What is ARM Based Microcontroller - Global Market?

ARM-based microcontrollers are a crucial component in the global market for embedded systems, serving as the brain for a wide range of electronic devices. These microcontrollers are built on the ARM architecture, which is known for its efficiency and performance. ARM, which stands for Advanced RISC Machine, is a family of computer processors that are designed to be energy-efficient and powerful, making them ideal for use in a variety of applications. The global market for ARM-based microcontrollers is vast and diverse, encompassing industries such as automotive, consumer electronics, industrial automation, and more. These microcontrollers are favored for their ability to handle complex tasks while consuming minimal power, which is essential in today's world where energy efficiency is a top priority. As technology continues to advance, the demand for ARM-based microcontrollers is expected to grow, driven by the increasing need for smart, connected devices that can perform a wide range of functions. The versatility and adaptability of ARM-based microcontrollers make them a key player in the global market, as they can be customized to meet the specific needs of different industries and applications.

Flash, Roomless, Others in the ARM Based Microcontroller - Global Market:

In the realm of ARM-based microcontrollers, there are several types that cater to different needs and applications, including Flash, Roomless, and Others. Flash-based ARM microcontrollers are among the most popular due to their ability to store data even when the power is turned off. This non-volatile memory is crucial for applications where data retention is important, such as in automotive electronics and consumer devices. Flash memory allows for easy updates and modifications, making these microcontrollers highly adaptable to changing requirements. On the other hand, Roomless ARM microcontrollers are designed to be compact and efficient, often used in applications where space is a constraint. These microcontrollers are ideal for portable devices and wearables, where minimizing size and weight is crucial. The Roomless design allows for integration into small form factors without compromising on performance. The "Others" category encompasses a range of ARM-based microcontrollers that may not fit neatly into the Flash or Roomless categories but offer unique features and capabilities. These could include microcontrollers with specialized functions for industrial automation, medical devices, or telecommunications. Each type of ARM-based microcontroller brings its own set of advantages, allowing manufacturers to choose the best fit for their specific application. The flexibility of ARM architecture means that these microcontrollers can be tailored to meet the demands of various industries, from high-performance computing to low-power IoT devices. As the global market for ARM-based microcontrollers continues to expand, the diversity of options available ensures that there is a solution for every need, whether it's for high-speed data processing or energy-efficient operation. This adaptability is one of the key reasons why ARM-based microcontrollers are so prevalent in today's technology landscape, providing the foundation for innovation across multiple sectors.

Communication Equipment, Automotive Electronics, Computer, Others in the ARM Based Microcontroller - Global Market:

ARM-based microcontrollers play a significant role in various sectors, including communication equipment, automotive electronics, computers, and others. In communication equipment, these microcontrollers are essential for managing data transmission and processing tasks. They enable devices such as routers, modems, and smartphones to handle complex communication protocols efficiently. The low power consumption and high processing power of ARM-based microcontrollers make them ideal for these applications, where reliability and speed are crucial. In the automotive industry, ARM-based microcontrollers are used in a wide range of applications, from engine control units to advanced driver-assistance systems (ADAS). They help improve vehicle performance, safety, and efficiency by managing various electronic systems within the car. The ability to process large amounts of data quickly and accurately is vital in automotive electronics, where real-time decision-making can impact safety and performance. In the realm of computers, ARM-based microcontrollers are used in everything from laptops to servers, providing the processing power needed for a variety of tasks. Their energy efficiency is particularly beneficial in portable devices, where battery life is a critical factor. Finally, in the "Others" category, ARM-based microcontrollers find applications in areas such as industrial automation, medical devices, and consumer electronics. Their versatility and adaptability make them suitable for a wide range of uses, from controlling machinery in a factory to powering smart home devices. The global market for ARM-based microcontrollers is driven by the increasing demand for smart, connected devices across these sectors, as they provide the processing power and efficiency needed to support the growing complexity of modern technology.

ARM Based Microcontroller - Global Market Outlook:

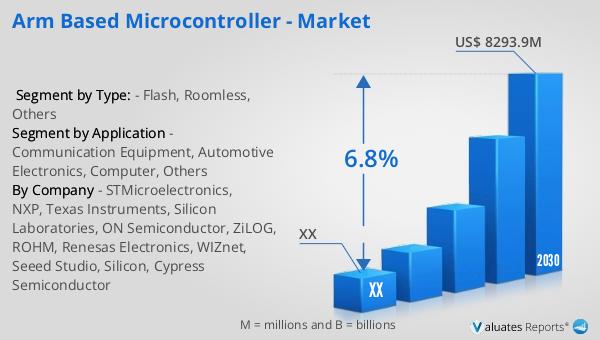

The global market for ARM-based microcontrollers was valued at approximately $5,312 million in 2023. This market is projected to grow significantly, reaching an estimated size of $8,293.9 million by the year 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 6.8% during the forecast period from 2024 to 2030. This upward trend reflects the increasing demand for ARM-based microcontrollers across various industries, driven by the need for efficient, high-performance processing solutions. The versatility of ARM architecture allows these microcontrollers to be used in a wide range of applications, from consumer electronics to industrial automation, contributing to their growing popularity. As technology continues to evolve, the demand for smart, connected devices is expected to rise, further fueling the growth of the ARM-based microcontroller market. This market expansion is indicative of the critical role that ARM-based microcontrollers play in the development of modern technology, providing the processing power and efficiency needed to support a wide range of applications. The projected growth of this market underscores the importance of ARM-based microcontrollers in the global technology landscape, as they continue to drive innovation and enable new possibilities across various sectors.

| Report Metric | Details |

| Report Name | ARM Based Microcontroller - Market |

| Forecasted market size in 2030 | US$ 8293.9 million |

| CAGR | 6.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | STMicroelectronics, NXP, Texas Instruments, Silicon Laboratories, ON Semiconductor, ZiLOG, ROHM, Renesas Electronics, WIZnet, Seeed Studio, Silicon, Cypress Semiconductor |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |