What is Global Memory Module Connectors Market?

The Global Memory Module Connectors Market is a crucial segment within the broader electronics and semiconductor industry. Memory module connectors are essential components that facilitate the connection between memory modules and the motherboard in various electronic devices. These connectors ensure efficient data transfer and communication between the memory and the processor, which is vital for the optimal performance of devices. The market for these connectors is driven by the increasing demand for high-performance computing devices, advancements in technology, and the growing need for faster data processing capabilities. As electronic devices become more sophisticated, the demand for reliable and efficient memory module connectors continues to rise. This market encompasses a wide range of products, including connectors for desktop PCs, notebook PCs, gaming machines, hard disk drives, solid-state drives, and networking servers. The evolution of technology and the increasing complexity of electronic devices are expected to further drive the growth of the Global Memory Module Connectors Market in the coming years. Manufacturers in this market are continually innovating to develop connectors that meet the evolving needs of the industry, focusing on aspects such as speed, reliability, and compatibility with various devices.

Standard Interface, Micro Interface in the Global Memory Module Connectors Market:

In the Global Memory Module Connectors Market, two primary types of interfaces are prevalent: the Standard Interface and the Micro Interface. The Standard Interface is commonly used in larger devices such as desktop PCs and servers. It is designed to handle higher data transfer rates and larger volumes of data, making it suitable for applications that require robust performance and reliability. These connectors are typically larger in size and are engineered to support the high power and thermal requirements of powerful computing systems. On the other hand, the Micro Interface is tailored for smaller, more compact devices like notebook PCs and portable gaming machines. These connectors are designed to be space-efficient while still providing adequate data transfer capabilities. The Micro Interface is crucial for devices where space is at a premium, and power consumption needs to be minimized. Both interfaces play a significant role in the functionality and performance of electronic devices. The choice between a Standard Interface and a Micro Interface depends on the specific requirements of the device, including size constraints, power consumption, and data transfer needs. As technology continues to advance, the demand for both types of interfaces is expected to grow, driven by the increasing complexity and performance demands of modern electronic devices. Manufacturers in the Global Memory Module Connectors Market are continually innovating to improve the performance and efficiency of these interfaces, ensuring they meet the evolving needs of the industry. This includes developing connectors that can support higher data transfer rates, are more energy-efficient, and are compatible with a wider range of devices. The ongoing advancements in technology and the increasing demand for high-performance computing devices are expected to drive the growth of both the Standard Interface and Micro Interface segments in the coming years. As electronic devices become more sophisticated, the need for reliable and efficient memory module connectors will continue to rise, further fueling the growth of the Global Memory Module Connectors Market.

Desktop PCs and Notebook PC, Gaming Machines, Hard Disk Drive and Solid State Drives, Networking Servers, Others in the Global Memory Module Connectors Market:

The Global Memory Module Connectors Market finds extensive usage across various applications, including desktop PCs, notebook PCs, gaming machines, hard disk drives, solid-state drives, networking servers, and others. In desktop PCs and notebook PCs, memory module connectors are critical for ensuring efficient data transfer between the memory and the processor. These connectors play a vital role in the overall performance of the device, as they facilitate the smooth operation of applications and processes. In gaming machines, memory module connectors are essential for delivering the high-speed data transfer required for seamless gaming experiences. These connectors ensure that the gaming machine can handle the complex graphics and fast-paced action of modern games. In hard disk drives and solid-state drives, memory module connectors are used to connect the storage device to the motherboard, enabling efficient data transfer and storage. These connectors are crucial for the performance and reliability of storage devices, as they ensure that data can be accessed quickly and efficiently. In networking servers, memory module connectors are used to connect the memory modules to the server's motherboard, enabling efficient data processing and communication. These connectors are essential for the performance and reliability of networking servers, as they ensure that data can be processed and transmitted quickly and efficiently. The Global Memory Module Connectors Market also finds usage in other applications, such as industrial equipment, medical devices, and automotive electronics. In these applications, memory module connectors are used to ensure efficient data transfer and communication between the memory and the processor, enabling the smooth operation of the device. As technology continues to advance, the demand for reliable and efficient memory module connectors is expected to grow, driven by the increasing complexity and performance demands of modern electronic devices. Manufacturers in the Global Memory Module Connectors Market are continually innovating to develop connectors that meet the evolving needs of the industry, focusing on aspects such as speed, reliability, and compatibility with various devices.

Global Memory Module Connectors Market Outlook:

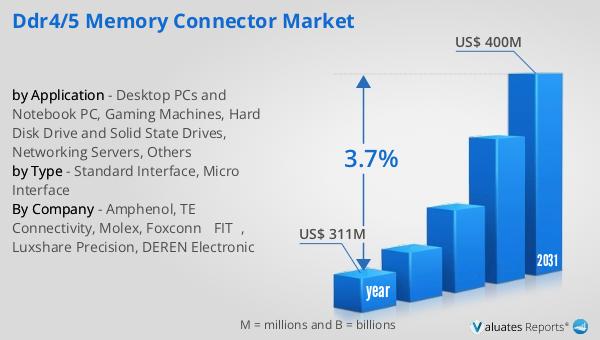

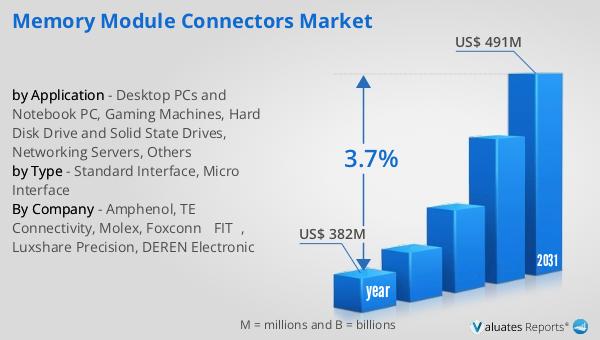

The outlook for the Global Memory Module Connectors Market indicates a promising growth trajectory. In 2024, the market was valued at approximately $382 million. By 2031, it is anticipated to expand to a revised size of $491 million, reflecting a compound annual growth rate (CAGR) of 3.7% over the forecast period. This growth is driven by several factors, including the increasing demand for high-performance computing devices, advancements in technology, and the growing need for faster data processing capabilities. As electronic devices become more sophisticated, the demand for reliable and efficient memory module connectors continues to rise. The market encompasses a wide range of products, including connectors for desktop PCs, notebook PCs, gaming machines, hard disk drives, solid-state drives, and networking servers. The evolution of technology and the increasing complexity of electronic devices are expected to further drive the growth of the Global Memory Module Connectors Market in the coming years. Manufacturers in this market are continually innovating to develop connectors that meet the evolving needs of the industry, focusing on aspects such as speed, reliability, and compatibility with various devices. The ongoing advancements in technology and the increasing demand for high-performance computing devices are expected to drive the growth of the Global Memory Module Connectors Market in the coming years.

| Report Metric | Details |

| Report Name | Memory Module Connectors Market |

| Accounted market size in year | US$ 382 million |

| Forecasted market size in 2031 | US$ 491 million |

| CAGR | 3.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Amphenol, TE Connectivity, Molex, Foxconn (FIT), Luxshare Precision, DEREN Electronic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |