What is Global Blood Test Analysis Software Market?

The Global Blood Test Analysis Software Market is a rapidly evolving sector within the healthcare industry, driven by the increasing demand for efficient and accurate diagnostic tools. This market encompasses software solutions designed to analyze blood test results, providing healthcare professionals with critical insights into a patient's health status. These software tools are integral in interpreting complex data from various blood tests, including complete blood counts, metabolic panels, and lipid profiles, among others. By automating the analysis process, these solutions enhance the speed and accuracy of diagnostics, leading to improved patient outcomes. The market is characterized by a growing adoption of advanced technologies such as artificial intelligence and machine learning, which further enhance the capabilities of these software solutions. As healthcare systems worldwide continue to prioritize precision medicine and personalized care, the demand for sophisticated blood test analysis software is expected to rise. This market is also influenced by the increasing prevalence of chronic diseases, which necessitates regular blood testing and monitoring. Overall, the Global Blood Test Analysis Software Market plays a crucial role in modern healthcare, offering tools that support timely and informed clinical decision-making.

Cloud Based, Web Based in the Global Blood Test Analysis Software Market:

In the Global Blood Test Analysis Software Market, cloud-based and web-based solutions are pivotal in transforming how blood test data is managed and analyzed. Cloud-based software solutions offer numerous advantages, particularly in terms of accessibility and scalability. These solutions allow healthcare providers to access blood test data from any location with internet connectivity, facilitating remote consultations and telemedicine services. This is particularly beneficial in rural or underserved areas where access to specialized healthcare services may be limited. Cloud-based platforms also offer the advantage of scalability, allowing healthcare facilities to expand their data storage and processing capabilities as needed without significant upfront investments in IT infrastructure. Moreover, cloud solutions often come with robust security measures, ensuring that sensitive patient data is protected against unauthorized access and breaches. On the other hand, web-based blood test analysis software provides a user-friendly interface that can be accessed through standard web browsers. This eliminates the need for complex installations and maintenance, making it an attractive option for smaller clinics and healthcare providers with limited IT resources. Web-based solutions are typically designed to be intuitive and easy to use, enabling healthcare professionals to quickly interpret blood test results and make informed clinical decisions. Both cloud-based and web-based solutions are integral to the Global Blood Test Analysis Software Market, offering flexibility, efficiency, and enhanced data management capabilities. As the healthcare industry continues to embrace digital transformation, the adoption of these solutions is expected to grow, driven by the need for improved diagnostic accuracy and patient care.

Hospital, Clinic, Others in the Global Blood Test Analysis Software Market:

The usage of Global Blood Test Analysis Software Market solutions is widespread across various healthcare settings, including hospitals, clinics, and other medical facilities. In hospitals, these software solutions are essential tools for managing the large volumes of blood test data generated daily. Hospitals often deal with complex cases that require comprehensive diagnostic evaluations, and blood test analysis software helps streamline this process by providing quick and accurate interpretations of test results. This not only enhances the efficiency of hospital laboratories but also supports clinicians in making timely and informed treatment decisions. In clinics, blood test analysis software is equally valuable, particularly in primary care settings where early detection and monitoring of health conditions are crucial. Clinics benefit from the software's ability to provide detailed insights into a patient's health, enabling proactive management of chronic diseases and other health issues. The software's user-friendly interface and automated features make it accessible to healthcare providers with varying levels of technical expertise. Beyond hospitals and clinics, blood test analysis software is also utilized in other settings such as research laboratories and diagnostic centers. In these environments, the software supports advanced research and development activities by facilitating the analysis of large datasets and identifying patterns or anomalies in blood test results. This can lead to new discoveries and innovations in medical science. Overall, the Global Blood Test Analysis Software Market plays a vital role in enhancing the quality and efficiency of healthcare services across different settings, contributing to better patient outcomes and advancing medical research.

Global Blood Test Analysis Software Market Outlook:

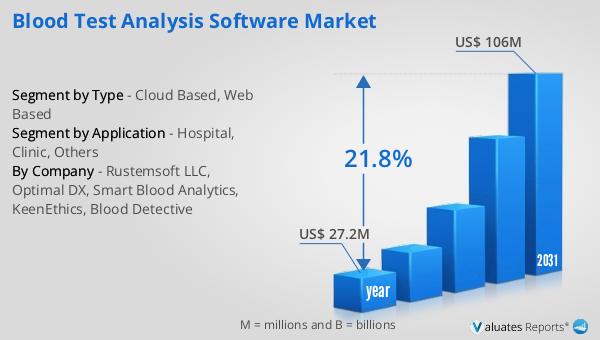

The outlook for the Global Blood Test Analysis Software Market indicates significant growth potential in the coming years. In 2024, the market was valued at approximately $27.2 million, and it is anticipated to expand to a revised size of $106 million by 2031, reflecting a robust compound annual growth rate (CAGR) of 21.8% during the forecast period. This impressive growth trajectory underscores the increasing demand for advanced diagnostic tools in the healthcare sector. A notable aspect of this market is the concentration of market share among the top five manufacturers, who collectively hold over 83% of the market. This suggests a competitive landscape where leading companies are driving innovation and setting industry standards. In terms of application, hospitals represent the largest segment, accounting for more than 62% of the market share. This dominance is likely due to the high volume of blood tests conducted in hospital settings and the critical need for accurate and efficient diagnostic solutions. As healthcare systems continue to evolve and prioritize precision medicine, the Global Blood Test Analysis Software Market is poised for continued expansion, driven by technological advancements and the growing emphasis on personalized patient care.

| Report Metric | Details |

| Report Name | Blood Test Analysis Software Market |

| Accounted market size in year | US$ 27.2 million |

| Forecasted market size in 2031 | US$ 106 million |

| CAGR | 21.8% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Rustemsoft LLC, Optimal DX, Smart Blood Analytics, KeenEthics, Blood Detective |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |