What is Global Epoxy-Based Concrete Floor Coatings Market?

The Global Epoxy-Based Concrete Floor Coatings Market is a specialized segment within the broader coatings industry, focusing on the application of epoxy-based materials to concrete floors. These coatings are renowned for their durability, resistance to wear and tear, and ability to withstand harsh environmental conditions. Epoxy-based coatings are particularly popular in industrial and commercial settings due to their ability to provide a seamless, easy-to-clean surface that can endure heavy foot and machinery traffic. The market is driven by the growing demand for high-performance flooring solutions in various sectors, including manufacturing, healthcare, and retail. Additionally, the aesthetic appeal of epoxy coatings, which can be customized with different colors and finishes, adds to their popularity in residential applications. As industries continue to prioritize safety and hygiene, the demand for epoxy-based concrete floor coatings is expected to rise, making it a vital component of modern construction and renovation projects. The market's growth is further supported by advancements in coating technologies, which enhance the performance and application efficiency of these products. Overall, the Global Epoxy-Based Concrete Floor Coatings Market plays a crucial role in enhancing the functionality and longevity of concrete floors across diverse environments.

Self-leveling Epoxy Coatings, Self-dispersing Epoxy Coatings in the Global Epoxy-Based Concrete Floor Coatings Market:

Self-leveling epoxy coatings and self-dispersing epoxy coatings are two prominent types of epoxy-based concrete floor coatings that cater to different needs within the Global Epoxy-Based Concrete Floor Coatings Market. Self-leveling epoxy coatings are designed to create a smooth, even surface over concrete floors, making them ideal for environments where aesthetics and ease of maintenance are paramount. These coatings are particularly beneficial in settings such as showrooms, kitchens, and hospitals, where a seamless appearance is desired. The self-leveling property ensures that the coating spreads evenly across the floor, filling in any minor imperfections and creating a uniform surface. This not only enhances the visual appeal but also simplifies cleaning and maintenance, as there are no joints or seams where dirt and bacteria can accumulate. Additionally, self-leveling epoxy coatings can be customized with various colors and patterns, allowing for creative design possibilities that can enhance the ambiance of a space. On the other hand, self-dispersing epoxy coatings are known for their exceptional mechanical strength and are often used in areas subjected to heavy loads and high traffic. These coatings are reinforced with quartz sand, which enhances their durability and resistance to impact, making them suitable for industrial environments such as warehouses, factories, and garages. The self-dispersing nature of these coatings ensures that they spread evenly across the floor, providing a robust and resilient surface that can withstand the rigors of daily operations. This type of coating is particularly advantageous in settings where forklifts, heavy machinery, and other equipment are frequently used, as it can endure the stress and strain imposed by such activities. Moreover, self-dispersing epoxy coatings offer excellent resistance to chemicals and abrasions, further extending the lifespan of the flooring and reducing the need for frequent repairs or replacements. Both self-leveling and self-dispersing epoxy coatings contribute significantly to the versatility and adaptability of the Global Epoxy-Based Concrete Floor Coatings Market. While self-leveling coatings prioritize aesthetics and ease of maintenance, self-dispersing coatings focus on strength and durability. This diversity allows businesses and homeowners to select the most appropriate solution based on their specific needs and preferences. For instance, a retail store may opt for self-leveling coatings to create an inviting and visually appealing shopping environment, while a manufacturing facility may choose self-dispersing coatings to ensure the flooring can withstand the demands of heavy machinery and equipment. The ability to tailor epoxy coatings to different applications underscores their importance in modern construction and renovation projects, where both functionality and aesthetics are crucial considerations. As the market continues to evolve, innovations in epoxy coating formulations and application techniques are expected to further enhance the performance and appeal of these products, solidifying their position as a preferred choice for concrete floor coatings worldwide.

Residential Building, Non-Residential in the Global Epoxy-Based Concrete Floor Coatings Market:

The usage of Global Epoxy-Based Concrete Floor Coatings Market in residential and non-residential buildings highlights the versatility and adaptability of these coatings in various settings. In residential buildings, epoxy-based concrete floor coatings are increasingly popular due to their ability to transform ordinary concrete floors into attractive and durable surfaces. Homeowners appreciate the seamless finish and the wide range of color options available, which allow them to customize their floors to match their interior design preferences. Epoxy coatings are particularly favored in areas such as basements, garages, and kitchens, where durability and ease of maintenance are essential. The coatings provide a protective layer that resists stains, spills, and scratches, making them ideal for high-traffic areas in the home. Additionally, the non-porous nature of epoxy coatings ensures that they do not harbor dust, allergens, or bacteria, contributing to a healthier indoor environment. In non-residential buildings, the application of epoxy-based concrete floor coatings is driven by the need for robust and resilient flooring solutions that can withstand the demands of commercial and industrial operations. In commercial spaces such as retail stores, restaurants, and offices, epoxy coatings offer a combination of aesthetic appeal and practicality. The seamless finish and customizable design options allow businesses to create a welcoming and professional atmosphere for customers and employees. Moreover, the durability and low maintenance requirements of epoxy coatings make them a cost-effective choice for businesses looking to minimize downtime and maintenance expenses. In industrial settings, such as factories, warehouses, and laboratories, epoxy coatings are valued for their strength and resistance to chemicals, abrasions, and heavy loads. These properties ensure that the flooring can endure the rigors of daily operations, reducing the risk of damage and the need for frequent repairs. The adaptability of epoxy-based concrete floor coatings to different environments and requirements underscores their significance in the construction and renovation of both residential and non-residential buildings. Whether enhancing the aesthetic appeal of a home or providing a durable and practical flooring solution for a commercial or industrial facility, epoxy coatings offer a versatile and reliable option. As the demand for high-performance flooring solutions continues to grow, the Global Epoxy-Based Concrete Floor Coatings Market is poised to play a crucial role in meeting the diverse needs of modern construction projects. The ongoing development of new formulations and application techniques is expected to further expand the capabilities and applications of epoxy coatings, ensuring their continued relevance and popularity in the years to come.

Global Epoxy-Based Concrete Floor Coatings Market Outlook:

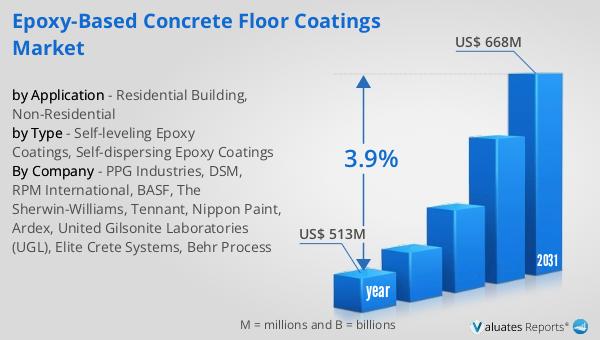

In 2024, the global market for Epoxy-Based Concrete Floor Coatings was valued at approximately $513 million. Looking ahead, this market is anticipated to grow, reaching an estimated value of $668 million by the year 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.9% over the forecast period. The steady increase in market size reflects the rising demand for durable and aesthetically pleasing flooring solutions across various sectors. As industries and homeowners alike seek to enhance the functionality and appearance of their spaces, epoxy-based coatings are becoming an increasingly popular choice. The market's expansion is driven by the coatings' ability to provide long-lasting protection and a seamless finish, which are highly valued in both residential and non-residential applications. Additionally, advancements in coating technologies and application methods are expected to further fuel market growth, offering improved performance and efficiency. As the market continues to evolve, the Global Epoxy-Based Concrete Floor Coatings Market is set to play a pivotal role in shaping the future of flooring solutions worldwide, catering to the diverse needs of modern construction and renovation projects.

| Report Metric | Details |

| Report Name | Epoxy-Based Concrete Floor Coatings Market |

| Accounted market size in year | US$ 513 million |

| Forecasted market size in 2031 | US$ 668 million |

| CAGR | 3.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | PPG Industries, DSM, RPM International, BASF, The Sherwin-Williams, Tennant, Nippon Paint, Ardex, United Gilsonite Laboratories (UGL), Elite Crete Systems, Behr Process |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |