required for targeting, surveillance, and navigation. Furthermore, zinc sulfide is used in the semiconductor industry, where it serves as a crucial material in the fabrication of electronic devices. Its properties as a wide bandgap semiconductor make it suitable for use in light-emitting diodes (LEDs), laser diodes, and other optoelectronic devices. The versatility of zinc sulfide raw material and its ability to meet the specific needs of various industries make it a valuable commodity in the global market. As technology continues to advance and new applications for zinc sulfide are discovered, its demand is expected to grow, further solidifying its position as a key material in multiple sectors.

Semiconductor, Optical Applications, Others in the Zinc Sulfide Raw Material - Global Market:

Zinc sulfide raw material finds extensive usage in several key areas, including semiconductors, optical applications, and other industries. In the semiconductor sector, zinc sulfide is valued for its properties as a wide bandgap semiconductor. This makes it an ideal material for the production of light-emitting diodes (LEDs), laser diodes, and other optoelectronic devices. The ability of zinc sulfide to efficiently emit light when subjected to electrical excitation is crucial in the development of energy-efficient lighting solutions and advanced display technologies. Its role in the semiconductor industry is further enhanced by its compatibility with other semiconductor materials, allowing for the creation of complex electronic devices with improved performance and reliability. In optical applications, zinc sulfide is prized for its high refractive index and excellent transparency in the infrared spectrum. These properties make it an essential material in the production of lenses, windows, and other optical components used in a variety of industries. In the defense and aerospace sectors, zinc sulfide is used in the manufacturing of advanced optical systems for targeting, surveillance, and navigation. Its ability to withstand harsh environmental conditions and provide clear, high-quality images is critical in these applications. Additionally, zinc sulfide is used in the production of infrared optics for thermal imaging cameras, which are widely used in security, firefighting, and industrial inspection. Beyond semiconductors and optical applications, zinc sulfide is also utilized in other industries due to its unique properties. In the coatings industry, it is used as a pigment to provide a bright white color and enhance the opacity of paints and coatings. This makes it a popular choice in the automotive and construction industries, where high-quality finishes are required. Furthermore, zinc sulfide is used in the production of phosphors for cathode ray tubes, electroluminescent panels, and other display technologies. Its ability to emit light when exposed to ultraviolet or electron beam excitation makes it an essential component in these applications. The diverse range of uses for zinc sulfide raw material highlights its importance in the global market and underscores the need for continued research and development to explore new applications and improve existing technologies.

Zinc Sulfide Raw Material - Global Market Outlook:

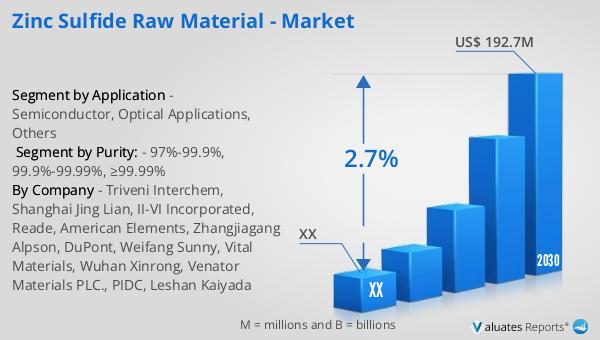

The global market for zinc sulfide raw material was valued at approximately $159 million in 2023. It is projected to grow to a revised size of around $192.7 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.7% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for zinc sulfide across various industries, driven by its versatile applications and unique properties. In North America, the market for zinc sulfide raw material was valued at a certain amount in 2023 and is expected to reach a specific value by 2030, with a CAGR of a certain percentage during the forecast period. The growth in the North American market is likely to be influenced by the region's strong industrial base and the presence of key players in the electronics, optics, and coatings industries. The steady growth of the zinc sulfide market globally and in North America highlights the material's significance in various sectors and the ongoing demand for advanced materials that can meet the evolving needs of modern industries. As the market continues to expand, companies involved in the production and distribution of zinc sulfide raw material are expected to benefit from the increasing opportunities and the growing emphasis on innovation and sustainability.

| Report Metric | Details |

| Report Name | Zinc Sulfide Raw Material - Market |

| Forecasted market size in 2030 | US$ 192.7 million |

| CAGR | 2.7% |

| Forecasted years | 2024 - 2030 |

| Segment by Purity: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Triveni Interchem, Shanghai Jing Lian, II-VI Incorporated, Reade, American Elements, Zhangjiagang Alpson, DuPont, Weifang Sunny, Vital Materials, Wuhan Xinrong, Venator Materials PLC., PIDC, Leshan Kaiyada |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |