What is Global Epinephrine Market?

The global epinephrine market is a crucial segment of the pharmaceutical industry, focusing on the production and distribution of epinephrine, a vital medication used primarily for emergency treatment of severe allergic reactions, known as anaphylaxis. Epinephrine, also known as adrenaline, is a hormone and a neurotransmitter that plays a significant role in the body's fight-or-flight response. It is used medically to treat conditions such as anaphylaxis, cardiac arrest, and severe asthma attacks. The market for epinephrine is driven by the increasing prevalence of allergies and the rising awareness about the importance of timely treatment for allergic reactions. Additionally, the growing demand for self-administered epinephrine devices, such as auto-injectors, has significantly contributed to the market's expansion. The market is characterized by a few key players who dominate the production and distribution channels, ensuring the availability of epinephrine products across various regions. With advancements in medical technology and increasing healthcare expenditure, the global epinephrine market is poised for continued growth, addressing the critical need for effective emergency treatment options. The market's dynamics are influenced by regulatory policies, pricing strategies, and the development of innovative delivery systems that enhance patient convenience and compliance.

Epinephrine Auto-injector, Epinephrine Prefilled Syringe, Combination Epinephrine Products in the Global Epinephrine Market:

Epinephrine auto-injectors are one of the most well-known and widely used products in the global epinephrine market. These devices are designed for ease of use, allowing individuals, even those without medical training, to administer a precise dose of epinephrine quickly during an emergency. The auto-injector is a compact, portable device that contains a pre-measured dose of epinephrine, which is delivered through a needle that automatically injects the medication when the device is pressed against the skin. This feature is particularly crucial for individuals at risk of anaphylaxis, as it allows for rapid intervention, which can be life-saving. The convenience and reliability of auto-injectors have made them the largest segment in the epinephrine market, accounting for a significant share of the market revenue. On the other hand, epinephrine prefilled syringes are another important product in the market. These syringes come preloaded with a specific dose of epinephrine and are typically used in clinical settings by healthcare professionals. Prefilled syringes offer the advantage of reducing preparation time during emergencies, ensuring that patients receive the medication promptly. They are also used in situations where precise dosing is critical, such as in pediatric cases or when treating individuals with specific medical conditions. Combination epinephrine products represent a newer development in the market, aiming to enhance the efficacy and convenience of epinephrine administration. These products often combine epinephrine with other medications or delivery systems to address multiple aspects of an allergic reaction or to improve the stability and shelf-life of the medication. For instance, some combination products may include antihistamines or corticosteroids alongside epinephrine to provide a more comprehensive treatment for anaphylaxis. Others may incorporate advanced delivery technologies, such as needle-free injectors or inhalation devices, to improve patient compliance and comfort. The development of combination epinephrine products reflects the ongoing innovation in the market, driven by the need to improve patient outcomes and address the limitations of existing treatment options. Overall, the global epinephrine market is characterized by a diverse range of products, each designed to meet specific needs and preferences of patients and healthcare providers. The continued growth and diversification of this market are fueled by advancements in medical technology, increasing awareness of allergic conditions, and the rising demand for effective and convenient treatment options.

Anaphylaxis, Cardiac Arrest, Others in the Global Epinephrine Market:

The global epinephrine market plays a crucial role in the management of anaphylaxis, a severe and potentially life-threatening allergic reaction. Anaphylaxis can occur within minutes of exposure to an allergen, such as food, insect stings, or medications, and requires immediate medical intervention. Epinephrine is the first-line treatment for anaphylaxis, as it works rapidly to reverse the symptoms by constricting blood vessels, relaxing muscles in the airways, and reducing swelling. The availability of epinephrine auto-injectors has significantly improved the management of anaphylaxis, allowing individuals at risk to carry the medication with them and administer it quickly in case of an emergency. In addition to anaphylaxis, epinephrine is also used in the treatment of cardiac arrest, a condition where the heart suddenly stops beating. In such cases, epinephrine is administered to stimulate the heart and restore circulation. It is typically used in conjunction with cardiopulmonary resuscitation (CPR) and other advanced life support measures to improve the chances of survival. The use of epinephrine in cardiac arrest is well-established, and it remains a critical component of emergency medical protocols worldwide. Beyond anaphylaxis and cardiac arrest, epinephrine is also used in other medical situations, such as severe asthma attacks and certain types of shock. In asthma, epinephrine can help to quickly open the airways and improve breathing, providing relief to individuals experiencing severe respiratory distress. In cases of shock, epinephrine can help to stabilize blood pressure and improve circulation, supporting the body's vital functions. The versatility of epinephrine in treating a range of emergency conditions underscores its importance in the global healthcare landscape. The continued demand for epinephrine products is driven by the increasing prevalence of allergic conditions, the aging population, and the rising incidence of chronic diseases that may lead to complications requiring emergency intervention. As such, the global epinephrine market is expected to continue growing, with ongoing research and development efforts focused on improving the efficacy, safety, and accessibility of epinephrine products.

Global Epinephrine Market Outlook:

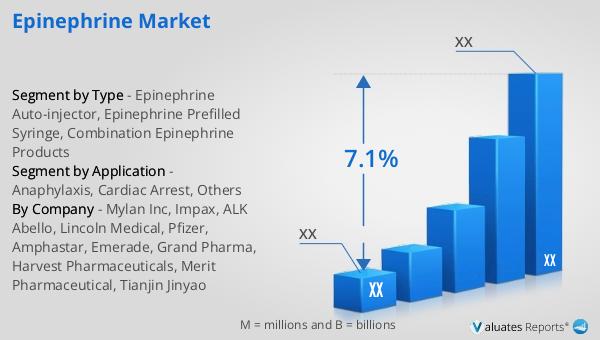

In 2024, the global epinephrine market was valued at approximately $3.48 billion, with projections indicating a rise to around $5.587 billion by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 7.1% from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold about 60% of the market share. The United States represents the largest market, accounting for roughly 40% of the global share, followed by Europe, which holds about 35%. Among the various products available, the epinephrine auto-injector stands out as the largest segment, capturing approximately 60% of the market. This dominance is attributed to the widespread adoption of auto-injectors due to their ease of use and effectiveness in emergency situations. The significant market share held by the United States can be attributed to the high prevalence of allergic conditions and the well-established healthcare infrastructure that supports the distribution and use of epinephrine products. Similarly, Europe's substantial market share reflects the region's focus on healthcare innovation and the increasing awareness of allergic conditions among the population. The projected growth of the global epinephrine market highlights the ongoing demand for effective emergency treatment options and the importance of continued investment in research and development to enhance the availability and accessibility of epinephrine products worldwide.

| Report Metric | Details |

| Report Name | Epinephrine Market |

| CAGR | 7.1% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Mylan Inc, Impax, ALK Abello, Lincoln Medical, Pfizer, Amphastar, Emerade, Grand Pharma, Harvest Pharmaceuticals, Merit Pharmaceutical, Tianjin Jinyao |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |