What is Wash-free CTP Plates - Global Market?

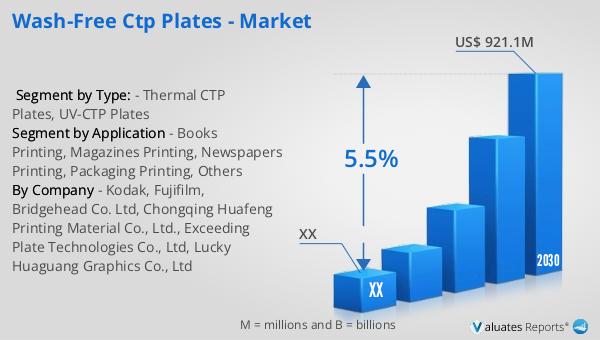

Wash-free CTP (Computer-to-Plate) plates represent a significant advancement in the printing industry, offering a more environmentally friendly and efficient alternative to traditional plate processing methods. These plates eliminate the need for chemical processing, which not only reduces the environmental impact but also simplifies the workflow for printing companies. The global market for wash-free CTP plates is driven by the increasing demand for sustainable printing solutions and the need to reduce operational costs. By eliminating the wash step, these plates help in reducing water and chemical usage, which is a significant advantage for companies looking to adopt greener practices. Additionally, wash-free CTP plates offer improved image quality and consistency, which are crucial for high-quality print production. As more companies become aware of the environmental and economic benefits of wash-free CTP plates, their adoption is expected to grow, further driving the market. The global market for these plates was valued at approximately US$ 629 million in 2023 and is projected to reach US$ 921.1 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2024 to 2030. This growth is indicative of the increasing shift towards sustainable printing technologies across the globe.

Thermal CTP Plates, UV-CTP Plates in the Wash-free CTP Plates - Global Market:

Thermal CTP plates and UV-CTP plates are two prominent types of wash-free CTP plates that have gained traction in the global market due to their distinct advantages and applications. Thermal CTP plates are known for their high precision and stability, making them ideal for high-quality printing tasks. These plates use thermal energy to create images on the plate, which results in sharp and consistent prints. The absence of chemical processing in thermal CTP plates not only reduces environmental impact but also enhances the efficiency of the printing process by minimizing downtime and maintenance requirements. On the other hand, UV-CTP plates utilize ultraviolet light to transfer images onto the plate. These plates are particularly advantageous for their versatility and ability to work with a wide range of substrates, including non-absorbent materials. This makes UV-CTP plates suitable for various printing applications, from packaging to specialty prints. The global market for wash-free CTP plates, including thermal and UV-CTP variants, is driven by the increasing demand for high-quality and sustainable printing solutions. As businesses strive to reduce their carbon footprint and operational costs, the adoption of these advanced plates is expected to rise. The market's growth is further supported by technological advancements that continue to enhance the performance and capabilities of thermal and UV-CTP plates. With the ongoing shift towards digitalization and sustainability in the printing industry, the demand for wash-free CTP plates is anticipated to grow, offering significant opportunities for manufacturers and suppliers in the market. The North American market, in particular, is expected to witness substantial growth, driven by the region's focus on adopting eco-friendly technologies and the presence of a robust printing industry. As the market evolves, manufacturers are likely to invest in research and development to further improve the efficiency and environmental benefits of wash-free CTP plates, ensuring their continued relevance and competitiveness in the global market.

Books Printing, Magazines Printing, Newspapers Printing, Packaging Printing, Others in the Wash-free CTP Plates - Global Market:

Wash-free CTP plates are increasingly being utilized across various printing sectors, including books, magazines, newspapers, packaging, and other specialized printing applications. In the realm of book printing, wash-free CTP plates offer significant advantages by providing high-quality, consistent prints that are essential for producing professional-grade publications. The elimination of chemical processing not only reduces production costs but also aligns with the growing demand for environmentally sustainable printing practices. Similarly, in magazine printing, where vibrant colors and sharp images are crucial, wash-free CTP plates deliver superior image quality and reliability. The ability to produce high-resolution prints without the need for chemical processing makes these plates an attractive option for magazine publishers looking to enhance their production efficiency and reduce their environmental impact. In the newspaper industry, where speed and cost-effectiveness are paramount, wash-free CTP plates offer a streamlined workflow that minimizes downtime and maintenance requirements. The quick turnaround time and reduced operational costs associated with these plates make them an ideal choice for newspaper publishers aiming to stay competitive in a fast-paced market. Packaging printing also benefits from the versatility and high-quality output of wash-free CTP plates. The ability to print on a wide range of substrates, including non-absorbent materials, makes these plates suitable for various packaging applications, from food and beverage to consumer goods. The environmental benefits of wash-free CTP plates further enhance their appeal in the packaging sector, where sustainability is becoming increasingly important. Beyond these traditional applications, wash-free CTP plates are also being used in other specialized printing areas, such as signage and promotional materials, where high-quality, durable prints are required. The global market for wash-free CTP plates is expected to continue growing as more industries recognize the benefits of adopting sustainable and efficient printing technologies. As businesses across different sectors strive to reduce their environmental impact and improve their operational efficiency, the demand for wash-free CTP plates is likely to increase, driving further innovation and growth in the market.

Wash-free CTP Plates - Global Market Outlook:

The global market for wash-free CTP plates was valued at approximately US$ 629 million in 2023 and is projected to reach a revised size of US$ 921.1 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2024 to 2030. This growth is indicative of the increasing shift towards sustainable printing technologies across the globe. The North American market for wash-free CTP plates was valued at a certain amount in 2023 and is expected to reach a specific value by 2030, with a CAGR of a certain percentage during the forecast period from 2024 through 2030. This growth is driven by the region's focus on adopting eco-friendly technologies and the presence of a robust printing industry. As the market evolves, manufacturers are likely to invest in research and development to further improve the efficiency and environmental benefits of wash-free CTP plates, ensuring their continued relevance and competitiveness in the global market. The increasing demand for high-quality and sustainable printing solutions is expected to drive the adoption of wash-free CTP plates, offering significant opportunities for manufacturers and suppliers in the market. With the ongoing shift towards digitalization and sustainability in the printing industry, the demand for wash-free CTP plates is anticipated to grow, providing a promising outlook for the market in the coming years.

| Report Metric | Details |

| Report Name | Wash-free CTP Plates - Market |

| Forecasted market size in 2030 | US$ 921.1 million |

| CAGR | 5.5% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Kodak, Fujifilm, Bridgehead Co. Ltd, Chongqing Huafeng Printing Material Co., Ltd., Exceeding Plate Technologies Co., Ltd, Lucky Huaguang Graphics Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |